Transacting has come a long way from bartering an item for another to buying everything on credit. Credit used to be a luxury that was provided by vendors, only to customers that had a long history of buying from them.

However, with the evolution of the banks, the availability of credit has expanded, from being provided to select customers by the vendors to customers being backed by banks for all their purchases from all vendors.

This facility provided by the banks is offered through credit cards. A bank provides this facility to almost all its customers with different spending limits, depending on their accounts’ balances and longevity of the relationship with the bank.

Evolution of the credit card

The first token to allow someone to buy stuff on credit was issued in 1947, known as Charg-It, and was accepted at multiple stores in specific areas of Brooklyn. It was a status symbol to have owned this card.

The idea gained momentum particularly with the traveling salespersons going for the Diners Club cards in 1949. It allowed them to travel without having to carry cash for food, fuel, and hotel stays. They were able to use this card only at network outlets though.

Looking at the phenomenal response that Diners Club cards got, banks as well started issuing such charge cards. In 1950 American Express charge cards were launched. Learning from their experiences and expanding aggressively, the charge cards are changing the way we transact, the world over.

The global expansion

In order to push the use of charge cards, the Bank of America mailed a plastic charge card to all its customers in Fresno, CA with a credit limit of USD 500 each. A lot of these were stolen and/or misused, thus creating huge losses for the bank. The experiment came to be known as the ‘Fresno Drop’ and was not a complete failure though. It was a learning that highlighted the security issue and propelled the evolution of the cards with higher security.

The present-day chip and credit card pin is the most secure and accepted mode of payment.

The Indian market

Up until the last decade, carrying out cashless transactions was a luxury, enjoyed only by a select few who were educated enough to understand how it worked and owned cards. The use of plastic money has been consistently on the rise during the last decade; however, it got a boost post the demonetization rolled out by the ruling government in 2016.

The cards are increasingly used for most online transactions. Additionally, people swipe their cards to pay for fuel, groceries, and other daily items. Several institutions offer special rewards points program for increased usage. The Indian population has come a long way from the barter system to the plastic money especially with the government promoting digitalization in the country.

The card culture has penetrated urban India but still has a room for expansion. Rural India is a vast untapped market that is still reluctant to switch to plastic money. Don’t have a card? Apply for one today and enjoy the freedom from paying in cash.

There is a very famous saying when it comes to investing – ‘Never put all your eggs in the same basket,‘ which in simple terms means that you need to have a diversified investment portfolio. Higher the risk, higher are the chances of yielding better returns, but as an investor, you need to formulate the entire plan based on various factors like age, assets, liabilities, existing investments, risk appetite, etc.

We are always on the lookout for investments that would give the maximum ROI [either in the short-term or long-term], but in some cases, you need to park aside the factor of ‘short-term gains’ and opt for an investment plan that can safeguard your near & dear ones when you are not around. There are pure play ‘Term Insurance Plans’ that provide insurance for a certain period of years, and the payout is done only if the policy holder is no more. However, what if there existed a plan that is an amalgamation of the two worlds – Term Insurance and Wealth Creation?

When we talk about investments, we cannot rule out the role that ‘technology’ is playing in every aspect of the spectrum – financial planning, tax saving, insurance, etc. Renowned financial institutions are now leveraging the power of AI, machine learning, deep learning, etc. in order to serve the digitally savvy investors who now seek to manage their money in a digital world. Rising internet and smartphone penetration, push for Digital India, rise of Fintech are some of the factors that contribute to the growth of the overall financial sector. Financial companies are becoming more agile to meet the changing needs of digitally savvy young investors by rolling out products to that particular market segment!

We had earlier hinted about a product that is an ideal fit from investment as well as insurance point of view. Edelweiss Tokio Life has come up with an #Unyakeenable Unit Linked Insurance Plan [ULIP] called the Wealth Plus Plan.Whether it is about securing your child’s future or saving for long term, Wealth Plus has the answers. So, let’s delve deeper into features of Wealth Plus, its benefits, etc.

Wealth Plus – High Level Features

Wealth Plus from Edelweiss Tokio Life is a market-linked insurance plan aimed at digitally-savvy customers. It is an industry-first product that is aimed at wealth creation and has no premium allocation & policy administration charges. The only assurance that the company needs from its customers is:

Paying the premium on time, and

Staying invested.

