Most people start planning their retirement life well in advance. The need for stable income during the retirement days is a must, especially when dealing with medical expenses during those years of your life. So, how do you ensure that you have sufficient income during retirement even with the lack of a consistent paycheck?

This is when your insurance plans come in handy. As a matter of fact, it necessary to start planning your retirement early in life. That timeframe allows you to build a robust financial source which you can rely on in the future.

In this article, we will discuss whether you should invest in ULIPsor Pension Plans.

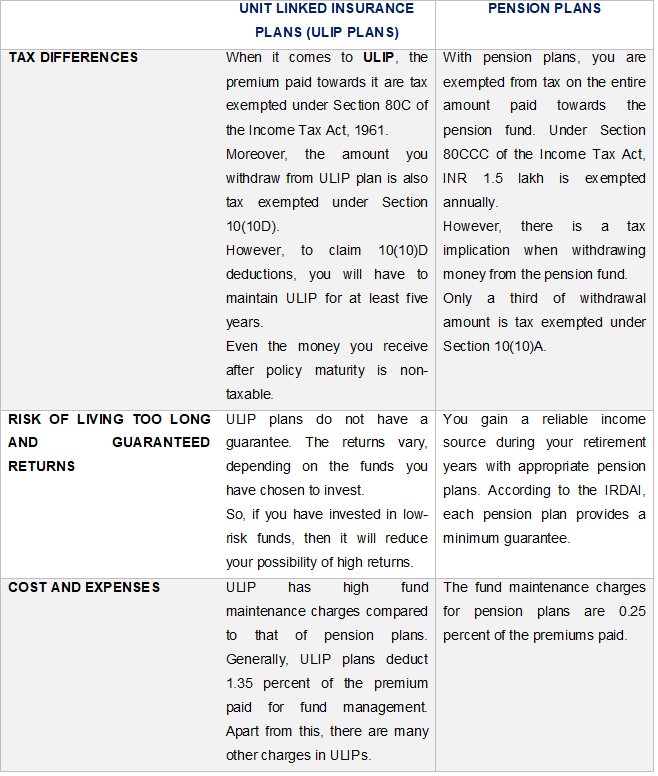

ULIP vs Pension Plans

In the table below, we have compared the two based on a few factors:

Despite the additional charges in ULIP plans, it is still one of the most reliable insurance instrument available in the market. Moreover, with ULIPs, you have the flexibility to invest in funds of your choice [depending on your risk appetite].

Generally, you can invest in equity-oriented funds, debt funds, or a combination of the two. If your risk appetite is low, then consider investing in debt funds. However, for those with a high-risk appetite can invest in equity funds.

Closing Thoughts

Between ULIP plans and Pension plans, if you have started your retirement investment early, then you might as well consider investing in ULIPs. The ULIP returns over the long run are high and beneficial. But make sure that you are comparing different ULIP plans online before choosing one. Also, keep monitoring the stock market movement to make necessary changes to the fund investments.

With age comes knowledge and experience to make better decisions. However, your ability to earn would reduce, as you grow older. Hence, it is important to start saving for retirement at a young age. Saving and investing a good amount of money when you are young will give you immense benefits once you reach your retirement age.

When you plan to save for your retirement, it is not enough just to have an ordinary bank account. You need a good long-term savings plan specially curated for retirement. Banks provide senior citizen savings account with additional benefits and offers so that you can enjoy while you retire.

Currently, there are many savings and investment options through which you can save for your retirement.

Here is a list of a few below

EPF [Employee’s Provident Fund]

Start saving in EPF if you are a salaried person which will be beneficial in the long run. But you must not withdraw from EPF savings if you want to get long term benefits. If you take loans from EPF or close it down prematurely, then you might not be able to reap the benefits fully.

Senior citizen saving scheme

This Government-sponsored scheme is popular among senior citizens and is available only for senior citizens and those who plan to retire early. SCSS is a long term saving/ investment that acts as a steady flow of income for senior citizens. It can be availed from banks and post offices. The scheme has a tenure of 5 years but can be extended for 3 more years.

