The Supreme Court of India recently rebuked the Insurance Regulatory and Development Authority of India [IRDAI] for not complying to its norms. The apex court had recently ordered insurance providers to not issue car insurance covers to those vehicles that didn’t have PUC certificates. The order was passed mainly to curb the growing problem of air pollution in the country. However, the Supreme Court found that the insurance companies were readily issuing new plans as well as allowing policyholders to renew car insurance without checking the PUC certificates.

Image Source – Car Insurance

Following norms, says IRDAI

The IRDAI, which is the apex insurance regulatory body in India, said that the car insurance sector was merely following the guidelines of the Insurance Act. The act states that every vehicle on the roads of India needs a basic third-party cover. The IRDAI or the insurance providers cannot refuse a car insurance renewal request based on the PUC status.

Not following orders, complains Supreme Court

The Supreme Court, however, is not willing to listen to any of this. The court has now strictly ordered the insurance sector to follow the car insurance renewal norms with immediate effect. The PUC certificate is an absolute must. Unless a vehicle has a PUC certificate, the owner cannot renew car insurance. And since car insurance is compulsory, the vehicle cannot be driven on the roads.

What exactly is the PUC?

The PUC is the Pollution Under Control certificate. As a vehicle owner, you need to get this certificate renewed from time to time. For this, your vehicle’s emission is tested and if found suitable, the certificate is issued. If there is a fault in the engine or the fuel exhaustion, the pollution will be a lot. You need to get it fixed and then get the PUC. You cannot have an insurance renewal unless the PUC is obtained.

Why is the Supreme Court making it a requirement?

There are two main reasons why the apex court is so insistent on having a PUC clearance for getting a car insurance renewal. They are:

Forces people to get a PUC – Air pollution is one of the largest mass killers of India. Thousands of people die because of this each year. And since vehicles majorly contribute to air pollution, it is extremely important to keep the emissions under control. If you cannot get a car insurance cover without a PUC, you will be forced to keep the pollution in check. If you don’t and your policy lapses, you will have to pay a higher car insurance premium to get it reinstated. So, the SC ruling is a healthy one to ensure every vehicle keeps its pollution levels in check.

Makes it easier to maintain air pollution levels – As stated, air pollution is dangerous. The SC order, therefore, is a positive step to maintain the air pollution levels. It is a handy way to ensure the vehicles don’t emit harmful gasses and the air we breathe remains clean. It will also keep a tab on the number of vehicles that violate the pollution norms and allow the authorities to take suitable action against them.

This is the main logic behind the Supreme Court’s recent ruling regarding PUC and car insurance renewals, and its insistence that all insurance companies follow it.

The bottom line

Car insurance is compulsory in India. You have to pay the car insurance premium and get the plan renewed before it expires. However, you need a PUC certificate before you do so. The Supreme Court insists this. But, since the IRDAI is bounded by the Insurance Act, it is forced to issue the plans even without the PUC certificates.

You should however be a good citizen and get the PUC done on your part as it is good for your vehicle and also for the environment. Get it done and then renew your car plan in the most suitable and lawful manner possible.

The returns from an investment decision are largely dependent upon the time frame of investment. Often, the financial impact of an investment can span across one’s entire lifetime. Hence, it becomes critical for one to have well defined financial goals. There are several other factors like risk profile, returns expected, fees and liquidity considerations while choosing a financial product. There is a high probability you must have heard the popular marketing line ‘Mutual Funds Sahi Hai’. But when compared to some of the features of ULIPs, like insurance and risk, MFs are a Nahi.

Image Source

We shall consider two financial instruments: ULIPs and MFs and compare both.

Meaning of ULIP

ULIP stands for Unit Linked Insurance Plan, i.e. an investment option which provides market-linked wealth creation along with life cover, by paying premiums till maturity. Besides, ULIP is also subject to tax benefits.

Meaning of Mutual Funds

A mutual fund is a professionally managed investment fund that pools money from several investors [retail and institutional] to buy tradeable securities.

Comparison of the features of ULIP vs Mutual Funds

Insurance – The single biggest ULIP benefit is that unlike mutual funds, ULIPs offer a life cover. This is the money the insurance company promises to pay the policyholder’s family in case of an untimely death of the insured.

Risk-return trade-off – There is a fundamental rule of finance i.e. high risk, high return. Since ULIPs are primarily insurance products, the risk is low, and the returns are limited and assured. On the other hand, mutual funds are of various types i.e. equity, hybrid and debt with subsequently reducing risk profile and declining returns, in that order.

Fees – Owing to a large number of investors pooling their funds, the management fees in mutual funds is relatively lower than ULIPs.

Liquidity concerns – Mutual funds are widely traded in the secondary markets and are more liquid compared to ULIPs.

Should I take a look at ULIPs?

A financially prudent investor definitely should. ULIP is a dual advantage product with in-built insurance and investment features.

Consider an example. Mr. A invests 50,000 in a ULIP, while Mr B buys mutual fund units with the same amount. All of this money is invested for both Mr A and Mr B. However, every month, a part of Mr. A’s investment is taken as insurance cover, which acts as the ‘protection for insurance premium’. This buys him an insurance cover of Rs 5 lakh. In Mr B’s case, he would need to buy an insurance policy separately to get a life cover. In case Mr. A meets with an accident and passes away, the insurance company would compensate his family with Rs 5 lakh or the fund value, whichever is higher. Mr B, however, will not receive the same benefits.

Conclusion

After looking into the pros and cons of investing in ULIPs and mutual funds, it can be concluded that there is no ‘one size fits all’. A prudent investor must consider diversification of his investment portfolio to leverage upon the insurance advantage of ULIP and the high return potential of mutual funds. You might ask “So why should I invest in ULIP?” To combine the insurance and investment benefits under one comprehensive plan, invest in a ULIP today.

With rising medical expenses, buying a health insurance policy has become a need of the hour. The rise in the popularity of health insurance plans has prompted the insurance providers to come up with lucrative and appealing policies for the customers. One such contemporary insurance service provided by most of the insurers is the cashless health insurance policy.

Image Source

Under the Cashless Mediclaim Policy, the medical expenses of the insured are directly settled by the insurance company. The insured is relieved from the hassles of paying cash at the hospital during the treatment. As cashless insurance is devised to eliminate payment through cash, the reimbursement part is successfully avoided. Cashless health insurance is extremely helpful at times of emergency when there’s no immediate access to cash.