As a percentage of Annualized Premium, there is additional premium allocated on every premium paid and that increases over a period of five years. Additional 1% allocation is added with every premium installment in the first 5 policy years.

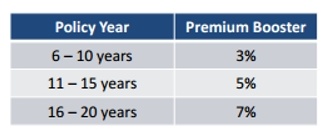

Another useful feature of the Wealth Plus is the ‘Premium Booster’. Premium Booster is added at the end of each year starting from the 6th Policy year till the end of the Premium paying term.

The reason why the company advises it’s investors to stay invested for a long term is that over a 20-year premium paying term, 80% of the one-year premium is reinvested via additional allocation. This means that a major portion of your premium is being paid via the interest earned on the earlier premiums paid by you.

Wealth Plus – Investment Strategies Suited to Your Requirements

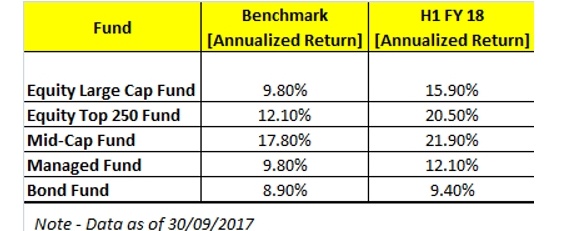

Investing in any fund becomes less beneficial if there are stringent terms associated with the fund. However, in case of Wealth Plus, the investment terms are very flexible, and the policy holder is free to invest the premium in any of the available funds based on his/her risk appetite. This is termed as the ‘Self-Managed‘ option. The funds available are below:

Equity Large Cap Fund

Equity Top 250 Fund

Equity Mid Cap Fund

Managed Fund

Bond Fund

The policy holder has the option to seamlessly switch between funds based on his/her choice. Also, your future premiums would be redirected to the newly chosen fund. Even if you are a passive investor in the equity market or just have knowledge about investing in the equity market, you can maximize the benefits of the Wealth Plus by switching between funds since it covers small cap, mid cap, and bond funds which have a different risk to returns ratio.

Just imagine that you are 40 years old and would remain invested for the next 20 years. Also, nothing wrong happens to the policy holder during the tenure. In such circumstances, as the age of the life insured increases and the remaining policy term reduces, ‘Life Stage & Duration Based’ strategy ensures that the sum invested is moved from riskier funds to safer funds over a due course of the time. As you are approaching 60 years, you can plan a graceful retirement since you have reaped benefits from the sum that you invested for the past 20 years 🙂

Under the Life Stage & Duration based investment strategy, the fund value is divided between the following:

Wealth Plus – Rising Star Benefit

If you are a parent, your child becomes your top priority. You ensure that your child is always happy and (s)he is given the best education so that (s)he can fulfil his/her dreams. Life is uncertain, and hence, it is left up to the parents to ensure that the child’s life is not adversely impacted when you are not around. Wealth Plus caters to these customers where the policy holder can avail the ‘Rising Star Benefit‘, where on the untimely death of the policy holder [the parent/grandparent], following benefits are paid:

Lump sum amount [based on age of policy holder] becomes payable immediately

Sum of all the future premiums are credited to the Fund Value

All future premiums waived off

Additional allocation will be added to the Fund Value as and when due

Maturity Benefit becomes payable on maturity

There would be a lingering question – What happens if nothing happens to the Policyholder? In such circumstances, on Maturity, you get the Fund Value. In case the Life Assured dies before the policyholder, the nominee would get either the Fund Value or Higher of the sum assured [whichever is higher].

Let us create a hypothetical scenario – You are around 30 years old and you pay an annualized premium of 1 Lakh. The sum assured is Rs. 10 Lakhs, investment strategy is Self-Managed and Payment mode is Annual. The premium paying term and Policy term is 20 years. With this input, on maturity you would make around Rs. 41.41 Lakhs. This number indicates that Wealth Plus is a ULIP that you can opt for both insurance as well as investment purpose.

Disclaimer: Information provided in the article is based on my research and I do not have any holding in it.

Technical development has modified how you execute trades on the stock markets. Several institutions offer online trading platforms with excellent features that make trading quick, easy, and simple.

