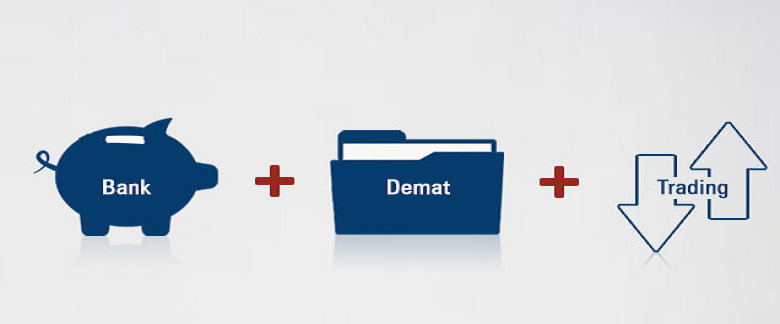

In order to save or borrow money with a bank, it is necessary to have a savings account. Similarly, to invest in the stock market, you may open a dematerialization account.

Understanding dematerialization [Demat] account

A dematerialization account, also known as a demat account, holds shares in an electronic format. It holds certificates of financial instruments that you have invested in, such as mutual funds, government securities, shares, and Exchange Traded Funds [ETFs], among others.

Benefits of having a dematerialization [Demat] account

You may open a demat account and enjoy the numerous benefits it has to offer. Following are five major advantages of holding shares in the dematerialized form.

- Through such an account, you may hold all your investments in a single account. It, therefore, acts as a common bank for your investments.

- Another major benefit is the automatic update facility. Since it is a common account, it eliminates the need to give out your personal details every time you make a transaction. Your personal information will automatically be made available to the companies you are transacting with.

- Holding shares in a physical format makes it susceptible to risks such as theft, loss of share certificates, or fake shares. Dematerialization, however, eliminates such risks. Upon approval of your trade, the securities get credited to your online demat account. Your securities are, therefore, safe and free from risks.

- Traditionally, it was necessary to pay stamp duty while transferring securities. This cost is eliminated while transacting through your dematerialization account.

You may, therefore, avail of the above-mentioned benefits of a dematerialization account.

Procedure of opening a dematerialization account

Quite contrary to the popular belief that the process of demat account opening is a cumbersome task, the same is not true.

You may follow the below-mentioned steps and open an account easily and quickly.

- The first step is to choose a Depository Participant (DP) of your choice.

- You may then submit a duly-filled application form in the prescribed format. Along with the application, it is mandated to provide supporting documents such as proof of identity, proof of address, and PAN card copy, among others.

- The next step is to sign an agreement on a stamp paper provided by your Depository Participant.

- Upon successful opening of a demat account online, you will be allocated a unique beneficial owner identification number. This number is to be used as a reference in all your future transactions.

- Once your dematerialization account is opened with the Central Depository Services (India) Ltd [CDSL], you may then trade securities using your unique demat account

A dematerialization account offers numerous benefits to traders who buy and sell securities on a regular basis. You may open such an account or even multiple accounts with the same DP or with different DPs. By doing so, you may execute transactions easily, and have full control over the transaction being executed.