How to avail cashless health insurance?

Make sure that the hospital where you undergo your treatment is present in the network of hospitals covered by the insurance company. A policy card is made available to all those who are covered under cashless health insurance. You are required to display this policy card at the hospital in order to avail the cashless facility. After presenting the policy card, you will have to fill a pre-authorization form. This form is then sent to the Third Party Administrators (TPA) for the verification of authenticity and eligibility. Following the validation from the TPA, the hospital receives a letter approving the treatment. The TPA processes the request within 6 hours, hence during emergency cases, the amount can be paid in cash. This amount is later reimbursed by the insurance company.

Make sure that you have a complete understanding of cashless health insurance before you buy this policy. Certain things that you must take note of before purchasing this policy are mentioned below:

Read the documents carefully to be well-versed with the terms and conditions of the policy.

In case the total medical expense does not fall with the limits of sum assured, you will have to pay for the remaining amount.

It is advisable that you keep a copy of hospital bills for future reference.

While you fill the pre-authorization form, make sure all the details are correct. Failing to which, your claim request would be at risk of getting rejected by the TPA.

The cashless health insurance policy does not cover documentation and service charges.

Other charges such as equipment charges are also not covered by the insurance provider.

Cashless health insurance can be categorized into two main categories, i.e cashless family health insurance and cashless health insurance for senior citizens. One of the most important advantages of cashless health insurance is that it offers complete peace of mind to the insured who is seeking treatment. It allows individuals to focus on their recovery rather than being worried about paying the hospital bills.

Cashless health insurance plays a significant role in reducing the financial burden due to rising medical expenses. Moreover, in emergency situations, it can become extremely difficult for patients or their family members to arrange funds on an immediate basis. This is where cashless health insurance can act as savior. Customized by keeping the consumers in mind, the cashless health insurance also offers a wide coverage that includes pre and posts hospitalization expenses and inpatient care. Some of the insurance providers also cover the ambulance charges. Hence, it is recommended that you must always compare various plans and then choose the one that matches your expectation. Now that you know the benefits of cashless health insurance, it’s time that you safeguard yourself and your family from the uncertainties of life by buying a health insurance policy that suits your needs in the best possible way.

There are many traits that differ from one person to another, investing is one of them. There is a famous saying which mentions that ‘Risks and Rewards are two sides of the same coin’. It can be said that ‘Greater the risk, higher is the probability of making rewards’. Not every investor can afford that route since investing depends heavily on factors like investor’s age, present portfolio, ability to take risks, current assets & liabilities, etc.

Image Source – Finance

As famous American investor Peter Lynch says ‘Do your homework’ and the same sentiment is echoed by legendary investor Warrant Buffet who says ‘Be selective’ i.e. Once you get a hang of investing money & have a well-balanced portfolio, narrow down those investments so that it reflects your goals. Goals would again vary from one person to another, some examples of goals are

Enjoying an early retirement.

Purchasing a flat/house within a specific span of time.

Plan higher education of your children, etc.

Goals have to be more realistic in nature so that you plan your investments in such a manner that each step takes you close to your goal. This could be termed as goal-based investing. Goals could either be a short-term goal or a long-term goal. In order to have a balanced portfolio, many investors follow a mix of ‘conservative + aggressive’ approach to investing.

Investment Options for ‘All types of Investors’

Investments in Fixed Deposits [FD], Recurring Deposits [RD], Public Provident Fund [PPF], Post-Office schemes, etc. are some of the common instruments in which conservative investors invest their money. Though different banks have different rates to offer for RD/FD, the average rate of interest for Fixed Deposit [FD] is close to 5.75% [maximum being 6.25%] and the average rate of interest for Recurring Deposit [RD] is close to 4% [maximum being 8%]. The interest rates might vary from one bank to another and the rates also keep fluctuating. ‘Rate of inflation’ is one of the major factors that can influence the banks to either increase/decrease Fixed Deposit rates. FD’s & RD’s offer the best combination of attractive interest rates, safety of capital, good returns [without much risk on investor’s part], and liquidity.

Even though you are a conservative investor, there is a high possibility that you would have opted for an insurance policy of any nature. There are different types of life insurance policies, namely Endowment plans, Term plans, and Money back plans. Term Plans provide only life-covers and are available at affordable premiums. ‘Term Plans’ are the best ways in which you ensure that your family members do not have to suffer in case any untoward incident happens to you. Many people who take home-loans opt for a ‘Term Plan’ from the bank that issued the loan; other investors choose the Money back plan or Endowment plan depending on his profile. Irrespective of your risk appetite & investment portfolio, it is recommended to always have at least one Term Insurance plan. Before taking a term insurance plan, always have a look at how much term-insurance coverage you need.

Systematic Investment Plan [SIP] – Good Returns with Marginal Risk

System Investment Plan [SIP] is another popular investment vehicle that yields good returns. A popular study shows that 51% of parents in India yield their children to be highly successful in life. This also means that you need to provide best-quality education so that your child can become educated and pursue a better career. Investing in ‘low-risk investment options’ [which were discussed before] would not yield great returns, hence it becomes necessary to invest in other options like SIP which can bring returns which can beat the ‘rising inflation’. It is suited for both low-risk & high-risk investors.

Investing in Mutual Funds via SIP’s is a good investment option where you can invest a fixed sum of your preference at regular intervals. This can be instrumental to achieve short-term, as well as long-term goals e.g. Goal of financing your child’s higher education, planning for retirement, etc. Investment in Equity Funds can offer returns at around 10~15% pa. Investment in SIPs is the ideal approach to long-term investing.

Let’s take a hypothetical example of two people ‘Ramesh’ & ‘Suresh’ who are near the same age, earn almost the same, but follow different investment ideologies. Ramesh invests close to Rs. 10,000 per month in a SIP, starting from the age of 30. At 15% annualized rate of return, he would have a corpus of Rs. 7 crore by the age of 60. Suresh, on the other hand, realizes the importance of investing in SIP at a later stage in his career and starts investing in SIP at the age of 40. The investment amount is Rs. 12,000. By the age of 60, Suresh would have a corpus amount of Rs. 1.8 crore, which is way lesser than what his colleague Ramesh could accumulate.