One such platform is offered by brokerage firm, Kotak Securities and is known as KEAT Pro X. It is loaded with multiple chart types and allows quick trades. It is a terminal-based trading platform known for its speed and performance. Here are seven beneficial features of this share market software.

Fast and seamless experience

KEAT is among the highest speed trading platforms that are currently available. It enables you to avail of real-time updates and reports, which allows you to make accurate trading decisions based on the changing market conditions.

Customization as per user’s needs

A unique and very beneficial feature of this share market software is the customization feature. It allows you to develop your own personalized view of the stock exchange. Therefore, you are able to see the information as you want. Furthermore, you are able to create multiple watch lists with up to fifty shares in each of these. Another beneficial feature of this trading platform offered by a reliable share market broker is that the watch lists may be set into different tabs.

Small application size

Compared to other share brokers’ online trading platforms, KEAT is amongst the smallest in terms of its size. This ensures you do not require too much memory and bandwidth to trade using this platform. It is fast and agile, which are important features during the peak trading hours of the stock markets.

Live share prices updates

You are able to watch the market performance using real-time free share quotes from different stock exchanges. In addition to the prices, you are able to avail of information about market lot sizes, top active shares, top losers and gainers, option calculator, and index updates.

Portfolio tracking

This share broker’s online trading platform enables you to have complete control over your portfolio. You are able to track the performance of your entire portfolio comprising various holdings. This allows you to determine your profits and losses and make accurate decisions. Furthermore, this share market software allows you to view order confirmations and trades. You may trade long contracts and sell from your current stock holdings. The risk report section gives you information about limits and positions on different tabs to have better control of your portfolio.

Stock recommendations

The brokerage firm employs a team of experienced and trained research professionals and analysts. They constantly analyze and monitor the stock markets to provide detailed research reports. The research team also offers stock recommendations based on analyst calls. You may maximize your trading benefits through such recommendations.

Charting tools

This share market broker’s trading platform gives you the option of using several types of charting tools such as Candlestick and Area. It enables you to study and analyze the different trading patterns to make the right investment decisions. Charts are an important component of technical analysis, which is highly useful when you invest in the stock markets. Furthermore, you may create graphs and charts to track and analyze past and future performance of your favorite shares.

Benefits of KEAT

The following are some benefits you enjoy while using this brokerage firm’s software:

When you open an online trading account, this platform is available for free

You may select indices or sectors and business groups

It allows you to create personal watch lists based on predefined lists

The platform allows you to easily sell from your existing holdings

You are easily able to view the changing profit and loss position to make investment decisions

It is compatible with different operating systems, which includes Windows, Linux, and Mac

This trading platform runs on various devices like Android, Java, iOS, Symbian, and Bada

It uses high-end security encryption to safeguard your confidential information. The share market broker has encrypted the software with 128 bit SSL along with two-step authentication to ensure your information is never stolen or misused

The platform is completely integrated, which means all modifications are accurately reflected across different devices such as laptop, mobile handsets, and tablets

KEAT is a complete integrated platform, which means you may trade in different stock exchanges like National Stock Exchange [NSE] and Bombay Stock Exchange [BSE]. Furthermore, you may trade across different investment products such as equities, derivatives, and currencies. You may also create multiple watch lists comprising one or more of these various investment products.

Downloading this software is very simple and easy and may be done through the share broker’s website. Once the download is completed, you may follow the installation instructions and start using it to trade and earn profits in stock markets.

There are a lot of factors that affect your investment decisions and you should be very careful in analyzing the situation. You should consider all the aspects to make an informed decision.

Stock investing is a high-risk high-return financial instrument. The uncertainty related to price movements is risky. Furthermore, stock markets are affected according to economic and other factors. Therefore, you may be wary of investing in direct equities.

To mitigate some of these risks, you may consider investing in mutual funds. Such funds accumulate corpus from several retail investors like you and invest it in equity and equity-related products. The funds are professionally managed by experienced managers to deliver returns.

You may even invest in mutual funds through a Systematic Investment Plan [SIP]. A SIP is an investment plan under which you can invest a small amount at regular intervals in the funds of your choice.

The factors that affect stock markets affect mutual funds too, though not at the same magnitude. So, do not panic and discontinue or postpone investing in mutual funds through SIPs.

