ofo, the world first and largest station-free bike-sharing platform, announced a new $866 million round of funding led by Alibaba Group, with participation from Haofeng Group, Tianhe Capital, Ant Financial and Junli Capital. The strategic financing presents the highest funding record in the bike-sharing industry and marks a new era for operational efficiency of the bike-sharing system.

As a precedent of asset mobilization in the bike-sharing industry, ofo uses a combination of debt and equity financing for this round. ofo will drive long-term success independently with the continuing support of leading investors.

As the global leader in the bike-sharing sector, ofo has been transitioning from a phase of rapid growth to a stage of high-quality development. ofo will continue to put our customers first and lead the bike-sharing industry with technological innovation and efficient operations.

According to the recent industry report, ofo has already achieved dominant market place globally. The service improves the urban transport environment by reducing traffic congestion, saving energy and promoting better living. It is expected that the global number of shared bike users will increase to 1 billion in the next two years.

ofo bikes in India

To date, ofo has operations in over 250 cities across 21 countries alongside widespread usage by over 200 million global users with more than 6 billion efficient, convenient and green rides, totaling to 32 million rides per day.

About ofo

Founded in 2014, ofo is the world’s first and largest ‘station-free’ bike-sharing platform operated via an online mobile application. The development of ofo platform was inspired by the concept of sharing economy and facilitated by smartphone technology, aiming to tackle ‘the last mile’ challenge in urban areas.

As of today, ofo is ramping up operations in over 250 cities across 21 countries. It generates 32 million transactions daily and has provided over 200 million global users with 6 billion efficient, convenient and green rides, which have reduced carbon emissions by over 3.24 million tons in total, the equivalent of saving more than 920 million liters of gasoline or reducing 1.55 million tons of PM2.5 emissions. For more information, please visit ofo

Mumbai based Wellthy Therapeutics, a digital therapeutics company for chronic disease management announced that it has raised USD 2.1 million in seed funding. Dr. Ranjan Pai through his family office, along with Beenext Ventures, GrowX Ventures, Currae Healthcare and other strategic HNIs like Ashutosh Taparia & Karan Bhagat participated in the round.

Self-funded until this seed round, Wellthy Therapeutics has spent the last 2 years in clinical pilots and gathering real world evidence of its solution capability, and in the process has graduated from the Merck Global Digital Health accelerator, Swiss Re’ Global and ICICI Lombard’s Nova InsurTech accelerators.

The company plans to use this funding to enhance the efficacy of its type II diabetes digital therapeutic while developing solutions for other disease areas, build deeper integrations with healthcare stakeholders in South Asia and Asia, and expand its team.

Commenting on the development, Abhishek Shah, Co-founder & CEO, Wellthy Therapeutics said

Digital health interventions are a necessity to enhance the effectiveness of current chronic disease care. Our product suite directly boosts outcome efficacy in incredibly significant ways, well beyond what current healthcare is able to do. This fund raise will help us continue to pioneer a new category of medicine that will revolutionize chronic disease care across Asia.

Dr. Ranjan Pai, CEO & Managing Director, Manipal Education and Medical Group added

Globally and in India, chronic diseases have become the largest burden on healthcare. Wellthy Therapeutics’ product suite has the potential to be the glue that binds healthcare providers, insurers, pharma and diagnostics one step closer to better patient outcomes. We were impressed with the early data of Wellthy’s type II diabetes digital therapeutic, and can see the opportunity for their solution suite to elevate the standard of care for multiple therapy areas.

As a part of this round, Siddharth Dhondhiyal will join the board as the investor representative.

