Jeet Suri does not own a credit card. He does, however own an apartment in Bangalore. It is almost bare, save for his furnished bedroom and modular kitchen. Considering the hefty furniture costs, he knows that he will need to avail of a personal loan to get his apartment fully furnished. But this is easier said than done! As a 24-year-old IT professional in a medium-sized IT firm, he has been denied personal loans twice in the past for not having the requisite Credit [or CIBIL] Score.

Image Source – Alternate Lending

Jeet has now made the decision to apply for a loan from one of the new Fintech startups that specialize in giving quick personal loans to salaried people. He applies, gets his approval within 2 hours and funds reach his account in 48 hours! Jeet himself is surprised at the smooth and quick process. And this is exactly what attracted numerous alternative lenders in the country to start online lending platforms, albeit at somewhat higher interest rates.

The Indian Banking Sector has quite a history of bad loans and non-performing properties that has made lenders [particularly public sector ones] more cautious and conventional. There are more than 1.5 million companies in the country, but banks tend to focus on lending to only to those salaried applicants working for less than 50,000 companies which are listed in their target databases. So where do the rest go for loans? This explains the rise of close to 100 alternate lenders in India in the last two years alone [India has the 3rd largest number of personal lending startups in the world, after China and the USA!].

This new breed of lenders can be broadly categorized as follows

Aggregators or Lead-Generators

Aggregators are solely responsible for generating a lead and passing it on to one, or more, banks. This is a commission-based task and they earn a fee per lead, regardless of whether the loan is approved [and eventually funded] or not. The decision to lend lies with the bank or the non-bank lender, who makes the final credit decision on the case. BankBazaar and PaisaBazaar are two notable names in this niche.

Direct Selling Agents [or DSAs]

DSAs do everything the aggregators do and some more. Aside from lead generation, they take care of the entire documentation process too, hereby assisting you in ensuring that your loan is approved. Here, too, the credit decision lies with the ultimate lender [a bank or a non-bank lender]. DSAs charge a fee to the lender, which typically ranges from ranging from 1.5 to 3 percent of the loan amount. Finance Buddha and Finwizz are two notable names.

Infographic Courtesy – Qbera

Consumer Durable Financing Marketplaces

Increased income, soaring consumer aspirations and easy cash access have prompted a sturdy growth in big-ticket purchases like electronics goods and furniture. Of the numerous schemes that have developed to fund these acquisitions, zero-interest EMIs and cardless EMIs are the most common. Astonishingly, in India, more than half of such purchases are made possible using small ticket loans from non-bank lenders! Here too, the lenders make the ultimate decision on the customer, and the platforms typically earn a commission or some sort of revenue share.

Business Correspondents

Business Correspondents take ownership of the entire life-cycle of the loan, from acquiring the customer, underwriting the loan, documentation, verification and ensuring the final loan is disbursed. The loans are funded by one of more lending partners and, uniquely, the platform plays a role in making the credit decision. They are not middleman, as they usually share risk [as well as revenues] with the bank or non-bank lending partner. Qbera is one such startup that is operating on this model

Summing it up

The online lending landscape in India is evolving rapidly. New-age online lenders are giving the incumbents a run for their money, as they partner with a variety of capital providers to test segments which have previously been untapped. Added to this, they provide a superior customer experience, which includes more transparency, a better approval rate, a convenient process and lower turn-around times. However, time will tell how many of these new-age lenders will be able to target new, profitable segments, whilst scaling their businesses with low(er)-cost capital, and do all this while maintaining the quality of their portfolio.

About the author

Nidaa Chakkittammal is a Proud feminist, former journalist, certified mountaineer and currently Content Manager at Qbera. She believes self-discovery is an eternal journey. When she isn’t drafting finance articles and blogs by the dozen for Qbera & other similar platforms, she is busy reading romantic poetry and fiction, rollerskating, participating in marathons, cycling, chilling with friends and trekking. You can find more about her on her LinkedIn profile page.

Today, India’s leading on-demand home services company, Housejoy, announced a strategic partnership with Truecaller, one of the leading communication platforms in the world, to give its users a quick and seamless one-tap on boarding experience. Housejoy has been constantly expanding their service offering and this integration would enable Housejoy to provide an easy phone number based identification as well as a trust based engagement experience.

With Housejoy’s core motive to serve the consumers with a friction-less interaction, they are constantly introducing innovative ideas to make user interface simple and convenient for the customers and the partnership with Truecaller is a firm step in that direction. Truecaller’s TrueSDK will help in instant user verification, hence simplifying the app on boarding experience. It will make the authentication swifter and secure for the users. TrueSDK has been integrated into Housejoy’s Android & iOS mobile apps and will be integrated soon on mobile & desktop web platforms too.

Commenting about the partnership, Saran Chatterjee, CEO, Housejoy said

It will help reduce a key friction point in the user on boarding process; ensuring that our customers get a secure and easy one-tap sign-up/sign-in experience via Truecaller.

A recent report by analytics platform Localytics found out that apps that asked users to sign up during the first session had 17% abandonment rates and only 41% app retention rates, Truecaller’s TrueSDK aims to bridge this gap and has become the right fit in fulfilling this critical need with its flexible and one touch phone number based authentication kit.

Speaking on the announcement Priyam Bose, Director of Worldwide Developer Relations at Truecaller said

It is critical to minimize friction for mobile focused businesses, especially during user on-boarding in mobile apps to create user delight and catalyse growth. With Housejoy, we are truly committed to offer a smooth user registration and trust based experience for millions of users.

Truecaller provides a suite of unique services such as a dialer that offers caller ID, spam detection, messaging and more. Currently, Truecaller has a 150 Million user base in India. India is now its largest market where they’re seeing explosive growth.

About Housejoy

Housejoy is the leading provider in the home services space. They are pioneers in providing high-quality on demand residential services, supported by a team of dynamic, capable and trusted professionals. Housejoy launched in January 2015 to provide an aggregation of services to customers ensuring punctuality, quality and reliability. Housejoy additionally offers specialized services in beauty and in-house bridal make-up and are expanding their service portfolio. Within a short time, Housejoy is operational in 5 cities across the nation and has raised 4 Million USD funding in series A from Matrix Partners and has raised 22 Million USD in series B led by Amazon and included new investors Vertex Ventures, Qualcomm and Ru-Net Technology Partners. For more information, please visit Housejoy

Though India is changing at a fast-forward pace, still there are some topics that are considered as Taboo and cannot be discussed online [as well as offline, especially with elderly people]. I am sure as soon as you read the word Taboo, many thoughts would have come to your mind. Some instances like buying a condom at a nearby store, shopping for lingerie, discussing openly about topics related to sex awareness, etc. do make us feel shy as well as uncomfortable. One such sector is Lingerie [for women] which is the foremost attire for women and due to the changing fashion trends, women have also become choosy about their lingerie selection.