By looking at some of the investment options available for different categories of investors [Conservative + Aggressive], one thing that can be concluded is that ‘safest investment options’ [like Fixed Deposits, Recurring Deposits, etc.] can be common in their portfolio. No one would want to put all their eggs i.e. money in one ‘type of basket’ since that would be a very risky game.

This is where the product named FD Xtra by ICICI Bank can be a big boon for investors since it is not a normal FD/RD. There are many added advantages and this is why it has a ‘market-fit’ in today’s changing times.

FD Xtra – Fixed Deposits & Recurring Deposits with many ‘investment advantages’

Before we have a look at the features of this innovative product by ICICI Bank, we should have a look at some of the important points that were discussed in the ‘interim union budget’ that was announced a few weeks back. This year’s interim budget brought lot of cheer for the ‘middle-class’ & ‘working class’. The government has proposed to increase the TDS [tax deducted at source] threshold on Post Office Savings and Bank Deposits.to Rs. 40,000 from Rs 10,000.

The increase in the TDS limit for FD & RD is a welcome move since it would encourage more number of investors to invest in these financial instruments. What if the investor who invests in FD/RD also gets a free term-insurance/option to invest in SIPs/investing to make your ‘goals’ a reality? This is where FD Xtra from ICICI Bank could be a game-changer as it packs the features of a safe investment option like FD/RD and also offers investors to generate more wealth by providing a ‘gamut of services’ like investing in SIP’s, etc.

This product serves two advantages

Offers safety of traditional investment options like FD, RD

Offers an option to invest in other high-growth financial instruments like SIP. Many investors in this category are still not aware of the importance of having a term-insurance, the advantages of having SIP, etc.

Let’s have a look at some of the investment schemes in FD Xtra

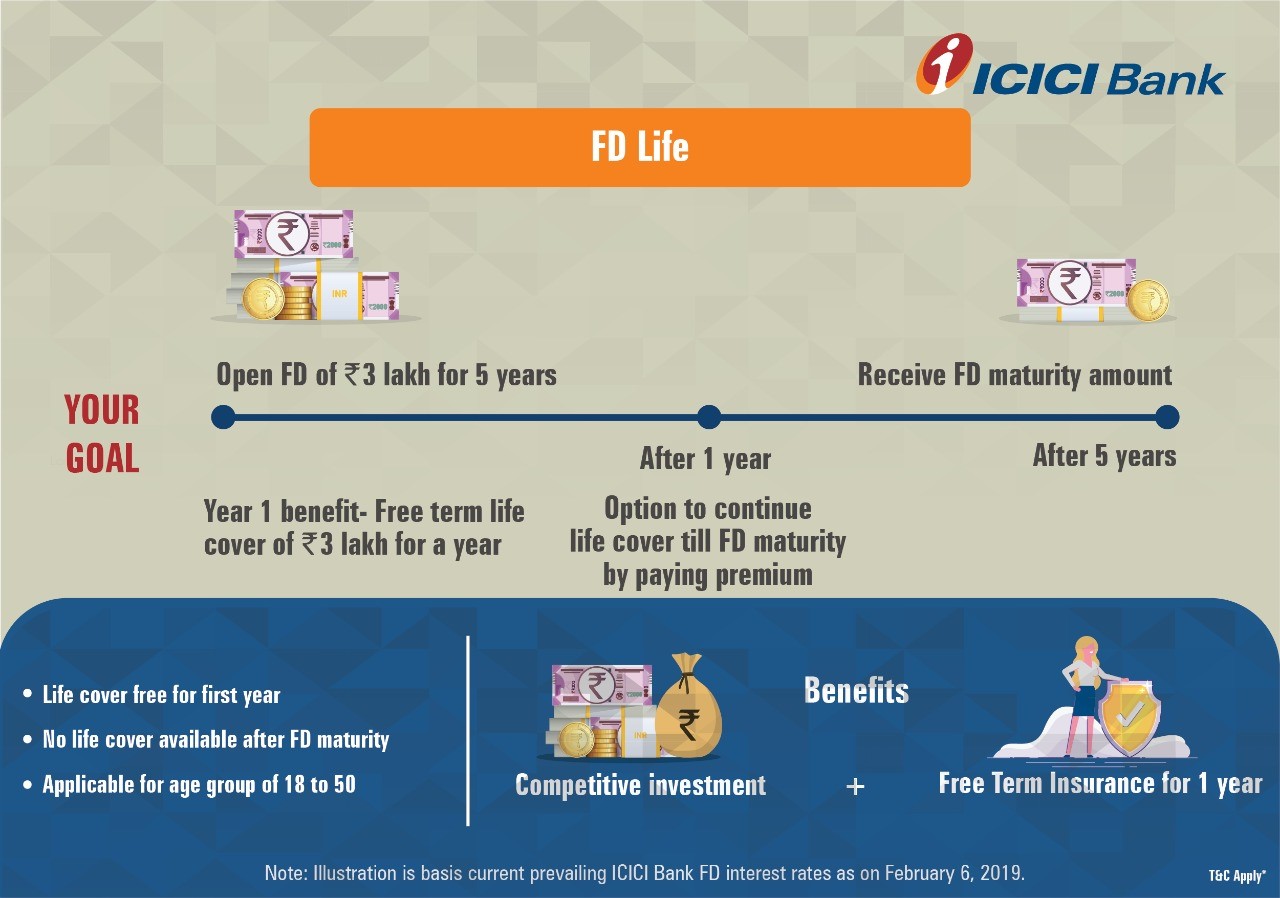

FD Life

This product offers customers a complimentary term life insurance cover of Rs. 3 lakh for one year by opening a Fixed Deposit of minimum value of Rs. 3 lakh and tenure 2 years and above.

Example– Akshay, 32 years, is recently blessed with a child. He opens a Fixed Deposit of Rs. 3 lakh for her education in five years. With ICICI Bank FD Life, he gets a free term life insurance cover of Rs. 3 lakh for a year. [He can renew it next year, if he chooses to]. This will financially secure his loved ones from any eventuality.