About Wellthy Therapeutics

Wellthy Therapeutics is a digital therapeutics company that uses a hybrid of artificial intelligence and human paramedical coaches to improve health literacy and facilitate behavior change for better outcomes in patients. It’s first digital therapeutic for type II diabetes has been endorsed by Asia’s largest diabetes association [RSSDI]. For more information, please visit Wellthy Therapeutics

Doodhwala, a micro delivery service for fresh groceries has received a seed investment of $2.2 million by Omnivore, a venture capitalist firm,for a minority stake in the company. The hyper-local delivery platform, Doodhwala, is a subscription-based, early-morning delivery platform for all farm fresh groceries sourced directly from local farms and dairies.

Doodhwala with it’s unique model has had a tremendous momentum, becoming a well-known brand for fresh milk and grocery delivery in Bengaluru & Pune. We are evolving into the finest delivery service option for customers seeking freshness, convenience and specialty products.

Doodhwala’s unique business structure benefits customers, dairies and supermarkets. It makes farm-to-fork viable by taking over sales, marketing, logistics, and fulfillment for producers. Additionally, we are expected to scale easily due to our capital effective model, paired with the high demand for milk, and a need for regulated milk supply.

Commenting on the transaction, Jinesh Shah, Founding Partner, Omnivore said

The lean operating model, and the direct sourcing relationships that have been built, made this company stand out amongst competitors.

Doodhwala offers users a wide selection of ad-hoc everything from fresh dairy milk, meat, vegetables, fruits to shelf stable items delivered to their door before 7 AM every day. Users get the convenience of ordering on subscription basis which helps in frequent and easy purchases.

Founders of Doodhwala : Ebrahim Akbari[L], Aakash Agarwal[R]

Our unit economics are exceptionally strong. By lowering our delivery cost to Rs 3, Doodhwala is uniquely positioned in a market where other players are struggling. We have done a great job of maintaining a steady month-on-month growth rate while scoring a 85% plus customer retention.

Currently operating in Bangalore and Pune, Doodhwala has over 4 lakh month deliveries. The new financing will go towards expanding Doodhwala’s service into new markets, funding talent acquisition and upgrading technology. Reihem Roy, Principal, Omnivore will join the board.

The new funding comes less than a year after the company raised an undisclosed amount in another Pre-Series A funding from Thomas Varkey, a partner at Stonehill Capital, USA.

About Doodhwala

Doodhwala is a Bengaluru-based online grocer that is digitizing the traditional doodhwalas. Doodhwala is the only app in Bengaluru and Pune to deliver fresh farm milk directly to houses. Besides milk the start up offers a variety of groceries, fresh poultry, veggies, fruits and household essentials at MRP. Founded in 2015 by Aakash Agarwal and Ebrahim Akbari, Doodhwala, is present in Bengaluru and Pune. For more details, please visit Doodhwala

We are honoured and humbled to have received this recognition, which is testimony to the fact that a passionate team, that sets out to solve real issues and doesn’t deviate from its vision despite market forces, makes for a successful organisation. Our drive and commitment to transform the grocery delivery industry in India is relentless and year 2018 will be a transformational year for Milkbasket and the industry.

The Startup of the Year award is dedicated to young SMEs, aged seven years or less, with great potential to become big in local / international markets. Considered as the most coveted awards show complementing the league’s best across SMEs, SMB and new and emerging small scale ventures, Small Business Awards 2018 were organised by Franchise India Group. The award ceremony was hosted in New Delhi.

About Milkbasket

Launched in early 2015, Milkbasket is India’s first and largest daily micro-delivery service. Built on the unique Indian habit of getting fresh milk delivered at home every morning, Milkbasket is today fulfilling the entire grocery needs of a household everyday before 7:00 a.m. To enable frequent and frictionless buying, Milkbasket has innovated flexi-ordering and contactless delivery – both a first in the ecommerce industry – and favourites of Milkbasket customers. Founded by INSEAD alumnus Anant Goel with his co-founders Ashish Goel, Anurag Jain and Yatish Talvadia, Milkbasket delivers only in select areas while expanding its network with new launches every week. With an order fulfillment rate of 99%, customer retention rate of 95% and on-time deliveries of 99.9%, Milkbasket has redefined the industry benchmarks and enjoys envious customer loyalty. For more information, please visit Milkbasket.