Post Office Monthly Income Scheme

It is a five-year investment scheme with a cap of Rs.9 lakh for joint ownership account, beneficial for senior citizen couples. The interest rate on the account, which is 7.7%* p.a is paid every month, and the interest amount is credited into the same bank account.

There is also the option to reinvest in the scheme post maturity for another 5 years to get double benefits:

Fixed deposits

Fixed deposits are another famous choice among senior citizens for saving money. It is easy to operate; it is safe and gives a fixed return without any risks. Fixed deposit is available for a maximum tenure of 10 years, thus enabling FD holders to start retirement planning in advance. In addition, senior citizens get extra 0.50% of interest on FDs that means more savings in the longer term.

Mutual funds

Early investment in mutual funds can give big benefits in the longer term due to higher profits. For that, you have to start investing in it before your retirement. Mutual funds are guided by market fluctuations and can are subjected to risks. But if properly planned, it will give you greater returns compared to other investment avenues like fixed deposits.

Tax-free bonds

Tax-free bonds are offered by government-backed institutions, which are extremely safe to invest for senior citizens and non-senior citizens with guaranteed returns. These tax-free bonds are available for 10, 15 or 20 years. Hence you must invest in tax-free bonds before retirement so that by the time you retire the bonds will also mature, and you will get the benefits.

Proper planning at young age can let you retire with a huge sum of money. Start planning today, one-step at a time.

A demat account is a mandatory requirement for those who want to trade in securities. This account is like your bank account, as it holds the securities for you. You need to have a bank account, a trading account, and a demat account to trade in the stock market. It is possible to have multiple demat accounts in India.

Image Source

Many traders want to have the best of both worlds and therefore, they prefer multiple demat accounts. Some traders have trading accounts with a full-service stockbroker, as well as, a discount broker. This allows you to make the most of the services offered by both the types of brokers.

However, you also need to consider brokerage, customer service, and a range of trading products before making a decision. A single broker might not be the best at all services and hence, multiple demat accounts can make a huge difference.

Additionally, you can also have multiple demat accounts to segregate between trading and investment practices. This will keep you aligned with your goals and you will be able to plan your investments in a better manner. It is important to remember that you cannot have two demat accounts with the same stockbroker. When you open demat account online, understand the terms and conditions of the broker. It does not make sense to have multiple accounts with the same broker.

The process of demat account opening is quick and convenient. However, in multiple accounts, you need to remember that there will be annual maintenance charges in each account. This could increase the cost of trading. Moreover, if the account remains inactive for a very long time, it will freeze after a few alerts sent to you and you will have to go through the e-KYC process again to reactivate it. You will also need more time to track and manage all the accounts separately.

There are pros and cons of having multiple demat accounts but serious traders enjoy having different accounts for different investment goals. You do not need to close a demat account when you open a new one and you can link any number of trading accounts with your bank account.

Most importantly, you do not need multiple trading accounts for online demat account opening. You can legally manage one bank account and multiple trading accounts and one trading account and multiple demat accounts.

Consider your personal preference and requirements before opening multiple demat accounts in India.

While borrowing money has become necessary for many small businesses. Some smart business owners are always on the lookout for ways to reduce their interest rates for business loans. After all, depending on how much loan is borrowed, the type of loan, and the health of the business, loan payment can quickly spiral out of control, affecting every aspect of your company.

Image Source

So how to reduce interest rates for business loans? Here are a few tips:

Look at your company the way the bank does

You need to understand what the lenders are looking for and also consider steps that would lead a lender to assign a higher interest rate. Once you’re able to recognize those issues, fixing any of them could lead to low business loan interest rates because you’re actively making your business a lot safer.

Improve your personal credit score

Your personal credit score is a helpful indicator of your history and likelihood of repaying a debt. So, reducing interest rate before you’ve acquired the loan, is an important strategy for showing the lender you’re a qualified borrower. Moreover, improving your personal credit score can also help you if you ever decide to secure another loan.