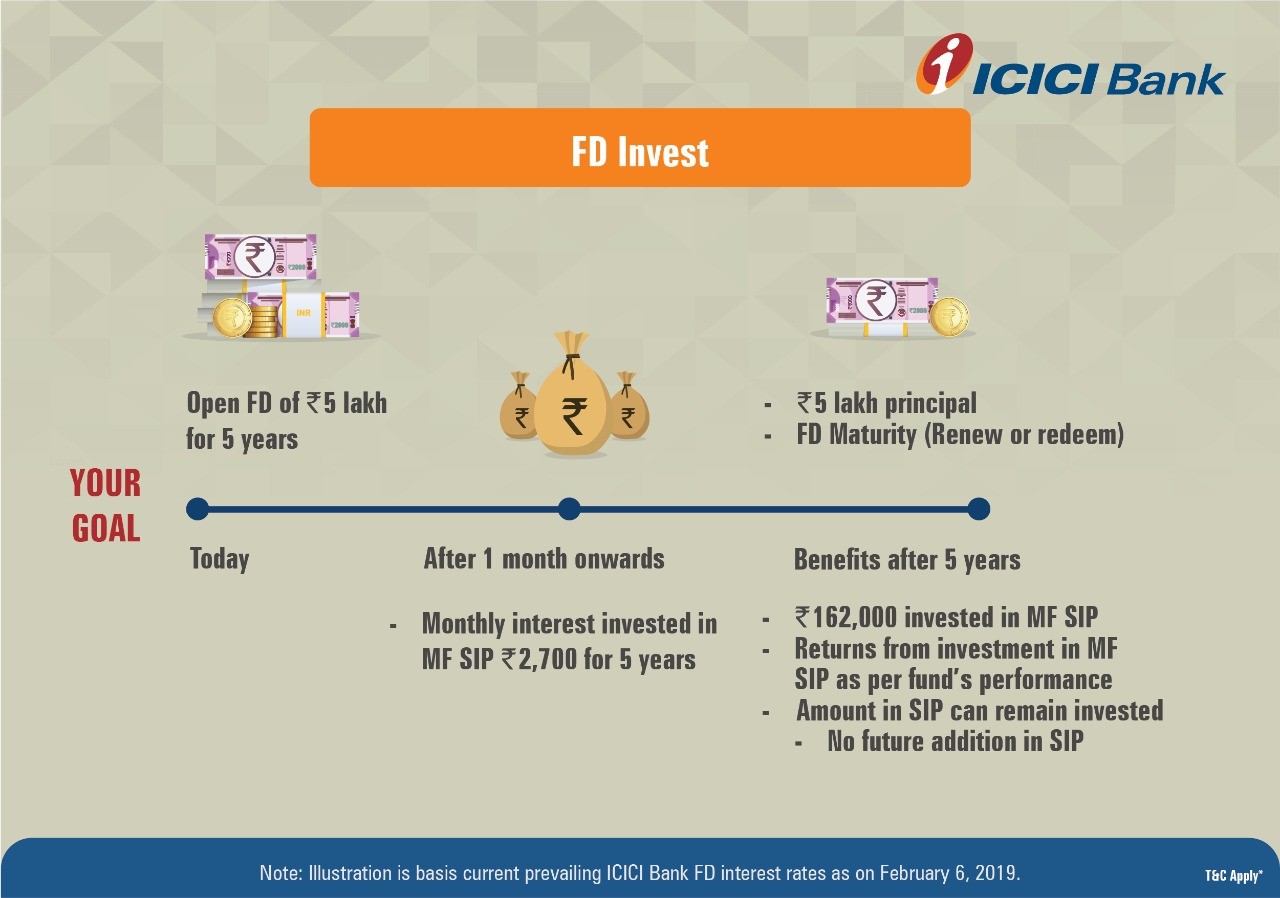

FD Invest

It is a unique product that offers customers the safety of a FD and returns of a Mutual Fund. This proposition enables customers earn monthly interest on principal invested. This interest is in turn invested in a Mutual Fund via monthly SIP.

Example– Neha, a working woman, is a conservative investor who doesn’t like to expose her hard earned money to volatility of equity markets. At the same time, she feels she is missing on the higher returns associated with equity markets. She opens a FD Invest of Rs. 5 lakh for tenure of 5 years. This will protect her principal invested and offer monthly interest of Rs. 2,702 post tax. Neha decides to put Rs. 2,700 in a Mutual Fund SIP. So her total investment in SIP for 5 years will be Rs. 162,000, while her principal invested is safe.

FD Income with Monthly Income

This facility enables customers to receive the maturity amount of the deposit as a monthly income for a tenure of their choice. The service is designed specially for meeting life stage needs like retirement among others.

Example– Raman, a private sector employee, has received a significant retirement corpus. FD Xtra can help him in getting a regular monthly income. For example, he invests Rs. 5 lakh in FD with Monthly Income for a tenure of 2 years as the FD investment phase. Post the investment phase, he will receive a monthly income (before TDS) of Rs. 25,911 for 2 years. He has the option of selecting the FD investment phase and the payout phase in any combination upto an aggregate of 10 years.