A very famous quote on investing says – ‘Risk & Rewards are two sides of the same coin’. This means that in most of the cases, higher the amount of risk involved chances of maximizing the returns are also very high! The investment portfolio of every person would differ since it is dependent on various factors like risk appetite, assets, liabilities, dependencies, etc. and hence, it becomes virtually impossible for any investment firm to cater to varied investment requirements of such a large audience.

This is where emerging technologies like Machine Learning and Artificial Intelligence can play a vital role in creating a tailor-made investment plan based on your long-term and short financial requirements. Machine Learning has already the paved way into the Fintech market, be it approving loans, documentation, managing assets, etc. Many Fintech startups are leveraging machine learning, AI, Chatbots and helping banking institutions to either enhance the existing banking experience or creating kick-ass products in the areas of wealth management, personal finance, customer service, etc.

According to a report by Bloomberg, less than 1.5% of the Indian population invested in equity markets and only 2% of India’s household savings were exposed to equity. However, there is a rising interest to invest in financial instruments like Mutual Funds if they are given proper guidance.

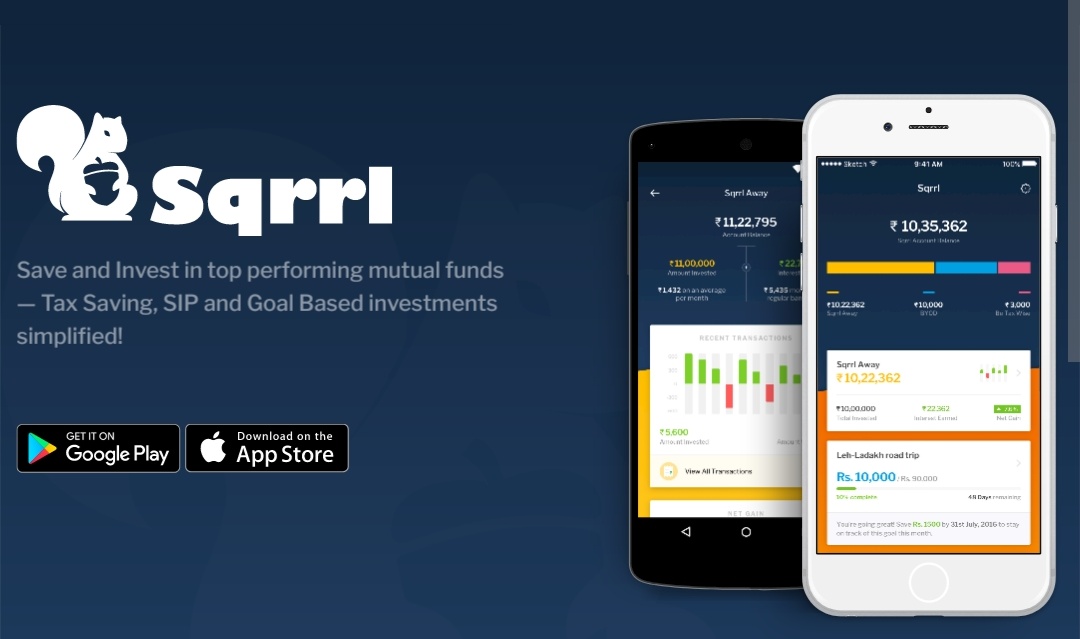

This is the problem being solved by Sqrrl, a Fintech startup that was incubated at Reliance GenNext Hub and seeks to help young people save & invest in Mutual Funds in a hassle-free manner. Sqrrl also recommends great tax saving investments for its customers, keeping in mind a seamless experience. All this with the aim to help young Indians financially prosper! Today we have a chat with Mr. Samant Sikka, Founder of Sqrrl about the app, Fintech, Personal Finance, etc. so let’s get started with the Q&A…

How did your team come up with the idea of Sqrrl ?