Monica Anand, Founder & CEO of Undercover decided to break that atboo and started her line of intimate wear with an aim to make lingerie all about fashion and comfort. Monica Anand draws inspiration from everyday things and people around her. A keen observer of people’s behaviour, evolving patterns and changing lifestyles, Monica is an entrepreneur, a people’s person and an unshakeable optimist at heart. Her indomitable spirit gave birth to the vivacious range of the detachable bra brand-Switchers, which truly redefines fashion and comfort.

Born in the United States, Monica has her grounding well-rooted in India. A graduate from Mumbai University with a Post-Graduation from Symbiosis Institute of Business Management, Pune, Monica has worked with leading corporates, including ICICI Bank, TATA AIG Life Insurance and MNG by Mango, USA. Undercover has been a wonderful beginning for Monica’s work in the lingerie space. Over the last 5 years, she married her observations on the lingerie industry and the needs of the consumer to launch Switchers by Undercover. Switchers is a first of its kind modular, mix and match bra that allows the user to mix and match their bra, pushing the line from innerwear to fashion wear.

Today we have a chat with Monica Anand about her entrepreneurial journey, building the Switchers brand, the changing Lingerie segment, etc. So, let’s get started with the Q&A…

How did you come up with the idea of venturing into the Lingerie segment ?

As a consumer, I was unsatisfied with the way my lingerie interacted with my outerwear. The 2 just never seemed to complement each other. One was always worried about wearing sleeveless, deep backs, racer backs, sarees, etc. because it lead to the question of What to do with lingerie. Options available would be biting silicon straps, stick on bras on in sewn cups, all of which were decent support but no where on fit or comfort.

That’s when I thought of the need for a super comfortable bra that detaches at various places to create better interaction with one’s outerwear without compromising on fit or support. I discussed the idea and execution with family, friends and professionals from the lingerie industry before finally going ahead with the product.

Can you share some details about the team behind UnderCover/Switchers ?

Under Cover Lingerie was started by me as the sole founder. I began the company with part time support from my family and have now taken it ahead on my own.

I am an MBA Graduate from SIBM in Pune. After spending the first decade of my career in banking and insurance, I recognised a need for better lingerie and nightwear at affordable rates and created my own lingerie venture in 2011.

How much is the overall market size of online lingerie that Switchers is trying to address ?

Switchers will address women in the age group of 15~30 in the metros and T-I cities.

Discussing about Lingerie [both from men, women] is considered a taboo [or rather awkward], how did you convince your near & dear ones about your intention to venture into it ?

I wouldn’t say it was difficult, but I would say that my family was surprised by my decision. Their concerns were that I was leaving a secure job to start a business and that the business was of selling lingerie. Add to that the novelty lingerie that we began our business with. I think they all thought I was a bit out of my mind, but they were supportive none the less.

Founder & CEO of Switchers – Monica Anand

Apart from retailing on Switchers, does your team retail the lingerie collection on other marketplaces like Amazon, Flipkart, etc.

Switchers is already available on Amazon Launchpad and will soon be available on Flipkart and LimeRoad as well. We are also exploring partnerships with other online retailers who are focused on fashion.

How do you ensure that ROR [Rate Of Return] is kept to the bare minimum since women could be very picky about the size, material,etc. [and reverse logistics accounts to huge amount of cash-burn]

We ensure intense quality checks and checks at the point of packaging to minimise returns and customer dissatisfaction. This is something we had to learn from experience. We would rather discard stock with errors than attempt to pass it on to a customer. That is very damaging in the short term.

There are lot of startups like ButterCups, Zivame, PrettySecrets, etc. that are trying to solve the ‘Perfect Fit’ Bra [as well as innerwear] for the women. What are some of the USP’s that Switchers offers vis-a-vis products offered by the competitors ?

When creating Switchers by Undercover, we worked closely with our target audience to understand exactly what their issues were with respect to lingerie, in particular-the bra. Our main takeaways were:

Different occasions and outfits call for different bras, which in all likelihood will not be very comfortable or supportive.

Women with larger cup sizes find it difficult to find fun bras

One’s favourite comfortable bra and fashion bras are 2 different products

This sent us back to the drawing board. The bra has traditionally been a one-piece garment. In order to create better interaction with outerwear, we have broken it into 3 parts. The cups, the back and the shoulder straps. The roles and requirements of each of these parts is very different and taking the bra apart allowed us to re-imagine each section individually.

To understand their individual strengths and limitations. Doing this has allowed us to use processes like hand embroidery to create high fashion accessories, which completely change the look of the bra without compromising on fit and comfort, making it a great fashion statement.

Please walk us through funding of UnderCover [Self/Angel/VC] and are you looking out for external funding ?

We are currently self funded but are now exploring funding to expand the Switchers line and marketing.

Can you please talk about the top selling products of UnderCover [and does the collection also include lingerie for pregnant women/any other customer segment].

At Under Cover Lingerie, panties and baby-dolls are our best selling products. We currently retail premium lingerie for all women.

Does Switchers only have online presence or you also plan to venture into offline retail [as many e-commerce companies are now pushing for omni-channel presence] ?

Switchers is currently available on our own website,Switchers has also been selected as an innovation and is sold on Amazon Launchpad and on Limeroad. It will very soon be available on other fashion portals as well.

We are very keen to explore offline as a mode of distribution for Switchers.

Who are the logistics partners of Undercover/Switchers and is there any discrete packaging followed for the items sent to customers to keep the privacy intact ?

We have partnered with FedEx to be our courier partners for Undercover & Switchers given their brilliant delivery timelines and service. Our products are shipped discretely in plain white secure bags to maintain our customers’ privacy.

Please share some details about the customer’s age dynamics [who shop on UnderCover] and some success stories ?

For Under Cover Lingerie, our customers were in the age group of 25~45 and spread across Metros and T-I cities in India.

For Switchers, our audience is younger aged 15~30 and is essentially based in the Metros.

We have received great interest on Switchers and most of our products have been gaining great interest. We haven’t met a prospect that didn’t love the idea. We are really looking forward to the future of Switchers.