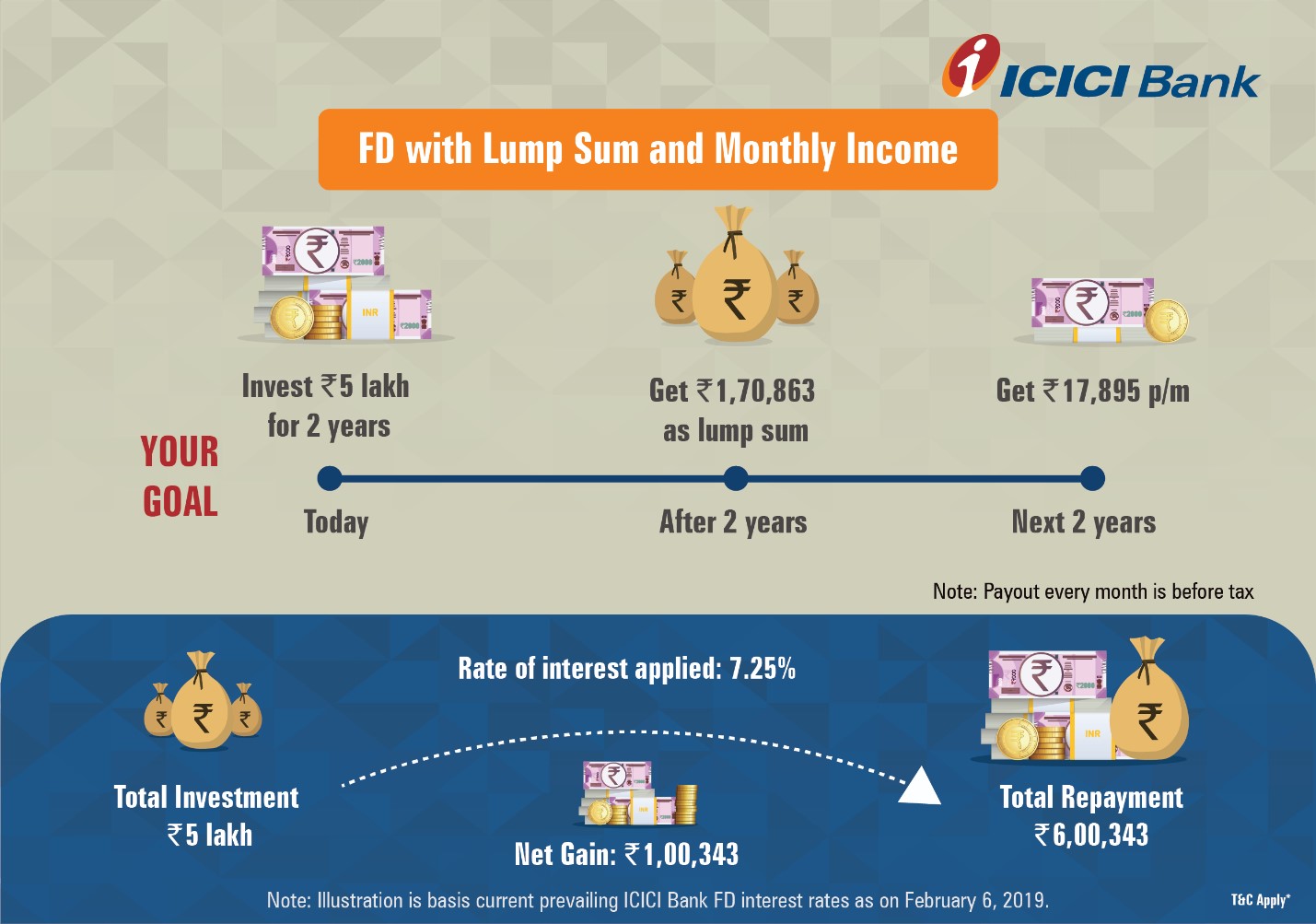

FD with Lump Sum and Monthly Income

This service enables customers to receive a lump sum amount at the end of the investment phase. The rest of the amount is available every month in the payout phase.

Example– Kalpana, a homemaker, wishes to enroll herself into a patisserie course and take her family out on a holiday. Kalpana has Rs. 5 lakh, which she invests in FD with lump sum and monthly income. Post the completion of the investment phase of 2 years, she will receive Rs. 170,863 as lump sum amount and Rs. 17,895 as a monthly income in the payout phase for the next 2 years. This will help Kalpana in going on her dream holiday and pursuing the patisserie course.