Having spent almost two decades in financial services domain one was constantly exposed to challenges of building distribution in a country as diverse as India. I was always intrigued by the fact that in spite of six decades since independence financial services ecosystem was still struggling to provide access of financial services to its citizens. To my mind the single most important reason that came in the way of expanding financial services footprint was ‘Unit Economics’. Unit economics basically dictated who got access to financial products & services and also which type of products got sold.

Sometime in 2015 I started to absorb the impact that culmination of technology & internet was starting to have on democratizing ‘access’. E-commerce was starting to grain traction and people started getting access to goods and services hitherto restricted to larger cities and towns. 2 things stood out, given the economic prosperity over the 2 decades people had both aspirations and means to consume and were demanding better experiences. Internet had started to travel deeper in the country and social and digital were starting to have an impact on consumers behavior and consumption patterns.

Meanwhile, silently but surely there the impact of #RegTech and benefits of India Stack which were started to make tremendous traction on the two biggest friction areas in financial services, on-boarding & payments. The timing seemed to be just right neither too late neither too early.

Can you take us through the founding team of Sqrrl ?

Putting the challenges & opportunity together gave birth to the idea of Sqrrl. The vision being to build a digital platform aimed at millennials with an Initial offering is around savings & investment products powered by Mutual Funds and will expand to Loans, Insurance, Payments ultimately aspiring to morph into a digital bank. The idea aligned the founding team which brought wealth if experience & complementary skills sets .

Sqrrl is an interesting name for a ‘Fintech startup, how did you zero in on the name and how does the brand ‘Sqrrl’ get along with the moto of ‘building financial literacy among Indians’ ?

Sqrrl name was chosen with care. The animal embodies certain character that we stand for

Doer and Prudent,

Natural Intelligence,

Hi-Energy-Active-Nimble,

Saver and plans for future. hoards for winters in summers,

Good at balancing work & play,

Social

What is the TAM of the Fintech market that Sqrrl is trying to address ?

India’s Asset management Industry has grown at a CAGR of 21% over the last 17 years [ 2000-2017] is expected to grow to USD 700 billion by 2022.

Sqrrl aspires to be amongst the Top 10 players by 2022 with an Asset Under Management [AUM] of approx USD 14 billion and 12 million customers

There are number of Fintech platforms that are targeting a similar problem [as well as market], what according to you are some of the core USPs of Sqrrl when compared to its competitors ?

Sqrrl is different from existing players in many ways. Important ones are highlighted below:

Sqrrl has a customer persona which is in the age group of 25-35 years, salaried class, upwardly mobile and digitally savvy.

Sqrrl is a not a marketplace unlike many others. We personalize investments needs of individuals and match them with funds available in the industry.

Can you please walk us through the funding of Sqrrl ?

We have been bootstrapped from beginning of our journey. We are currently in funding raise discussion of about 1M USD with some VCs.

Once user has created an account on Sqrrl [and all his investments from various AMCs are under one window], what other services does your team provide to the investors so that they can get more returns from their investments ?

Sqrrl keeps monitoring all of the funds recommended by its team. We stay with our customers in their investment journey and keep guiding him with right decisions from time to time.

Can you give a small glimpse about the tech behind Sqrrl ?

We are app only offering on iOS and Android

Our API layer is powered by Python [Falcon framework]

Our database is AWS RDS on PostgreSQL

Other than this we use many third party APIs

Sqrrl is currently limited to Mutual Funds, are there any plans/timeline on whether it would be expanded to cover other financial instruments ?

Yes, we have plans to launch loans and insurance products in future.

What are some of the methodologies that your team use in order to keep the investors hooked on to the platform ?

We have a way to connect with customers in 360 degree way. Our customer success team keeps talking them on Email, Phone, SMS, Whatsapp in addition to in-app communications.

Sqrrl was incubated in Reliance GenNext Hub, how was the experience in the accelerator program and how did the program help your team to validate & scale the startup ?