Does Switchers also provide ‘Try & Buy’ facility for it’s customers ?

Not yet, but we will be able to offer that when we go offline. The wonderful thing about Switchers though is one only needs to try the bra once, then can accessorize to their heart’s content without worry.

Monica, you have donned multiple hats [before venturing into entrepreneurship] like merchandising manager, marketing manager, product manager, etc. how much of this varied experience helped you in your entrepreneurial journey ?

Every single thing I have done till date has contributed to my journey at Under Cover Lingerie and Switchers. My experience in merchandising had obvious benefits while those as product and marketing manager have built my skills on P&Ls, ROI, marketing, brand and distribution.

Do you also plan to venture into other segments [apart from Inner-wear] and if so, please share some details about the same ?

With Switchers, we have so many ideas on the lingerie side that it will be a while before we extend the product into other segments. Although it is part of our vision, we aren’t in the position to share details yet.

We thank Ms Monica for her time and sharing valuable insights for our readers! If you have any questions for the Monica & her team about the market, impact on retail segment, entrepreneurship, etc., please email them to himanshu.sheth@gmail.com or leave your question in the comments section.

News CorpVCCEdge, India’s leading publisher of alternative investment, deals and startup news, data and information and part of globally diversified media, education and information services group, News Corp, has today released its India Quarterly Deals report for Q1 CY2017.

Capturing funding deal activities encompassing private equity, venture capital, angel/seed investment transactions for the seventeen quarters ending March 2017, the report also offers information on mergers and acquisitions with sector and region-wise analysis.

Highlights of the News Corp VCCEdge India Quarterly Deals report

PE Investments see a sober start to the year

238 deals worth $3.04 bn in Q1, CY2017 vis-a-vis 432 deals worth USD 4.19 billion in Q1, CY 2016.

Median deal value quadrupled to USD 2.25 million for Q1, 2017 compared to USD 0.6 million in Q1, 2016.

Angel investments at a 4-year low at USD 28 million with VC investments dropping by 14% YoY.

The top PE deal for the quarter was the Bharti Infratel-KKR, CPPIB deal which at USD 946 million pushed up the average deal value.

Fund infusion sees better times though investors tread cautiously

Investment values doubled against last quarter to USD 820 million for Q1 CY2017, though this was a fraction of the USD 2,500 million for Q1 CY2016.

There were no fresh investments of USD 250 million or more from investors, this quarter.

The top four fund infusions involving Oman India Joint Investment Fund II, KKR India Credit Fund, ICICI Venture Fund Management’s India Advantage Fund Series IV and IDFC Private Equity Fund IV captured a major share of total funds at USD 641 million.

Ominous times for PE funds as exit values fall

YoY, the situation seems grim with exits having fallen to USD 1.4 billion for Q1 CY2017 vis-a-vis USD 2.1 billion for the same quarter last year

Open markets dominated exit deal values at USD 945 million, bouncing back as the preferred exit route

Key exits recorded for the quarter were the Providence Equity Partners-Idea Cellular deal and the Khazanah Nasional Berhad-Apollo Hospitals deal.

Delhi NCR continues to rule the roost

At USD 1,246 million, Delhi saw more action this quarter than Mumbai [USD 692 million] and Bangalore [USD 441 million] put together.

Information Technology continued to dominate the space in Delhi NCR with 29 deals in the sector followed by 9 deals in Consumer Discretionary and 4 each in Consumer Staples and Industrials.

Coming second in terms of deal value was Mumbai with 47 deals amounting to USD 692 million, with Information Technology leading the way with 23 deals followed by Consumer Discretionary with 7 deals and Financials at 6 deals.

Bengaluru registered 53 deals amounting to USD 441 million with close to 60% being in the Information Technology space and ~19% in the Consumer Discretionary space. Pune with 8 deals to the tune of USD 62 million and Hyderabad with 18 deals amounting to USD 32 million made it to the top-5 investment destinations of India.

Vodafone-Idea deal dominates M&A space

M&A deal numbers came in at 226 as opposed to 237 for the last quarter, with the trend of a few large deals contributing to the total value continuing.

Of the total of USD 16 billion deal value for Q1 CY2017, the Vodafone-Idea deal saw a majority deal value of USD 12.4 billion.

Low median value across deals in the past 5 quarters vis-a-vis higher average deal values indicate a larger number of small ticket transactions in the space.

The Electronic Components space saw 3 deals followed by Wireless Telecommunications and Pharmaceuticals at 2 each.

Sharing her views on the News Corp VCCEdge India Quarterly Deals report, Nita Kapoor, Head India-New Ventures, News Corp & CEO, News Corp VCCircle said

PE sentiment seems to be extremely cautious and this is clearly reflecting in market performance. Appetite for risk is low with consolidation, job cuts and rollback of funding plans underway. A dip of 22% in deal values with simultaneous decline in exit figures is worrisome, though these are early days and a bounce back is possible, if not probable in the immediate future.

About VCCEdge

VCCEdge is an online financial research platform of the VCCircle Network which is owned by the global diversified media, news, education and information services company – News Corp. VCCEdge offers information on mergers and acquisitions, private equity and venture capital transactions including deal terms, structures, deal amounts and valuations. It also contains entity information on all companies involved in the transactions including target companies, investors and advisors. For more information, please visit VCCEdge