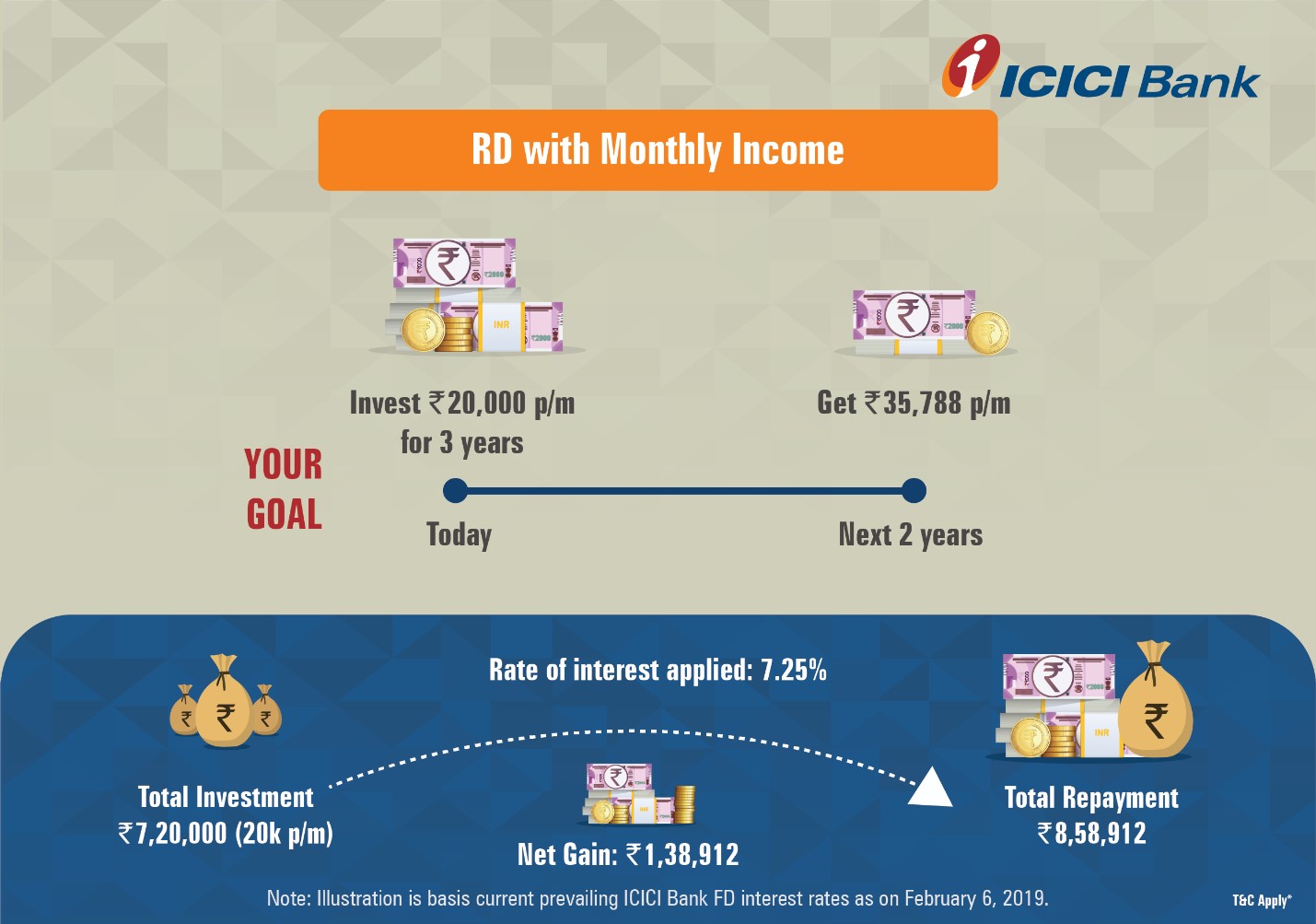

RD with Monthly Income

Designed on the similar lines of FD with monthly income, this service enables customers to meet their life stage goals by saving systematically and gaining returns as a monthly income.

Example– Satish, an HoD in a renowned college, with over 25 years of work experience is planning for his retirement. He wishes to save for post-retirement expenses and daughter’s higher education. With a steady income, Satish decides to invest Rs. 20,000 every month in RD with monthly income for a period of 3 years as the investment phase. His total investment in 3 years will be Rs. 7.2 lakh. Post the investment phase, he will receive a monthly income (before TDS) of Rs. 35,788 for 2 years, which is the payout phase. This will help him sort his finances post retirement.

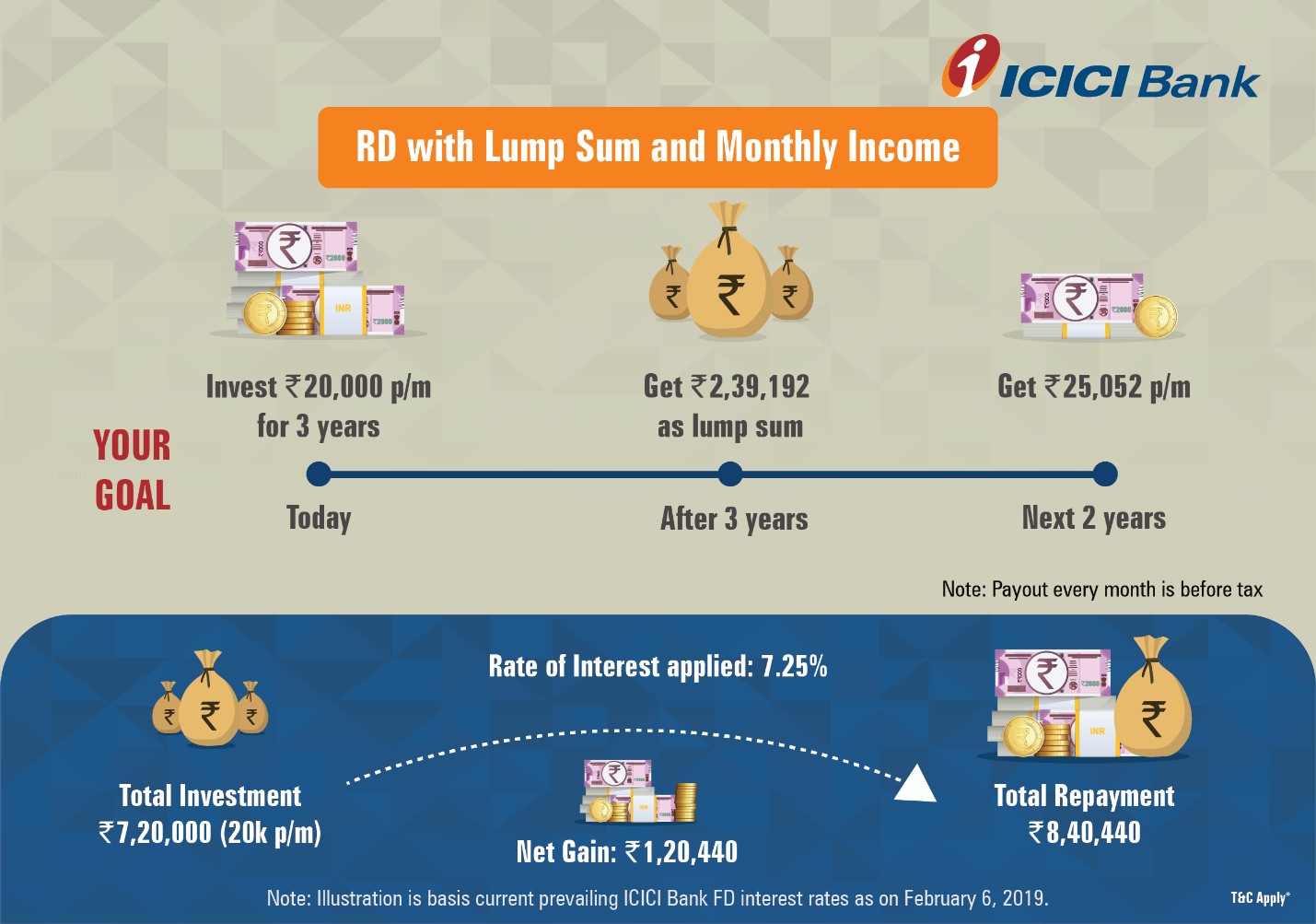

RD with Lump Sum and Monthly Income

The service enables customers to receive a lump sum amount at the end of their investment tenure and the remaining amount as a monthly income during the payout tenure.

Example– Amit works in a renowned MNC and wishes to buy his dream car in the coming years. With a steady income, he decides to save Rs. 20,000 every month for a period of 3 years using the RD with lump sum and monthly income facility. He will save Rs. 7.2 lakh during the investment period of 3 years. Post the completion of this period, he will receive a lump sum amount of Rs. 239,192 which will assist him with the down payment for the car. After which, he will receive Rs. 25,052 as a monthly income for 2 years during the payout phase. This will in turn assist him in paying the EMI for his car.

With so many investment options with FD Xtra, investors who are not comfortable with investment in SIPs, Mutual Funds, etc. can learn the tricks of the game and shift from investing in traditional options like FD & RD. The other intent behind investing in something like FD Xtra is that you can take advantage of India’s Growth Story which is currently on an upward trend.