The program was really of great help in helping us with product market fit study and beyond. They really helped in methodical product market fit. In addition to product market fit, customer traction strategy and its execution planning was done with them.

Are there any setup charges or any other charges that customers have to pay to use the Platform ? Do you charge any withdrawal or closure charges for the Sqrrl’s recommended funds ?

There are no setup charges to use Sqrrl. However there may be early withdrawal charges for some funds before initial lock-in period.

Which are some of the AMC’s that are currently on-boarded on the Sqrrl platform ?

There are 17 AMC that are there with Sqrrl. It covers 91% of the industry AUM

As you have mentioned earlier, Sqrrl aims to encourage Indians to save more. There are various investor initiatives like #MFDayon7th by Reliance MF and CNBC TV18, does Sqrrl have plans of starting an investor education initiative [or something else] in order to widen the horizon of passive investors [that could be an integral part of the investors eco-system, but don’t know where to get started] ?

The ecosystem is doing a great job in educating investors. AMFI is doing great job in communication like ‘Mutual Funds Sahi Hai’. AMCs themselves have different plans. Sqrrl plans to use these and some of its own to launch education awareness. We are working on them.

Many fintech companies, namely PayTm [or PaytmMoney], FreeCharge, PhonePe, etc. are planning to have boutique of finance products on their platform, does this growing competition have an impact on a startup like Sqrrl and how it would the competition result in expansion of the fintech ecosystem ?

It is good that this space is getting its validation by entry of bigger players. There will always be space for early movers like Sqrrl based on its customer service differentiation.

Can you comment on the ‘Customer/Investor’ demographics that are currently using the Sqrrl Platform ?

90% of the users are under age 40 years.

61% of the users are from B15 [beyond top 15] cities.

We have coverage from over 700 cities of India.

What is the revenue model of Sqrrl and does it follow the Freemium model ?

We get distribution fee from the underlying Mutual Funds.

Along with the integrated AMC approach, building investor portfolio as per his requirements, etc. does your team also provide advisory services ? If not, what are some of the services that you plan to offer in future [especially with the Mutual Fund Products] ?

We are not providing advisory services now but we are open to embrace this in future.

How Fintech is shaping up the Financial Eco-system in India and how technologies like Blockchain will bring the next wave of Fintech revolution ?

Blockchain and its acceptance is in very early stage. Most of the work is happening in Crypto exchanges. We are open to exploring something on blockchain which is widely accepted.

Some books that you highly recommend for entrepreneurs

Zero to One by Peter Thiel

The Lean Statup by Eric Ries

Traction : How Any Startup Can Achieve Explosive Customer Growth by Gabriel Weinberg

Some closing thoughts for our readers!

As Bill Gates says, ‘If you are born poor its not your mistake, But if you die poor its your mistake.‘ Sqrrl is a platform available for every Indian to manage their money.

We thank Mr. Samant Sikka for sharing his insights with our readers. If you are planning to put your money to work via smart investments, then you should download Sqrrl. If you have any questions for Samant or the Sqrrl Team, please email them here or share them via a comment to this article.

‘Ownership’ is a word that has a lot of sentiments attached to it. Whether it is owning a commodity like a car, bike, mobile phone, electronic appliance, etc. or owning a house, it brings a deep sense of accomplishment to the owner. Many years back, owning either of them would be considered a herculean task, but with the rise in urbanization, increase in the overall disposable income of the urban Indians, changing lifestyle and easy access to financial tools [like Equated Monthly Installment], the rate of consumption has increased rapidly.

If a consumer has a good financial track record and an exceptional CIBIL score, getting a home loan/personal loan/vehicle loan is a piece of cake and consumers can pick and choose from the best possible options, since financial institutions do not want to lose the customer and they would try their best to retain/bring a new customer on board. However, EMI comes with a baggage full of responsibilities and missing the EMI on a consistent basis can have serious implications on your financial track record. In some scenarios, you might be looking for a short-term loan or a relatively smaller amount for which you might not want to take a bank loan. In such scenarios, you either lend money from family, friends or from companies operating in the burgeoning fintech sector.