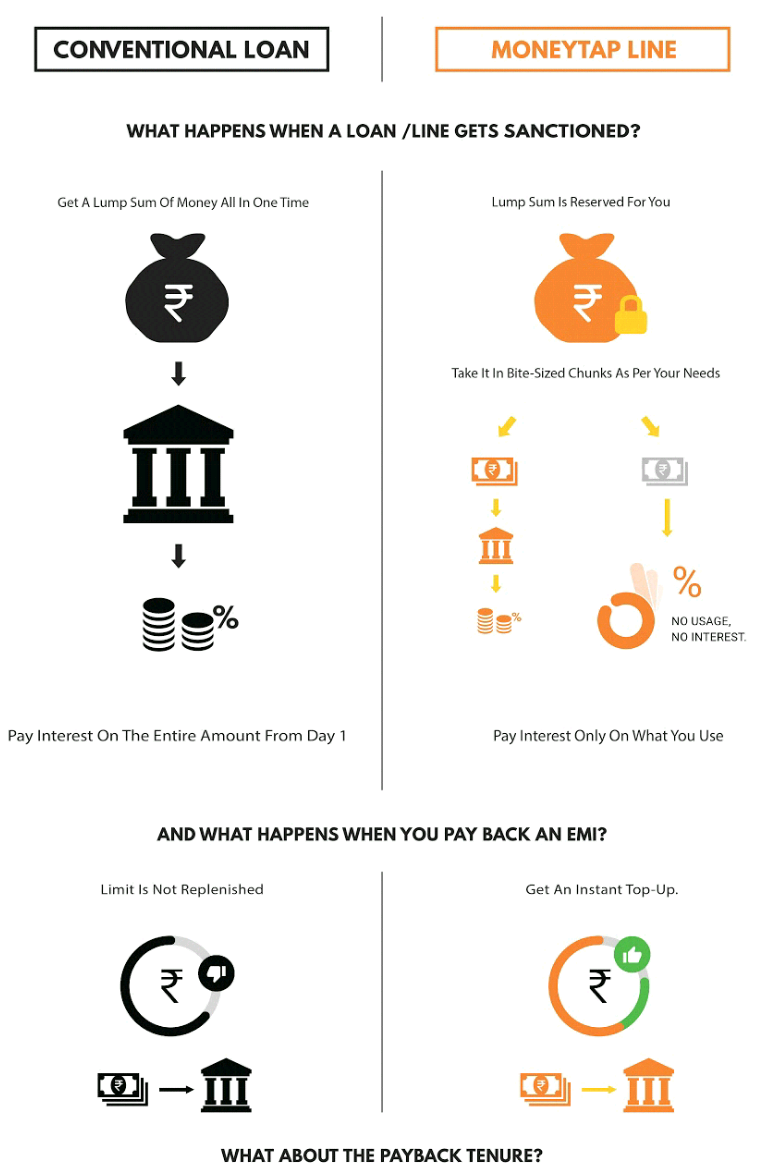

Few weeks back, we reviewed MoneyTap which is India’s first app based credit line. You can find the MoneyTap review here. As mentioned in the review, MoneyTap offers unsecured loans for salaried professionals in association with its partner banks.

Unlike P2P lending companies, the interest rate is much lesser and the loan process is fast & simple 🙂 Today we have a chat with Bala Parthasarathy, Co-founder & CEO of MoneyTap about MoneyTap, the P2P lending market, opportunities in Fintech, impact of Digital India & much more. So let’s get started with the Q&A….

How did you come up with the idea of MoneyTap ?

It was a combination of personal experiences as well as general observation. Growing up in India in the 80’s & 90’s and coming from middle-income group families, we have all faced shortage of additional funds at some point. We observed the market need and realised that the middle income group [the salaried class] has always been facing challenges with respect to credits, especially small amounts. People are not comfortable going to banks for loans for minimal amounts-this could be anywhere from Rs. 3000 to Rs.50,000 to 1 or 2 Lakhs.

Asking for money from family and friends always has an embarrassment factor. The needs are what most of us have, that could be anything from medical, birth, death, school fees, deposit to take a rent on house, etc. In many cases, people even have fixed deposits that they just don’t want to break for a small need. This is where we thought of MoneyTap and wanted to be like a friend who could be reached out at fingertips.

At MoneyTap, we are on a mission to change this and make credit accessible to those who deserve it. The ubiquitous presence of smartphones and initiatives such as Aadhaar has made it possible for us to develop a truly powerful and disruptive financial instrument. The credit line for consumers with accessibility through an app is a new concept in India and we are excited about the opportunities it can bring to thousands of millions of Indians. MoneyTap is like a friend who gives you money when in need, be it marriage, birth sudden death in family, school fees, hospital bills or sudden cash crunch during the month end. We, at MoneyTap, want to make credit available for deserving and eligible candidates.

Can you share some details about the team behind MoneyTap ?

MoneyTap is based in Bengaluru and all the three of us have been entrepreneurs before with an IIT/ISB background. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and USD 300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 [now Prime Venture Partners] where he helped create companies like ZipDial [sold to Twitter], EZETap, Happay, etc.

Kunal [ex Texas Instruments] & Anuj [ex Airtel & JWT] co-founded Tapstart that grew to 300K users and turned profitable in 2 years. They exited this venture in 2015.

What is the TAM of the consumer debt market that MoneyTap is trying to address ?

Consumer debt is growing fast in India. According to the last available consolidated data from the Reserve Bank of India [RBI], personal loans – extended by banks grew at 28.7% in 2015 and credit cards grew at 23.6%. But if we look at the actual numbers, there are just 24 million credit cards for a country of 1.2 billion! Middle income customers making Rs. 25,000 per month or more, facing frequent cash crunch for regular needs like education, medical, birth/death, etc. are not serviced by financial institutions today without putting up collateral such as gold.

Large needs, such as buying a vehicle, house, etc. are addressed by financial institutions unlike online and offline shopping. Though the latter often involves very high credit card interest rates of 40% if one doesn’t pay on time. This is the clear unaddressed need.

How different is lending based on Line Of Credit vis-a-vis P2P Lending or taking a loan [any type of loan, personal/housing/education,etc.]

We see the following major differences

1. Once a credit line is sanctioned with an upper limit, one can decide any amount of money from that limit and choose to withdraw only that specific sum from the credit line. So, if there’s an approved credit line of say Rs. 3 Lakh, one could withdraw a small amount like Rs. 5,000 or Rs. 50,000 and so on.

In contrast, a typical personal loan would force one to take the entire Rs. 3 Lakh in one shot, even though the need for money is spread over a period of time.

2. Interest would be charged only on the small amounts borrowed and not on the full Rs. 3 Lakh. Thus, if amounts of Rs. 5,000 and Rs. 50,000 are borrowed separately, then one would only have to pay interest on the total of Rs. 55,000 and not on the entire amount of Rs. 3 Lakh sum. This would have made a world of difference to a person’s monthly cash flows and overall financial condition.

The obvious contrast with a typical loan is that interest would be charged on the full Rs. 3 Lakh amount from day one. Usually a person has no choice in this scenario.

3. In most cases, the flexible borrowing options in a credit line come with the convenience of deciding payback periods for the separately borrowed amounts. Thus, for an amount of Rs. 5,000 borrowed from the credit line, one could choose to repay in 2 months and pick a longer tenure for the amount of Rs. 50,000, say anywhere between 12 months.