Do your homework

There are business loans that are tough to qualify for, loans that take a long time, loans that you pay back daily, and every type in between. But how to get low business loan interest rates? Well, one way to make sure you’re paying the lowest possible interest rate is to complete the research necessary to know that you’ve borrowed from the best possible lender to avail of the best interest rate for your situation.

Pay faster

There are two ways lenders calculate interest:

Simple Interest

In simple interest, a lender will require repayment in a certain amount of time at an amount somewhere above the original amount owed.

Compound Interest

In compound interest, the loan amount is calculated at certain set intervals, and the interest rate is calculated based on the remaining balance of the original loan amount in addition to previously accrued interest.

Many business loans have a particular date at which the interest rate increases in case of a remaining balance. That hike in interest rate can cost a lot, so make sure you’re paying the loan as soon as possible.

Refinance your business’s debts

If you acquire multiple loans at high-interest rates at the beginning of your business and your finances have improved, refinancing could be a perfect option. You could integrate the outstanding debt into a single loan with a reduced interest rate based on the improvement of your company’s financial health.

Make a strong impression

When you meet with lenders, make sure you’re completely prepared. Treat these meetings like job interviews and give more time and effort into a thorough business plan. Making sure you’ve got the proper and necessary documents and records on hand. With a smart business plan and be ready to explain the future of your company.

Prove to the lenders that you are reliable enough to repay the loan. Once you’ve proven you’re not at risk of failing to pay, you are much more likely to get lower interest rates for business loan.

Bike insurance or two-wheeler insurance is an insurance policy which can include both third-party insurance along with own-damage insurance. While third-party damage indemnifies you from any legal claims resulting out of an accident involving your bike, own damage insurance provides cover to your bike because of any accident or damage. The Motor Vehicle Act in India makes it a statutory requirement for all motor vehicle insurance policies to have a third-party cover.

Image Source

You must always remember to have a valid insurance for bike as not having insurance is a traffic offence. As per the Motor Vehicle [Amendment] Bill, 2019, not having valid insurance for bike is punishable by a fine of Rs 2,000 and/or imprisonment up to three months for the first offence and an enhanced fine of Rs 4,000 for the second offence.

In 2018, the Insurance Regulatory and Development Authority of India [IRDAI] announced changes in insurance rules for bikes. For new bikes purchased after September 1, 2018, the IRDAI made it mandatory to avail five-year insurance for third-party. This meant that the premium for third-party, for a total of five years, had to be paid upfront while purchasing a new bike. Owners of two-wheelers purchased before the specified date could continue with their existing insurance policies.

Here, you must remember that the IRDAI made changes about third-party rules. Own-damage premium could be availed both on a multi-year or annual basis. The change in rules did affect rules about the no-claim bonus or the Insured Declared Value [IDV] of a bike.

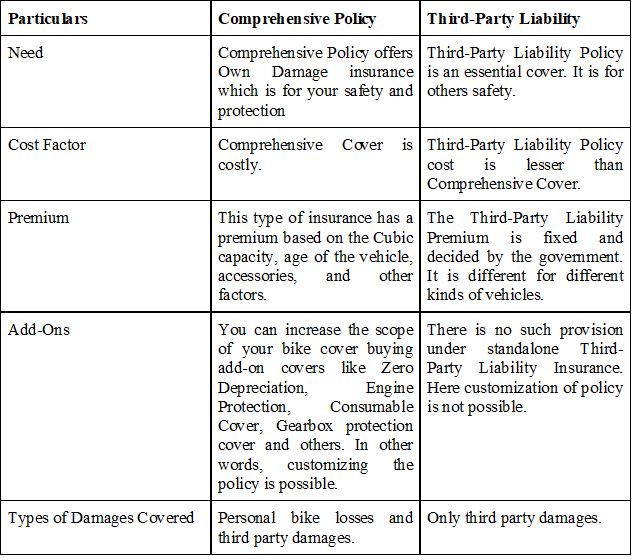

Types of bike insurance plans

You can avail of two types of bike insurance plans

Third-party liability cover – This policy provides financial cover only to the third-party against damages by your bike.