The overall financial landscape is also changing at a very rapid pace in order to accommodate the changing sentiments of the customers. Innovations like Unified Payments Interface [UPI], India Stack, India Chain, push towards Digital India, increasing internet penetration, etc. have resulted in many innovations in the Fintech Space. Though startups catering to Payment services [PayTm, FreeCharge, PhonePe, etc.], P2P Lending [LendBox, EasySalary, etc.], Personal finance [BankBazaar, Capital Float, ScripBox, etc.], Lending based on credit-line [MoneyTap] have resulted in major customer and investor interest, there is still a lot of room for innovation in the fintech sector. In many cases, Banks and Fintech players are working together and utilizing their relevant expertise to create a better experience for their customers.

#SmartlyOwn – Better Option to Own Things

As reiterated earlier, ownership brings a sense of pride, but it comes at a cost. Though consumers have options to buy furniture, bike, electronic appliances, etc., by utilizing the financial services of banks as well as fintech companies, they still have to worry about repaying their loan on time. Unlike in the past, young population is more comfortable to switch cities in case they find better career opportunities. In case they opt for relocation, they need to take the important decision on whether they carry the commodities they own like car/bike/electronic appliance along with them or sell them at the best possible price. Since each of these is a depreciating commodity, hence their overall value depreciates from the very moment you own them.

Hence, consumers need to take the important decision on whether they need to own them or use options like ‘renting’ so that they can save money and #SmartlyOwn the items. This is the problem being solved by new-age rental companies that are using technology to offer better options to their customers. Even if you own a house, you still need to worry about setting up the home and good home interiors might burn a hole in your pocket. L Rather than blowing up hard-earned savings in owning up such items, the millennial generation has better investment options like Mutual Funds, Stocks, CryptoCurrency, etc. Due to all these factors, many urban Indians are switching to a #SubscriptionLifestyle since they have options to rent bikes, appliances, furniture, etc.

RentoMojo – Consumer Leasing Company to a Fintech Startup

Rentomojo, India’s leading consumer leasing company has various plans so that customers can buy a bike, furniture, electronic appliances on rent for a minimum period of three months. Founded by IIT alumnus Geetansh Bamania, RentoMojo is a first-of-its-kind consumer product leasing business that raises lease-capital from financial institutions for products rented to consumers for long-term periods, typically 12-18 months.

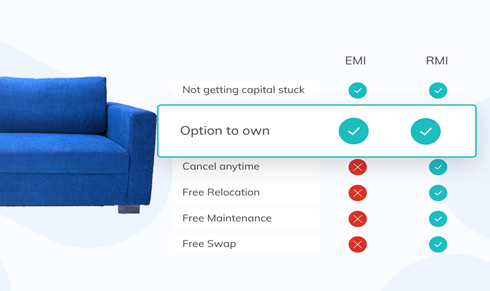

With an option like Rental Monthly Installment [RMI], you can own a product like a piece of furniture, a bike or an appliance without being bonded with a lifetime commitment. How is RMI better as compared to EMI? There are so many benefits that come along with it, which are not available with EMI and flexibility and non-commitment to the products is the biggest of them. You can take the products till the time you want and return when you don’t. The other important benefits include free delivery and maintenance, a swap of the products and much cheaper payouts monthly as compared to EMI. This is how the concept has broadened to a wide universe of the customers who have always considered renting as a financial decision.

Since many customers rent products for a long-term period of 12~18 months, they might want to increase the rental tenure or own the products as well, making a lot more financial sense. This is the thought with which they announced an exciting proposition of Rent-to-Own [#RentToOwn], where now the customers will be able to rent till whatever time they want, return or own the products. This is a whole #NewWayToOwn!