In contrast, a personal loan tenure would be fixed upfront with little or no flexibility in most cases. The advantage of a credit line is that as soon as EMIs are paid back, the credit line gets replenished automatically and one can continue the cycle of borrowing and repayments without needing to apply gain.

The infographic also explains how a credit line differs from a conventional loan:

What are some of the data points that MoneyTap uses in order to check whether an individual is creditworthy to be approved as a borrower on MoneyTap ?

Firstly, an individual needs to qualify the MoneyTap eligibility criteria mentioned below:

23 years and above age

Salaried individuals with minimum salary of 20,000 pm.

Credible KYC documents

Residents of Delhi, NCR, Mumbai, Bangalore, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara and Bharuch [will be launching in other cities soon]

Secondly, our partner bank check the creditworthiness of the applicant based on their credit history and thereby the applicant is approved/ disapproved basis all the steps. Once approved, their credit limit is set according to their credit history.

Few years back, there was huge wave about MFI’s (like SKS Microfinance), in 2016~17 the wave is around fin-tech sector (NBFC’s), what are your thoughts about the Fintech space in the coming years ?

Fintech will see significant growth and innovation in the next few years. Innovations like IndiaStack and deregulation in the form of GSTN, payment bank licenses and demonetisation along with a massive governmental push to move payments to digital will spur a significant growth in multiple areas in finance.

[L to R] MoneyTap founders – Kunal Verma, Anuj Kacker and Bala Parthasarathy

There is a general question with borrower, what happens if they are unable to pay an EMI on time/not able to return the money. How is the lingering question of Credit Risk taken care of ?

The same consequences of not paying one’s credit card bill or bank loans apply in this case as well. The Reserve Bank of India has nominated 4 credit agencies [e.g. CIBIL] that track an individual’s financial credit scores. If one does not repay or delay the repayment, our partner bank will automatically report it to these agencies, which will record the information. This can lower the borrower’s credit score.

Once an individual’s credit score is affected, they will not only lose MoneyTap access, but all future loan applications will be negatively impacted. He might not be able to get loans easily to buy a house, a car or a two-wheeler or get a credit-card, as all the lending institutions in the country check with these agencies before approving any loan. The bank might also initiate legal recourse to recover the money from the individual.

Can you please share some insights into the min/max loan that a person can avail on MoneyTap, interest rates, pre-closure charges, association with RBL Bank and any other details that would come in the mind of a personal availing a short-term credit

MoneyTap enables consumers to get instant credit from partner banks at the tap of a button on the app. Credit Line, a facility that was only available for businesses until now, is now being made available to consumers. The ‘Credit Line’ means that the bank will issue a limit of up to INR 5 lakhs, without any collateral or charging any interest. Against this limit, using the MoneyTap app, consumers can borrow as little as Rs. 3000 or as much as Rs. 5 lakhs and repay it as EMIs from 2 months to 3 years. The interest is paid only on the amount borrowed and the rates can be as low as 1.25% per month. The limit also gets automatically replenished as soon EMIs are paid back.

Any salaried employee can download this free Android app and in a few minutes, using a patent-pending Chatbot interface, provide all the information typically required by banks. The app securely connects with the banking systems to give them not only an instant approval but also a credit limit, depending on individual credit history.

The RBL Bank is the launch bank partner of MoneyTap. RBL’s technology enables MoneyTap to provide instant decision and instant access to money, 24/7, irrespective of holidays. Though all actions are initiated on the MoneyTap app, per RBI guidelines, all financial transactions such as billing, repayment or withdrawals will directly be with the bank using secure APIs.

As an added convenience for shopping needs, a ‘MoneyTap RBL Credit Card‘ is also provided for the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

According to your data, which is the biggest category where customers have opted for loan based on Line of Credit/MoneyTap ?

Our Top-3 categories are Wedding spends, Household related purchases and Education.

Currently MoneyTap is available only for working professionals, any time-line or plan on when you plan to open up this avenue for entrepreneurs, SMB’s, freelancers, etc.

As of now our only target is to expand our customer base among the salaried class. We have lowered the minimum salary limit for eligibility from Rs. 25,000 per month to Rs. 20,000 per month. MoneyTap now is also available for people staying in shared accommodations.

Normally Banks & other financial institutions take couple of days~weeks for KYC, how does technology [behind MoneyTap] ensure that the entire process of validation of credit-worthiness of an individual is expedited ?

The first step in our evaluation process is to understand the person’s credit profile. We are able to do this under 7-minutes on the MoneyTap app that you can download for free from the PlayStore. After that, qualified applicants who have their Aadhaar card and updated mobile number with Aadhaar, can eSign their documents so that absolutely no paperwork is required.

We are able to do this because of our advanced technology as well as the increasing adoption of Aadhaar and IndiaStack.

MoneyTap is currently present in how many cities in India ?

MoneyTap is currently present in Bangalore, Delhi, NCR, Mumbai, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara, Gandhinagar, Anand and Bharuch.

Are there are any RBI guidelines regulating the app based businesses [based on Line Of Credit] in India or to put it the other way round, is there a requirement to regulate lending based on Line Of Credit in India ?

Lending, whether they’re on an app, website or physical branches is regulated in the exact same way. There must be a bank or NBFC that meets all of RBI criteria. MoneyTap also meets with RBI from time to time to provide inputs so that the regulators can draft appropriate policies.

What are some of the things that a borrower needs to keep in mind while opting for repeated loans on MoneyTap [or for that matter any medium offering loan based on Line Of Credit] ?

Whether it is MoneyTap or not, basic rules of finance that we learnt from our parents and grandparents apply. Borrowing money to tide over medical emergencies or invest in things like education are good. Buying and spending things beyond the ability to pay it back will always have a bad ending.

In case of Loans, interest rates vary from Bank to Bank and are also dependent on external factors like market volatility, etc. can you let us know whether the interest rates are fixed on MoneyTap or whether it is like a normal loan [where for certain number of years interest rate is fixed and later it is variable] ?

A borrower has to pay interest only on the funds he uses. At the time of withdrawal, he can choose the terms of repayment, which can be anywhere between 2 months and 3 years. The repayment tenure he chooses will determine the EMIs.

The interest rate is equivalent to market rates for any ‘personal loan’ with zero collateral or security. It can be as low as 1.25% per month depending on the partner bank and the credit profile of the user.

Who are some of the competitors of MoneyTap ?

MoneyTap is the first credit line app in India. Until now the concept of credit line was present for traders through money lenders. We have introduced the concept for consumers for the first time. There is no competition that we see at present.