As an investor, what are your thoughts about investing in 2019 and how a product like FD Xtra by ICICI Bank fits into your bigger investment plan? Would like to your comments…

India is one of the largest consumers for two-wheelers in the world. It might be great news for bike manufacturers, but not so much for riders. As the number of vehicles on the road increases, the probability of occurrence of incidents also increases.

Image Source

While one cannot stop the influx of new bikes on the road, an individual can minimize the chances of being financially affected due to accidents. How do you ask? Well, simply buy an online two wheeler insurance policy. It would not only offer you legal clearance, as mandated by the Motor Vehicles Act of 1988 but also offer much-needed coverage. In the event of an accident or any incident, your bike insurance will keep you financially safe.

If you renew bike insurance, make sure to purchase a comprehensive plan. While it might cost a bit more than a third-party liability policy but it offers so much more as well. When you renew bike insurance, you can choose to pick add-ons as well. Here is a list of 5 add-ons that you should include in your bike insurance.

1. Personal Accident Cover

This add-on offers health coverage and sum insured in the event of any unforeseen incidents. By paying merely INR 750 per year, you can secure a sum insured of INR 15 Lacs. The policy is quite handy in cases such as accidental death, total permanent disability or partial permanent disability. The sum insured was INR 2 Lacs earlier, but recent modifications have ensured that it is updated to INR 15 Lacs. This cover is usually included in your bike insurance policy.

2. NCB Protection Cover

The No Claim Bonus is applicable if you have not made any claims during the previous term of the policy. Most experts recommend skipping minor repairs so as to retain the NCB. However, with an NCB protection add-on, you need not worry about any such repairs. This add-on would ensure that your NCB is intact even though you make a claim.

3. Roadside Assistance Cover

If you are someone who likes to go on long rides, having a roadside assistance cover is a must. While buying online two wheeler insurance, you can opt for this add-on. Your insurance would ensure that you receive round the clock emergency services in the case of a breakdown or accident. Some common services include a change of tire, towing, refueling, getting a mechanic to fix issues, etc.

4. Engine Protection Cover

The engine is the most critical part of a bike and needs additional protection. This add-on ensures complete peace of mind by offering engine coverage. Usually, a comprehensive plan doesn’t cover the protection of engines. It can be particularly helpful for people who stay in areas which are prone to natural calamities such as floods, cyclone etc.

5. Zero Depreciation Cover

The zero depreciation or zero dep is one of the most popular and sought-after add-ons. It is a highly recommended cover when it comes to new bike owners or new riders. The add-on ensures that your insurer would consider the actual price of repairs and not factor in depreciation into it. Should you own a comprehensive plan along with zero dep cover, your insurer will pay the depreciation costs.

The Bottom line

Yes, add-ons do come at some extra cost. But if you consider the unmatched benefit that each of them provides, it is hard to ignore them. When you are buying online two wheeler insurance, you can add these to your policy and enhance its coverage several folds.

While you are at it, do not forget to compare bike insurance. When you compare bike insurance, you get the best of both the worlds. In essence, you get the best policy with sufficient coverage without paying a lot of money for the same. It would also save you a lot of time and effort, should you decide to compare and a buy bike insurance policy.

Investing to save income tax is a smart way to build wealth. With Rs 1.5 lakh every year, the current tax deduction limit under Section 80C, one can invest in ULIPs to generate returns. This way one also gets to benefit from the power of compounding. Unfortunately, many tend to postpone tax planning till the month of March and end up investing in sub-optimal schemes.

Image Source

A prudent investor should start planning early from December itself and research the investment avenues carefully, so as to settle for a plan with multiple benefits. We shall now study how ULIPs make for an ideal investment plan this tax season, benefits of ULIPs and how returns from ULIPs are computed by way of NAVs.

What is ULIP exactly?

Let’s start with the basics – what is ULIP plan? Unit linked insurance plans are hybrid products that mix life insurance, investments and tax savings. The policyholder has the freedom to choose from equity, debt and hybrid funds. We shall study the benefits of investing in ULIPs, from the tax angle and other monetary aspects.

Capital Protection against inflation – The sum assured in ULIPs is guaranteed as long as the premiums are paid, and the policy is in force. While the life insurance component is not inflation protected because of being a fixed cover-fixed tenure product, the investment portion has the potential to generate inflation beating returns, especially if an equity fund is selected. Your ULIP plans returns can create considerable wealth in the long run.

Liquidity – ULIPs are liquid after the lock-in period of five years. This is possible by redeeming units or by making premature withdrawal or surrender of the policy at a loss. Further, loans are available against the policy, depending on the type of policy tenure, its sum assured or the fund value at the time of applying for a loan.

Exit Option – One has the option to surrender or terminate the policy in case of any financial loss. However, the insurer will credit the proceeds of the discontinued policy to the policyholder only on completion of the lock-in period.

Tax Implications – Premium payment towards ULIPs are eligible for tax deductions under Section 80C with a limit of Rs 1.5 lakh in a financial year. The proceeds from the maturity or claims on a ULIP policy are exempt under Section 10 [10D] of the IT Act, 1961.

Conclusion

The correct approach to tax saving is to build wealth over a period of time. When the primary intention is wealth creation and not just saving the tax outgo, it has multiple advantages. Firstly, one picks the best suited investment scheme and secondly, this instills financial discipline in the long run, whereby regular premiums help build a corpus in the long term. A mindset change can go a long way in reaping greater rewards.

Unlike traditional plans where a sum assured decides the premium, ULIPs function differently with growth plus protection. In ULIPs, the premiums paid decide the extent of death benefit. As policies can be of regular premiums or a one-time single premium, the sum assured varies accordingly. The Net Asset Value [NAV] determines the financial performance of ULIPs. The ULIP NAV is published on the website of every insurance provider and one must do a comparison, before zeroing in on a plan. Hence, book your date with ULIP Plans this tax season and see your money grow in the long run.

The importance of financial planning cannot be emphasized more in today’s times. With rising inflation, burgeoning population with higher disposable incomes and increased consumption demand, meeting the financial goals of self and family have become of paramount importance. This opportunity of wealth creation is only possible during the working years, to provide financial protection during the sunset years of retirement and insurance cover for the family, in case of death of the earning member.