#RentToOwn – A Smarter Way to Ownership

Though it was started as a rental business, Rentomojo has evolved as a fintech model where the customers can lease furniture, appliances, and two-wheelers by paying an extremely affordable RMI. With the new offering of ‘Rent-To-Own’, the customers will have a new way of ownership, where after paying some RMIs if the customer feels like buying the products, it can be done. Customers also have an option where they can ‘try and then buy’ through product trials at their doorstep.

Eminent content contributors were invited for the launch of this event where the idea and concept was introduced for the first time to a larger audience. Sharing his views on being the first fintech startup to have this feature, Geetansh Bamania, Founder & CEO of Rentomojo, said

Usually renting is considered for a longer duration. A lot of customers also get a strong sense of ownership once they buy the products. What we also realized that, although the perception of renting could be for a smaller duration, the average rental tenure of our customers is 12-18 months, which itself makes us very different than a typical rental model. With an option of owning if the customer wants to after he has rented, where he is paying a nominal RMI, is a new way of ownership.

The below table summarizes the advantages of RMI as compared to EMI and ‘Option to Own’ is definitely a feature that would lure customers who rent for a longer duration since they now have an option to own the item they have been using on rent!

Some of the questions asked during the launch event were:

Should customers opt for renting items even if they have the financial capability to own them?

Since Rentomojo provides ‘Free Maintenance’, how does it educate its customers about product quality so that maintenance expenses are kept to the bare minimum?

Who are the partners of Rentomojo in the bike, electronics appliance sector?

Does Rentomojo plan the omnichannel route in future so that customers can also get a touch and feel of the products [especially the furniture]?

Does Rentomojo service only the B2C sector or they also have B2B customers?

What are some of the unique offerings of Rentomojo as compared to other companies operating in the same sector?

Geenatsh Bamania explaining the ‘RentToOwn’ concept

Geetansh and his team answered all these questions with ease since they are very confident about their offerings. Since their team has extensive experience in technology, e-commerce, retail, their main focus has been on unit economics rather than chasing a vanity metric like Gross Merchandise Value [GMV].

What are your thoughts about the RentToOwn concept? Do leave your feedback in the comments section.

Eduvanz Financing Pvt Ltd, a skill development loan provider, has announced that it has been granted the NBFC Licence by the RBI to start providing Loans in the multi-billion skill development sector. The Firm has raised $500,000 investment led by Blinc Advisors. Eduvanz will utilize the funds for strengthening it AI based Lending technology for loan appraisal and expands its operation pan India.

Eduvanz is a pioneer in using proprietary AI-based algorithms and complex predictive analytics to collate financial & socio-economic data from conventional and non-conventional sources to make lending easier for skill development. A successful pilot phase where over 12000 leads worth over $8 Million were assessed to fund over hundreds of students, Eduvanz has validated its concept.

With the non-banking financial company [NBFC] status approval from the Reserve Bank of India [RBI], Eduvanz is bringing much needed financial support in the Skill development ecosystem using analytical tools and advanced risk management capabilities to extend loans without any paperwork in a matter of minutes.

Varun Chopra, Co-founder, Eduvanz Financing Pvt Ltd, said

We are solving problems that are directly linked with nation building and growth of Indian Industry. Over the next four years, more than 200 million Indians will undergo some form of skill training before they enter the work force. At Eduvanz, our mission is to financially empower every individual to chose the vocation, skills and career of their choice.

With this approval from RBI, Eduvanz has moved one step closer to becoming India’s leading lender for vocational courses, on-job training programs and certifications programs.

??Eduvanz works with Training Partners, Top Corporates and Certification Providers spanning more than 16 Industry Sectors to increase their enrollments by providing innovative financial solutions to students and skill-seekers looking to skill up for their careers.