2016 was a tough year for startups [especially from funding point of view], how according to you should entrepreneurs deal with such adverse situations ?

Grin and bear it. Markets are always cyclical and the sky high valuations backed by even higher expectations were bound to come back to earth sooner or later. This is actually a great time to get excellent talent who are not overpaid and build great businesses.

Can you share some tips for building an effective team for startups [especially the initial core team].

There are three big rules:

Hire very, very smart people. You can’t substitute intellectual horsepower with anything else. And give them a lot of autonomy.

Smart people are rarely easy to work with. The ‘brains-premium’ is worth paying, up to a point.

If and when they get disruptive or if you made a mistake in hiring, quickly let them go. It’s better for both parties in the long term.

How important is it for early stage startups to pivot their business model [in case things are not working out as per their plan] or when is the right time to pivot ?

It is critical. But the problem with Indian entrepreneurs is not in recognizing the importance of pivoting. It is the execution of a pivot. They typically just add on the new business and keep the old one. That’s a ‘khichadi’ strategy, not a pivot strategy.

After demonetisation, there has been a huge demand for payment apps [including UPI], do you see that trend working in favour of apps like MoneyTap [that offer different services compared to e-wallet apps].

Absolutely. We are not a merchant or consumer UPI app like others. We are in the business of providing credit. UPI is a terrific way for our customers to take money out and pay back without the hassle of net-banking, etc.

Bala’s earlier venture Snapfish was acquired by HP, what according to you should entrepreneurs look for when there is interest [from other companies] for their startup getting acquired [and not acqui-hired].

Again, there are three rules for selling your company:

Good companies are bought, not sold. In other words, if you are actively out there selling your company, you will have to settle for peanuts.

You should always have multiple parties engaged, not just have one buyer.

Sell on a high note-when the company is doing great, potential buyers will extrapolate to value your company at an even more glorious future.

As per your entrepreneurial experience, when should an entrepreneur look out for external funding ?

When they really don’t need the money. It’s always the best time!

Some books that you highly recommend for entrepreneurs

There are lots of good books. The two I recommend are, ‘Zero to One’ by Peter Thiel and ‘Hard things about Hard Things’ by Ben Horowitz.

Some closing thoughts for our readers!

Entrepreneurship is not easy and not for everyone. But it is addictive and some of the most creative moments in your life will be during this journey. And there is no other [legal] way to have a huge financial windfall besides running your own company.

We thank Mr Bala for his time and sharing valuable insights with our readers! If you have any questions for Bala about MoneyTap, Fintech, scaling up, etc., please email them to himanshu.sheth@gmail.com or leave your question in the comments section.

Market research plays a critical role in the life-cycle of any business since it helps in gathering new customers and retaining existing customers. Also, collating important facts [and working on feedback] from customers helps businesses to stay ahead of the competition and deliver a WoW value 🙂

Surveys come in very handy in order to gather feedback, brand awareness, understand customer’s buying patterns, insights into business expansion [derived from the data captured via the Survey]. It can also be used to investigate the characteristics, behaviours, or opinions of a group of people [Source]. In a nutshell, surveys are an effective tool for any business since they help companies with customer satisfaction, employee satisfaction, and other related areas.

Entrepreneur Hamid Farooqui wanted to address this problem by offering customers with comprehensive, feature-rich and modern online survey maker with beautiful templates.

Today we have a chat with Hamid Farooqui, Co-founder & CEO of SoGoSurvey about the startup, online survey business, how companies can effectively leverage data from surveys, marketing, etc. So, lets get started with the Q&A…

Every idea is born out of a problem, can you please let us know how did you come up with the idea of SoGoSurvey ?

In old License Raj India it did not matter if your customers liked the car you sold to them. It did not matter what your customers thought of the after-sales service for the fridge they purchased from you. You were running a monopoly business. You would mumble something like, ‘The customer should be so excited to get his car delivered so quickly – just 4 years from the date of booking!‘

Similarly, employers did not care about the job satisfaction of their employees because the general thinking was that the employee should be happy to have a job in the first place. But post-License Raj abolition in 1991, things have been slowly changing. And in the last 10 years, things have just turned around 180 degrees. Now consumers have a choice of products-cars that can be purchased and delivered within a day, electronics and appliances with so much choice that it’s hard to figure out which one to buy.

In every category of product there is a lot of choice for the consumer and companies need to ensure total customer satisfaction or risk losing many customers due to negative publicity on social media and other avenues. We came up with the idea of measuring satisfaction using online software and thus SoGoSurvey was formed.

Can you share some details about the team behind SoGoSurvey.

I founded SoGoSurvey along with my elder brother, Suhail Farooqui. Together we bring expertise as well as experience to the table having previously founded K12 Insight, which offers cloud-based solutions to enhance communication between educators and community members, and MouthShut.com, which is India’s most successful consumer review site, considered a pioneer of the internet revolution in India.

Today, more than 70 employees constitute the SoGoSurvey team.

What is the Total Addressable Market [TAM] that SoGoSurvey is trying to address ?

We cater to small, medium, as well as large businesses that need to conduct different types of surveys such as Employee Satisfaction Surveys, Customer Satisfaction Surveys, Employee Engagement Surveys, and others to check the pulse of their customers or to know the state of their employees’ satisfaction with the company.

What are some of the standout features of SoGoSurvey vis-a-vis other competitors in the market ?

We compete with a few other players in the online survey space. Our USP is to offer a really powerful, highly user-friendly online survey software at a super-low cost. When it comes to online survey software, users have had two difficult options:

a. The affordable, low-end, low-power solution, and

b. The more powerful solution that breaks the bank

We saw a need for a tool that would be high quality but for a low cost, and that’s how SoGoSurvey was born. And that’s not all. It comes with training and extensive support that existing customers are raving about. We’re changing not just how you collect feedback in a secure, collaborative setting, but also how you fundamentally view feedback from customers, employees, and other stakeholders. Our solution is easy for the beginner and powerful for the expert. This is what makes us stand out with the competition in the space.

As far as features are concerned, here are some of the top differentiating features of SoGoSurvey that set us apart from the competition.

What is the revenue model of SoGoSurvey [Freemium/Premium] and what are some of the features that enterprise customers of SoGoSurvey get as compared to standalone users ?

We follow an exciting subscription-based freemium model. The customers can use our survey tool by signing up for a free trial account and use it for real work and then upgrade to the paid packages, if and when they need advanced features or to reach a large number of participants.