Comprehensive cover – This policy covers any damages suffered by your bike and you along with the mandatory third-party cover. Other benefits include a cover for damages arising out of man-made and natural calamities and against vehicle theft.

Existing options for bike owners with regards to insurance policies: If you are a bike owner, you have the option of multi-year comprehensive two wheeler insurance policy, where the premiums for both third-party and own damage have to paid for multiple years, or a bundled policy, where you are required to pay own damage premium on an annual basis. You can opt for an annual policy or a multi-year policy on the basis of your specific requirements. But a multi-year insurance for bike is always advantageous vis-a-vis annual policies.

Benefits of multi-year insurance policies: Along with reduced costs on the bike insurance price through discounts by insurers, there are many benefits of multi-year bike insurance policies. Some of these include:

Hassle-free – You don’t have to worry about how to renew bike insurance online. At Finserv MARKETS, policy renewal is an easy and straight forward process. Forget the worry of getting your bike renewed each year amidst a host of personal priorities like filing of income tax returns, vehicle servicing, annual health check-up etc. If you forget to renew the bike insurance on the specified date, then you run the risk of riding with an invalid insurance. This is a punishable offence.

Saves from increase in premium – IRDAI and insurers revise the bike insurance policies on a regular basis, usually annually. Purchasing a multi-year policy protects you for the increase in bike insurance price due to revisions. So you can save money on the bike insurance price through reduced premium payments.

No Claim Bonus benefits – Insurance companies provide you with No Claim Bonus[NCB] for not making any claims for own damage during a year. In the case of annual policies, the NCB will fall to zero in case of no claims, and won’t be carried forward. But, in the case of multi-year policies, the NCB will be carried forward to the next year. The bonus can start from 20% at the end of the first year to a maximum of 50% for five consecutive years.

Easy cancellation – Even if you want to change your existing insurer after completion of the first year, you can easily buy bike insurance from another company and apply for cancelling the present multi-year insurance policy. You can receive a refund after your application is processed. What’s more, the NCB can be transferred as well through an NCB retention certificate.

Which multi-year bike insurance policy is the best?

You can consider Bajaj Allianz Two Wheeler Insurance policy, available on Finserv MARKETS, which provides you with attractive discounts on the bike insurance price. You can avail of hassle-free renewals with no requirement of bike inspection. Along with cashless settlement of claims at more than 4,000 network garages, you can avail of 24*7 roadside assistance. You can apply for getting a new insurance policy, or for renewal through a simple online process. You can also register your claims online, resulting in quicker settlement of claims.

Becoming a resident of India’s capital has its own perks. Yes, it makes a lot of sense to have a home in Delhi. With the city growing by leaps and bounds, Delhi has become famous for its residential localities. Home loans are a preferred way of purchasing a Delhi address.

Image Source

If you need more convincing, here are the top ten benefits of getting a house in this megapolis.

Connectivity

If you have a home in Delhi, you have access to connectivity in every form. Indira Gandhi International Airport is the main gateway for the city’s domestic and international air travel. The city’s road network is well-maintained. It also has one of India’s largest bus transport systems. Then, there is Delhi Metro, which allows mass rapid transit and is the lifeline of the city’s urban travel. Explore housing loan options provided by Tata Capital if you are thinking of buying a house in Delhi.

Renowned medical facilities

Delhi being the capital city of India provides all major types of facilities. It is famous for the All India Institute of Medical Sciences [AIIMS], Delhi is a premier medical school for treatment and research. There are also different top-quality private medical hospitals and nursing homes in and around Delhi, which provide modern healthcare.