Hence, personal finance decisions need careful study and analysis of the investment options available in the market. Further, it would be more beneficial if the investment scheme has added features like minimum lock in period, minimum hassles of paperwork, inflation-proof returns, low risk instrument, withdrawal facility in case of unforeseen emergencies, flexibility in premium payment and scope for capital appreciation. We shall consider two financial instruments: ULIPs and NPS and compare both to arrive at the winner.

Meaning of ULIP

ULIP stands for Unit Linked Insurance Plan, i.e. a plan which provides wealth creation along with life cover. The name reveals itself as being a multiple advantage plan with life cover protection, income tax benefits and market-linked growth potential. We shall now study each of the features briefly:

1. Life insurance – A Unit Linked Insurance Plan [ULIP] provides life cover. This is usually the sum insured or the market value of the investment [fund value], whichever is higher. This provides financial protection to one’s family in the event of sudden death of the earning member.

2. Tax exemption – A ULIP policy provides the insured person tax benefits as follows:

a. Under Sec 80C of the IT Act, 1961, the premiums paid towards ULIP are allowed as a deduction from taxable income up to INR 150,000 in a financial year.

b. The lump sum amount on maturity under ULIPs are tax exempt u/s 10(10D) of the IT Act, 1961.

3. Attractive returns suited to risk appetite – A ULIP policy offers the investor the option to invest in either high growth equity, safe debt instruments and balanced or hybrid plans catering to diverse risk profiles from conservative, moderate and aggressive.

4. Shifting option – The investor can shift his money from equity to debt and vice versa, depending upon the fund performance.

5. Flexibility of premium payment – An investor can change the frequency of premium payment i.e. quarterly or yearly as per convenience.

How to Select the Ideal ULIP Plan

How do you select the best ULIP plan for yourself? An ideal ULIP would be one which complements the financial goals of the investor. Some of the desired features would be:

Choice of investment in a wide range of asset classes

Minimum premium allocation charge with entire premium being invested

Flexible payment structure with option of multiple premium payments

Higher lump sum value on maturity like higher sum assured, higher fund value of the plan, a percentage of premiums paid

Free switching of funds from equity to debt and vice versa, along with minimum switching charges

Meaning of NPS

National Pension Scheme is a voluntary, defined contribution pension system, introduced by the Government of India, with similar features like ULIPs, namely a market linked retirement plan with option to switch between fund managers and change allocation of fund invested between equity, debt and Government securities.

The two drawbacks of the NPS compared to ULIPs are:

NPS does not offer life cover

At the time of retirement or 60 years of age: 40% of the maturity amount has to be mandatorily invested in an annuity scheme, the monthly pension being fully taxable. Out of the balance 60% accumulated corpus withdrawn, 40% is tax exempt, while 20% is taxable.

Conclusion

After looking into the pros and cons of investing in ULIPs and NPS, it can be safely concluded that the ULIPs clearly score on the tax benefit front. Consider an example. For instance, if one has invested Rs 5 Lakh in ULIP by way of premiums and the total gains excluding the invested amount comes at Rs 20 Lakh. This means the take home is about Rs 25 Lakh. If this is withdrawn before the lock-in period of 5 years, then the entire amount falls under tax slab. However, if the ULIP is withdrawn after maturity, the entire gain of Rs 25 Lakh is tax exempt. One must invest wisely and ensure that your hard-earned money works hard for you.

It is natural to always hope for the best. Hence, when we hear of diseases or disasters, we imagine it happening to someone else, but never us. However, life works in strange ways. Thus, it is imperative for all citizens of the country to invest in a long term health insurance.

Health insurance is not an indicator of bad times, but a support when times get tough. It gives you ample cover and keeps you going during difficult times. Choose an insurance that is best suited for your age and financial capacity. This way you can be rest assured of financial help at any given time.

Why buy health insurance?

Apart from the fact that health insurance provides cover there are some essential reasons which make it prudent for an individual to opt for a policy at an early age. Let’s take a look at them.

Premium is affordable

Premium amount keeps increasing as the age advances. Considering that younger individuals are less prone to get seriously ill, the premiums for younger individuals are much lesser.

Lifestyle Illnesses

Urban lives have increased the chances of lifestyle diseases like diabetes, lung problems, heart ailments and cancer. All of these entail expensive treatments, which a good health insurance can help you with. The best insurance plans insist on yearly health check-ups giving you an idea of how you are doing.

Financial benefits

If you don’t want to face the stark truth of what the health insurance plan can be used for, think of it as an investment. If something were to go wrong, the financial strain would not fall on the family. Health insurances are good ways to avail tax benefits as well.

Employer cover

Even though a lot of employer’s do a group medical insurance for their employees, it might not be enough. Be sure to check the fine print to know what all is covered under the group policy, before you decide against going for an individual health insurance.

Waiting period

This is a very important point to remember. Most health insurance plans do not start providing actual coverage for 2~4 years. This waiting period is best to get over with at an early age, so you have the health insurance ready for you as your age advances.

No Claim Bonus [NCB] Benefit

If you do not claim for a few years, NCB adds more value to your insurance plan and thereby increases cover. You can enjoy higher coverage without actually paying for it.

Approval

If we invest in insurance early on, chances of it being approved are much higher. As age advances, companies tend to do a more detailed scrutiny to approve the insurer’s coverage.

Bajaj Allianz General Insurance

A Brand to reckon with, Bajaj Allianz General Insurance has some of the best health insurance plans in the industry. We cater to individuals of all ages and provide flexibility that is rarely seen. Some of our best health insurance plans are:

Bajaj Allianz’s Hospital Cash Daily Allowance Plan

Bajaj Allianz’s Star Package Health Plan

Bajaj Allianz Health Ensure Plan

Bajaj Allianz Tax Gain Plan

Bajaj Personal Guard Accident Health Insurance

Women Specific Critical Illness Insurance

All of these provide the following basic features, but some go beyond these standard ones as well:

Cashless hospitalization

Pre and post hospital expenses

Emergency ambulance charges covered

In-house health admin team

10% NCB which can go up to a maximum of 50%

Allowing renewability

We do hope you have got a comprehensive idea of how beneficial a health insurance plan can be. Do make an informed decision to live a happy and healthy life.