Advanced features such as Google Analytics Integration, Exporting Data to SPSS, Switch Invitations, Custom-Branded Survey URL, and Merge Surveys are a few of the options our Enterprise customers are entitled to.

How does your team ensure the authenticity of the survey results and what sort of technologies are used to ensure there are no fake reviews, etc.

Responses are collected to surveys in real time and they get updated in the tool immediately. There is no bias or tampering involved in the response collection process. Restrictions based on cookies or IP address can be set on public links, plus single-access-use links help to avoid inappropriate usage. Finally, once all of the data is in, we can also run a report by IP address to ensure that no one’s stuffing the ballot.

Since Surveys are more about ‘Decision Oriented Results’ i.e. Decisions are taken based on results obtained from the survey(s), how does the back-end logic of SoGoSurvey ensure that the organization takes the correct decisions based on those results ?

SoGoSurvey’s powerful reporting engine provides in-depth analysis and facilitates decision-making for both an organization’s clients as well as internally. First, embedding logic in the survey design ensures that participants are only asked relevant questions, resulting in the most accurate data possible. Then, reports such as Advanced Frequency, Assessment Summary, and Statistical Report help in viewing the collected data from different dimensions, giving a different perspective to problems and coming up with feasible solutions.

Set conditions and apply filters to drill down even further on results, leading to even more actionable data for specific groups and items. We know that results matter and that people are collecting data for a reason. SoGoSurvey uses these high-impact needs to prioritize features in its annual releases.

Can you please list some of the existing customers of SoGoSurvey [including SMB’s] and why startups should prefer SoGoSurvey over other survey softwares ?

Currently we cater to a lot of Fortune 500 companies as well as top educational institutes in the US. To name a few, EBay, Swiggy, Citibank, UNICEF, Marriott, IBM, HP, and FedEx are already our customers. Individuals and organizations prefer SoGoSurvey since we offer a powerful tool at a reasonable price. More details about the pricing can be found here

How many languages are currently supported by SoGoSurvey ?

SoGoSurvey currently supports 38 languages. To mention a few, we have Arabic, Bahasa, Bosnian, Burmese, Chinese, German, English [UK], Spanish, French, Greek, Hebrew, Hindi, Malayalam, Russian, Tamil, Thai, Urdu, etc.

Does SoGoSurvey provide mobile based dashboard for viewing/editing/analysing survey results ?

We do not provide a mobile-based dashboard to view survey results, but our reports can be shared with colleagues to share dynamic, real-time results no matter your device. Plus, all of our surveys, forms, polls, and assessments are mobile friendly. They render beautifully on mobile and tablet, as well as computer screens as they are optimized to let respondents participate from any platform or device.

Any plans of coming up with SoGoSurvey SDK where developers can build software that can make use of SoGoSurvey’s features, data, APIs,etc.

SoGoSurvey is SaaS-based survey software used to design and deploy surveys and later run reports. We do offer API integration to users to integrate our tool with the systems they are already using.

Can you take us through the funding aspects of SoGoSurvey ?

SoGoSurvey has been funded by family and some very close friends. The total investment in the company is about 2 million USD. We have not needed extra funding after the initial angel round as we started to see good revenue coming in by the second year of operations.

Can you share some survey creation tips so that it drives maximum results i.e. customer satisfaction KPI’s enterprises need to use while using surveys ?

Taking a survey is not a core piece of work for most and hence participant engagement is the most important thing to keep in mind while designing a survey. Here are a few tips:

a. Keep the survey short and avoid displaying progress bars, page numbers, or question numbers.

b. Use branching and question display logic to make sure only relevant questions are presented to the participant

c. Use data pre-population and piping in surveys and mail merge in email invitations to personalize the participant experience.

Couple of blogs by SoGoSurvey for more information on this topic can be found here & here.

How according to you has the internet has changed over the post Web 2.0 era and the impact social, digital, mobile, NLP, AI, etc. Have created in today’s era ?

One of the biggest changes has been user participation. Content, ideas, and information are all capable of flowing from site owner to site users. A good example of that is Wikipedia, where anyone can edit or contribute. One of the most significant changes is Software as a Service [SaaS], which developed APIs to allow for automated usage.

The trend has been shifting to collaboration and an emphasis on feeling a connection, resulting in the need for more applications to seamlessly work together. Social channels emerged with an emphasis on online communities that called on their users to add value through commenting, uploading images or files, sharing, and linking to information.

Your views on Funding – Bootstrap/External funding and when according to you should someone look out for external funding.

To fuel faster growth to the next level, we may consider venture capital investments in the future. The idea is to take funding from a VC who, along with money, brings expertise and experience to our company to fuel the growth further.

Some closing thoughts for our readers

It’s an exciting time to be involved in this industry. More than ever before, people are talking and smart organizations are listening. We are happy to be part of making these conversations happen and giving customers the data they need to make smart decisions. With the rapid pace of change, we are always looking for feedback, too, and we are always taking action to better meet the needs of our customers.

In our new release, in May, we will roll out many new features our customers have asked for. Feedback really does make a difference, and we are glad to have our customers working with us to ensure we deliver the best product at the best price.

We thank Mr Hamid for his time and sharing valuable insights with our readers! If you have any questions for Hamid & his team about the market, pricing of SoGoSurvey, SoGoSurvey for SMB’s, etc., please email them to himanshu.sheth@gmail.com or leave your question in the comments section.

After creating a multi-million dollar company, GoodWorkLabs CEO Vishwas Mudagal and Co-Founder & MD Sonia Sharma have ventured into becoming Angel Investors in 2017. They are joining the leagues of marquee investors such as Tata Group patriarch Ratan Tata or Infosys Founder Narayana Murthy, who are investing in start-ups across the country and helping to raise the maturity of the start-up ecosystem in India by the launch of their Coworking Innovation hub, GoodWorks CoWork, a design-inspired co-working incubation studio, which is located in the heart of Bengaluru’s Silicon Valley—Whitefield.

It was in 2013 that Vishwas and Sonia started GoodWorkLabs, which now a multi-million dollar company is recording a 500% revenue growth YoY. Recently, GoodWorkLabs was also ranked as the 5th fastest growing tech company in India by Deloitte in 2016. Their products are being used by 60+ million people globally.