About Eduvanz Financing Private Limited

Eduvanz is a innovative finance company, which is completely revolutionizing the educational loan market. Eduvanz has won the the Judges Award at the Wharton Indian Economic Forum’s Startup Challenge where it competed with over 500 other start-ups. For more information, please visit here

India’s leading mobile health and fitness platform, HealthifyMe, have raised $12M Series B round of funding led by Sistema Asia Fund, the India focused fund of Russia’s largest Conglomerate. Silicon Valley based Samsung NEXT, Singapore’s Atlas Asset Management and Japan’s Dream Incubator are the other participants in the latest round of funding alongside existing investors IDG Ventures India, Inventus Capital, Blume Ventures and Dubai based NB Ventures. The Rainmaker Group was the advisor to the company on the transaction for which the term sheet was signed in October 2017.HealthifyMe has grown 3.5 times in 2017 to 4 million users, spread to 200+ cities, and is booking US$ 4.5M in ARR [Annualized Run Rate] revenue. With more than a million monthly active users, HealthifyMe enjoys about 10% of the Indian market share in the health/fitness category as per AppAnnie. HealthifyMe users have tracked 200 million foods, workouts and exchanged 10 million messages with their nutritionists and trainers.

Learning from this, HealthifyMe launched the world’s first AI nutritionist ‘Ria’ in late 2017, which is now guiding its paying consumers alongside human nutritionists and trainers. The HealthifyMe app itself has also become the highest rated app on Google Play in India achieving a rating of 4.6 and Google’s Best app of 2017 recognition – third year running.

HealthifyMe intends to use this fresh round of funding to deepen its presence in India by offering health foods, diagnostics and insurance products beyond its digital nutrition/fitness services portfolio. HealthifyMe also hopes to enter other emerging markets. The company recently launched in the GCC [Gulf Cooperation Countries] market and is already in the top 3 on Google Play, UAE. Additionally the company intends to use the funds to further its AI and Data Science capabilities.

Our vision is to build the world’s largest online health and fitness service. We want to help millions of consumers achieve their goals by engaging with nutritionists and other health experts empowered with Artificial Intelligence. ‘Ria’, our AI nutritionist that we introduced last quarter will have a game changing effect on fitness/nutrition access to Indians. We are already India’s go-to health app, this funding will help us to launch in other emerging markets where obesity and lifestyle diseases are growing exponentially. It will also help us expand our offerings portfolio to affiliated products and services that our customers need.

We are strong believers in preventive healthcare. People all over the world associate healthcare mostly with disease treatment, but ideally healthcare should prevent diseases. HealthifyMe team is disrupting this vitally important sector with its technology platform, transforming everyday behavior of people, and measurably making them healthier. We are happy to back the company in its mission.

HealthifyMe is the leading digital health app in India, and a very compelling mix of both human and machine intelligence. Its network of coaches helps users stick to their diet and fitness plans, the AI they have developed helps the coaches be more efficient. We were also impressed with the sheer amount of data the company has gathered, including the database of Indian foods.

HealthifyMe was co-founded by Tushar Vashisht and Sachin Shenoy who worked previously at UIDAI [Aadhar, Govt of India], Deutsche Bank and Google across India and Silicon Valley. The HealthifyMe app is available to download for free and enables users to keep a track of their calories, set personal fitness goals and measure progress. It boasts of the world’s largest database of Indian foods and syncs with all leading wearables, Google Fit and Apple Health. As part of its subscription services, HealthifyMe connects users with qualified nutritionists and trainers who review their progress, provide diet and exercise plans and work with the users to help them achieve their fitness goals.

HealthifyMe also has curated a digital workplace wellness program and has worked with clients such as P&G, Unilever, Accenture, Cognizant, Shell, Philips amongst others. The Company also works as a digital/preventive partner for top healthcare providers in India like Medanta, Manipal, Apollo ACODE etc. In early 2016, HealthifyMe had setup its global headquarter in Singapore and received Series A funding of US$6 Million led by IDG Ventures India, Inventus Capital, Blume Ventures and NB Ventures.