The market and NAV see-saw

Because of the volatility in the stock market, the Net Asset Value [NAV] of your mutual fund, mutual fund portfolio remains volatile. However, it is recommended you do not panic and discontinue your investments when the fund performance falls. Lower NAV for mutual funds is actually favourable, as it results in rupee cost averaging. You are able to accumulate more units at a lower NAV, which reduces your overall purchase costs.

Another reason why you must avoid discontinuing your mutual fund investment is to ensure your financial goals are not disrupted. Most SIPs are related to certain long-term goals and discontinuing these due to poor performance may have disastrous outcomes. In all likelihood, you will not immediately move your investment to another fund or financial product. Therefore, you postpone your ability to meet your financial objective.

Thus, you should ignore discontinuing your SIP or mutual fund investments even if markets appear turbulent or slow. These conditions are only temporary, and your investments are long-term. In fact, if you are not already investing, it would be the right time to invest in mutual funds.

Non-performing funds vs. slow market conditions

It is crucial that you carry out a thorough research and then conclude if it is your fund that is under-performing or it the overall market that has slowed down. This is extremely critical because, if the overall market has slowed down, then this would be the ideal opportunity to accumulate more units and invest in under-performing funds.

However, if the research findings definitively point out that the mutual fund you have invested in is underperforming or not performing then it would be a wise decision to switch funds. Nonetheless, it is very important that you immediately start investing in another better performing fund.

Short-term market conditions vs. long-term Investments

Time in the market has always been more reliable and fruitful than timing the market. This approach has always been served well, even to those investing directly in the stock market.

There are many brokers and investors that make money by timing the market, but the risks involved are very high as the market is unpredictable. The risk in timing the market is that you buy an equity, anticipating that it will appreciate in the short-term and then you can sell it and make money. Alternatively, you sell it, anticipating that its prices will fall. However, this may not happen and you may lose your capital investment too.

These risks do not apply to mutual fund investments, as these are for the long-term. The short-term volatility of prices and market affects only marginally on the earnings of such investments, as the earnings herein are dependent on the overall performance of the equity over the long run, and has little to do with short-term fluctuations.

Right time to stop your SIP investments

It is important you refrain from discontinuing SIP investments until you want to stop investing completely. If you want to stop investing in one fund, you must immediately invest in another.

Do not make your investment decision based solely on the fund performance. Compare it to the overall benchmark, similar funds, and the fund category to make an informed decision.

You must not make your choice based on the short-term [two or three months] performance of the fund. If the performance is below average, it will take at least six to nine months before it shows up. Temporary under-performance must not be the basis for your investment decision.

In case your research shows that your chosen mutual fund investment is accurate, consider increasing your investment at dips. Investing in mutual funds requires a little bit of financial planning first, such as what are your investment needs, how much corpus you need to accumulate, after how much time you need the money, and how much risk you are willing to undertake. You can use a personalized mutual fund recommendation platform such as Angel Wealth, which will suggest you mutual funds to fulfill your needs.

GST is a single indirect tax on the supply of goods and services in the entire chain right from the manufacturer to the supplier. Good and Services Tax [GST], since its effect has left multiple emotions in the mind of the common man, there are a number of questions which need answers in order to understand GST.

Image Source – GST

Let us understand the difference between GST and other taxes which were in effect before its applicability.

VAT [Value Added Tax] was considered to be the first generation reforms introduced in April 2005. The existing sales tax was replaced with VAT. Central Sales Tax, Excise Duty, Customs Duty, Service Tax became part of VAT.

Goods and Services Tax is considered to be the second generation of tax reforms. The VAT system was merged with Luxury tax, entertainment tax and renamed as State Goods and Services Tax [SGST]. Furthermore, Central Sales Tax, Excise Duty, Customer Duty, Service Tax have been incorporated under a single umbrella as Central Goods and Services Tax [CGST]. There is no major segregation between the VAT and GST, the taxes have been clubbed together and brought under a single umbrella.

What are GST rates and when is it levied ?

As per the Act, all goods and services have been placed in five brackets – 0%, 5%,12%,18%, and 28%. The tax is levied on the sale of goods and services. Each bracket has multiple items falling under it, which are a taxed accordingly.