After successfully establishing GoodWorkLabs as a boutique Software and Mobile App Development Company in India and USA, Sonia and Vishwas are excited to build a thriving start-up community through the launch of GoodWorks CoWork. Not only that, this year they are also set to mentor upcoming start-ups and extend their Thought Leadership to help businesses grow. They plan to choose three promising start-ups that have a ‘real’ business model, growth and potential and plan to invest anywhere between USD $50,000 and USD $200,000.

We were invited to the GoodWorks CoWork office in Akshay Tech Park, Whitefield and the space looks amazing. The entrepreneurial zeal is clearly visible in the design of the office, some pitcures below:

Vishwas Mudagal(L), Himanshu Sheth [2nd from Right]Q&A time with Vishwas, in the picture is Himanshu ShethVishwas Mudagal gifting signed copy of Loosing My Religion to the bloggers present at the meetup.

The New Year was a great occasion for us to try out something that we have been wanting to do for a long time. It will mark a new beginning, a new chapter in our lives and we hope to give as much as we got from the ecosystem. Bengaluru is a great breeding ground for start-ups and we are extremely excited to provide the best ecosystem for start-ups to succeed.

By working at this 3000 sq ft. co-working space, the start-ups will get access to virtual offices, dedicated and private offices, conference & meeting rooms, high-speed internet, 24/7 surveillance, storage units, unlimited beverages, in-house security and maintenance, among others. However to entrepreneurs Sonia and Vishwas who are industry leaders with a strong entrepreneurial background, the GoodWorks CoWork studio is not just a shared office space. The start-ups will also get access to technology, marketing, design and PR as well as mentorship from Sonia and Vishwas. Not only that, they will also be able to tap the network of both Vishwas and Sonia and get funding for their ventures.

Sonia Sharma, Founder and Managing Director, GoodWorkLabs said

By giving access to core services for entrepreneurs, new and old alike, such as marketing, Accounts & Finance consulting, HR and recruitment, Tech consulting, Design, UI & UX consulting in addition to other facilities, we want to dig deep into assessing and mentoring new entrepreneurs who maybe just have an idea and a business model to support it, but might have limited resources to assess its scalability & growth. Also this will help create a symbiotic ecosystem additionally helping us to choose the startups we can fund.

About GoodWorkLabs

GoodWorkLabs is a world-leading outsourced product development company that designs and builds mobile apps, software products and games for top clientele globally. With offices in Bangalore, Kolkata and San Francisco Bay Area, the company is growing at 500% YoY and has established itself as a premium tech provider for Fortune 500 companies and startups. The company is led by industry veterans Vishwas Mudagal, CEO & Co-founder, and Sonia Sharma, MD & Founder, and is a valued member of NASSCOM. For more information on GoodWorkLabs, please visit GoodWorkLabs. To know more about the GoodWorks CoWork community please visit GoodWorks CoWork

HackerEarth, leader in innovation and talent management software, is set to host the fourth edition of the India’s largest developer confluence, the IndiaHacks 2017 in association with Honeywell. The confluence is aimed at encouraging developers from across the globe and celebrating the spirit of hacking. Registrations are now open and the event will be conducted in three phases : Phase 1 [online], Phase 2 [offline-zonal] and Phase 3 [offline- final].

The code fest will be a series of four offline hackathons and one online hackathon across 3 zones. Participants stand a chance to win cash prizes upto INR 35 Lakhs. There will be two programming tracks around Algorithms/Data Structures and Machine Learning. These online challenges will have developers solving complex programming problems by using concepts of algorithms, data structures, data science, etc.

The remaining 3 will be hackathons on FinTech, IOT and Artificial Intelligence. These hackathons will see developers build unique and interesting products in less than 48 hours. Hacks will be evaluated based on parameters such as uniqueness of the idea, usability of the hack, code quality, design and other parameters.

The first stage is the Idea Submission & Online Hackathon. Participants can submit their ideas here

Each hackathon will have separate themes. Participants across the country will have six weeks to submit their unique ideas & hacks. The submissions are evaluated and the top twenty teams from each zone are shortlisted for Phase II-the zonal level offline hackathons.

The zonal hackathons will be held in Delhi [North Zone], Pune [West Zone], and Bangalore [South Zone] between 29th July~19th August. The participants will build hacks related to the theme/domain. Hacks will be evaluated on parameters like uniqueness of idea, usability of hack, code quality, design etc. The top five teams from each zone will be invited to the grand finale. More than 200 finalists are expected to be part of the final offline hackathon from September 8th-9th.

The biggest attraction of the fourth edition of IndiaHacks will be the Developer Conference in Bangalore-India’s biggest developer confluence. Along with the grand finale of IndiaHacks, the audience will be treated to a host of talks, discussions, and tech workshops by the biggest names in the industry. The event is also supported by IBM, RBS, HERE, S&P Global, Zoho and Active.AI

Sachin Gupta, CEO and Co-founder, HackerEarth said

It has been four years since we started HackerEarth and hackathons have been an integral part of our community. IndiaHacks is our annual flagship event that has been about recognizing and rewarding the hackers-the problem-solvers among us. This will be our fourth edition and we are aiming to make this a massive confluence. There will be interesting programming challenges and hackathons for every kind of hacker and developer from across the world. Through this event, we are trying to encourage programmers and coders to up their game and bring out their best.

IndiaHacks 2016 was a huge success with 1,43,000 registrations from 1500 cities in 21 countries. The developer conference had 55 speakers from various industry verticals who spoke about various topics ranging from technical to management to startups. Some of the keynote speakers included Puneet Soni, Anand Chandrasekaran, Harish Sivaramakrishnan and Viral Shah among others.

IndiaHacks 2016 also saw two of its winners Pally [Fintech] and IOTRANICS [IoT] start their own companies and get funded.

Senthil Kumar from IOTRANICS had this to say about IndiaHacks 2016

The winning moment in IndiaHacks 2016 was a huge confidence booster and an opportunity to showcase our innovation to the world. Our idea, SaveMom, was selected as best social innovation by Airmaker, a Singapore-based startup accelerator. We are happy to share that we started our company JioVio HealthCare in Singapore.

About HackerEarth

HackerEarth is the leading provider of innovation and talent management software to some of the world’s foremost companies, including Pitney Bowes, Amazon, Walmart Labs, Honeywell, and more. HackerEarth has powered innovation and talent management for large enterprises across major industries such as financial services, retail, healthcare and manufacturing. HackerEarth empowers businesses to connect with developer community to crowd-source ideas into real-life products and helps them assess technical talent for hiring. For more information, please visit HackerEarth