The tax applied is ‘Value Driven’ i.e. it is applied on goods or services at every stage where the value of the goods or services increases or is added. The tax will be levied where the goods or services are consumed. For example, if the goods are created or manufactured in Maharashtra and sold in Andhra Pradesh, then the tax would be levied in Andhra Pradesh.

What are the types of GST ?

GST is destination based. Basis the same, these are the following types of GST:

SGST – State Goods and Services Tax

CGST- Central Goods and Services Tax

IGST- Interstate Goods and Services Tax

The sale of goods and services intra-state would levy central and state GST. The inter-state sale of goods and services would levy inter-state GST.

Is GST same for all ?

GST is different for different businesses. The application of GST for different businesses is also different.

Mostly, all businesses, whether manufacturing or e-commerce have been brought under the purview of tax regime. Registration forms an important part of GST. It is important for businesses to register and procure tax number in order to file tax as per the stipulated norms.

Is GST registration mandatory ?

There is a stipulated threshold for businesses to register which is an aggregate turnover of INR 20 lakh in a financial year. If the businesses are under that threshold, it is not mandatory for these businesses to register. In such cases, the registration is voluntary.

As per the Act, if the registered seller sells the goods and services to the unregistered buyer, he is supposed to pay GST for the unregistered buyer. If your business is registered under VAT or service tax or excise duty, you should migrate to GST.

The GST explainedabove is the basic know how about the new tax. It is also important to understand the tax regime appropriately and file the tax when due. The assessee can login into the Government of India website, which provides necessary information in regards to the changed tax regime.

A zero balance account can be any type of bank account which does not require a minimum balance to maintain it. Conventional bank accounts require the account holders to maintain a minimum balance at all time. If the account holder makes withdrawals from the minimum balance, the bank will charge a penalty. However, with a zero balance account, you can even withdraw the entire amount in your savings account without attracting any penalty.

Zero balance accounts can be used for both personal and professional purposes. Businesses generally use a zero balance 811 account to make payments. Since a balance is not maintained in these accounts, the interest earned from these accounts will be less. Hence businesses maintain just enough money to cover their pending debts in a zero balance account.

A zero balance accounts are a great way to keep your money liquid and separate from the other interest earning assets. They have great utility for controlling your money flow. Hence the chances of money loss from bounced checks, theft and mistakes are quite less. Moreover, banks allow expedite transfers between zero balance and other accounts, hence it is a quick and reliable way to obtain funds. Financial emergencies may strike out of the blue, however, with zero balance accounts, you can be assured of quick availability of fund without any restrictions

Benefits of a Zero Balance Account

One of the major benefits of a zero balance account is the feature of no minimum balance.

Earn interests on the amount deposited as per prevailing bank rates

Free ATM cum Debit card

Get new cheque book each year with no extra charges

Free access to online banking and fund transfer services

Special privileges and offers for salary account holders

The RBI has mandated all the banks to allow a zero balance account to be used as a secondary bank account. Therefore, even if you have a saving account with a particular bank, you can use this as a secondary account to manage your regular savings. Moreover, the rate of interest offered by zero balance accounts is the same as savings accounts. Hence you need not worry on that note.

How to Get a Zero Balance Account?

Most of the banks offer zero balance accounts for personal as well as business use. A personal zero balance account can be opened with minimum documentation. You just need to submit your identity proof and address proof along with the KYC form to the respective bank. Business customers can speak to their bank about zero balance account options.

What are the characteristics of a sound investment? Usually, a good investment gives profits, has the potential to tackle inflation, can explore the true power of compounding interest and diversifies your invested money. An equity mutual fund is one such investment that can display all these traits. What if, along with being a sound investment, equity mutual funds could also help you save taxes? Now, that would be an icing on the cake! However, you don’t have to look around hard. Equity-Linked Savings Scheme [ELSS], a type of equity fund, can provide the icing.

So, let’s run the rule over ELSS and see how it fares against other tax-saving products.

Tax Benefits

An ELSS is a diversified equity mutual fund with a majority of its investments in equities. Thus, like an equity mutual fund, there is no Long-Term Capital Gains [LTCG] tax for an ELSS.

ELSS funds have a lock-in period of three years. The amount you receive after three years is tax-free. ELSS helps you claim tax deductions of up to Rs 1.5 lakh under Section 80C of the Income Tax Act, 1961. Notably, this proviso is not applicable to other types of equity funds.

Why ELSS trumps other investments?

National Savings Certificate [NSC] and public provident fund [PPF] can be considered ELSS’ direct rivals when it comes to tax-saving options. Let’s see how ELSS fares against these two tax-saving funds.

Lock-in period

o ELSS: 3 years

o PPF: 15 years (option of partial withdrawal after 6 years)

o NSC: 5 years Returns

o ELSS: 16.48%*

o PPF: 8%

o NSC: 8% Safety

o ELSS: Related to equity performance

o PPF: Considered safe; different asset class

o NSC: Considered safe; different asset class Deposit method

o ELSS: Systematic investment plan

o PPF: Available [deposits can be made in 12 instalments]

o NSC: One-time deposit Tax on returns

o ELSS: Returns and dividends are tax-free, but only after the first year

o PPF: Returns are tax free.

o NSC: Not available

* Category average as on September 29, 2017 as per the CRISIL–AMFI ELSS performance index.

The lowdown on the three tax-saving funds show that ELSS can provide the highest returns. It also scores favourably on its liquidity quotient when compared to the other two options.

Additionally, by investing in ELSS through the Systematic Investment Plan [SIP] route, you get a chance to explore the power of rupee cost averaging.

ELSS: Your doorway to equity

In a country of over 132 crore people, a little above 5.5 crore people invest in mutual funds. According to another report, most states have less than 5% registered stock market investors. Thus, it is safe to assume that Indians don’t like to invest in equities. But, ELSS could help change your views. With ELSS, you can save taxes and simultaneously enter the world of equity.

Unit Linked Insurance Plan [ULIP] may shout out saying they provide the option of investment and insurance and is therefore better than ELSS. But ELSS is more liquid, tackles inflation better and can also provide higher returns. To top it, ELSS is managed by a professional fund manager; you don’t need to constantly worry about revisiting your portfolio.

To sum up

There are numerous options available for you to save taxes. However, very few options can help you save taxes and give high returns. ELSS can be that option. So why wait?

Purchasing a new car is indeed a dream for many. There are numerous aspects to take into consideration while buying a car. These include comparing various brands and models, selecting the right mode of finance, choosing the best dealer, and taking the car for a test drive, among many others. Once you have made the purchase, it is necessary to ensure that all legal formalities have been completed.

Follow the below-mentioned steps after you have bought your dream vehicle.

Check if all the paperwork is in order

Upon purchase of your car, make sure that you have the necessary paperwork from your dealer. Some of the documents include registration certificate, receipt of payment, tax receipt, and delivery challan, among others. You may also make sure to receive all the original documents in case you have borrowed a loan from a bank.

Insurance

According to the Motor Vehicles Act, 1988, it is mandatory to have a car insurance policy. Such an insurance policy

Accessories for your vehicle

If you have just bought a new car, you may make small value additions to enhance the look and safety features of your car. If your car does not come fitted with reverse cameras, mobile docks, or Bluetooth kits, install them upon purchase. You may also invest in a gear lock, mud flap, steering wheel cover, remote central lock with security alarm system, and GPS navigator, among others. Such accessories turn to be very useful, at times.

Proper maintenance of your car

Vehicle maintenance is very important for numerous reasons. It helps to reduce repair costs, maintain the car’s value, and also optimizes your car’s performance. Take your car to your local service center for regular servicing. You may make regular checks on your car’s engine, tire pressure, transmission, battery, emission system, and brake system, among others.

Roadside assistance

In an event of a breakdown such as a flat tire or engine failure, you may be left in a desperate situation. In order to avoid such a situation, purchase a roadside assistance cover that comes as an add-on on most auto insurance policies. You may seek emergency towing services, replacement of a flat tire, replacement if your keys are lost, and may also avail of coverage against minor repairs.

Take the aforementioned tips into consideration upon purchase of your new vehicle. Ensure to have all car-related documents such as registration certificate, 4-wheeler insurance, and Pollution Under Control [PUC] certificate. Once you have all your documentation in place, drive the car of your dreams without any hassle.