Good property investment

Delhi and the larger NCR provides ample opportunities for real estate investment through homes. For instance, Gurgaon is one of the fastest-growing cities of India. With migrant workforce demand driving the home demand, Delhi allows you to buy a house and hold it over the years to enjoy capital value appreciation.

Attractive rentals

If you are looking for rental income, a home in Delhi is a good option. Rental can help pay your Home Loan EMI and be a second source of income. When you repay the home loan, you can get full advantage of the rental income. So, consider Tata Capital housing loan schemes if you are looking to buy a house here.

Multi-cultural hotspot

Delhi’s culture has been influenced by various factors. It is home to people from Punjab, Haryana, Uttar Pradesh, Bengal, Tamil Nadu, Kerala, and increasingly from North-Eastern states. The multi-cultural story makes Delhi a treat for those with a deep interest in literature, fashion, food and performing arts. It has a vibrant culture that embraces people from different parts of India and the world.

Key economy

Delhi is the largest commercial centre in northern India. With a growing economy, the workforce is looking for good homes at useful locations. Job demand, salary/income growth, and various products & services make Delhi’s economy diversified. Taking a home here gives you the chance to enjoy the fruits of this important economy. Consider a housing loan to do so.

Close to hill stations, tourist hotspots

Delhi ranks as one of the top 30 most visited cities in the world. It has numerous tourist attractions, both historic and modern. Shopping hubs are in Connaught Place, Chandni Chowk, Sarojini Nagar, Khan Market, and Dilli Haat. Religious sites include Laxminarayan Temple, Gurudwara Bangla Sahib, Lotus Temple, Jama Masjid and ISKCON. It is also located close to many hill stations in nearby states.

Access to top-quality education

For families wanting to stay in Delhi, education is an important criterion. A home loan can be worthwhile for parents if their children have access to top-quality education. Delhi has famous private schools. It has over 150 colleges, five medical colleges and eight engineering colleges.

Government amenities

The Delhi government has announced that people living in the capital do not have to pay any amount of their electricity bills if their power consumption does not exceed 200 units. Additionally, there is a one-time waiver of water arrears, which means all categories of houses will receive an exemption from late fee payments. Consider Tata Capital housing loan schemes if you are looking to buy a house here.

Sports capital

Delhi is a booming sporting hub. It has hosted many major international sporting events such as Asian Games, Hockey World Cup, Commonwealth Games, and Cricket World Cup. Cricket and football are the most popular sports. Buddh International Circuit in Greater Noida also hosted the Formula 1 Indian Grand Prix. This is good news for residents who are sports enthusiasts.

Most people prefer using credits due to the reward programmes linked to them. These rewards are like bonus given by the banks in the form of incentives, air miles or cash banks. Generally, banks offer reward points based on the types of credit cards.

Credit card users can redeem these points for several benefits like discounts on shopping, gift vouchers, etc.

How can one earn rewards on credit card?

You can simply earn rewards on a credit card while making transactions using them. While you can certainly earn reward points for day-to-day purchases, you can enhance your rewards further by using credit cards smartly. For this, you need to understand your reward programme and ways to earn reward points.

Many banks gift certain rewards points to their new credit card customers as a Welcome Bonus. So, you can earn reward points just by getting a new credit card. Sometimes, card issuers also give more reward points to the customers, who spend a certain amount during the initial period.

What type of transactions will get you more reward point?

All credits are linked to rewards points for specific amount of transactions made on them. For example, if a credit card offers five reward points spend on every Rs. 200, then the card user will get 1250 reward points after spending Rs. 50,000. The same rewarding system is applied for almost merchant establishments like shopping websites, utility bills, etc.

Buying expensive things like jewel or electronic items or booking a holidays will help you earn more reward points on your purchases. You can also earn more reward points by linking your credit cards to utility bill payments. As utility payments are compulsory expenses, you get the following double benefit by using credit cards to pay them,

Earning rewards points for each transaction

Becoming eligible for loyalty points

Furthermore, premium credit cards like Gold or Platinum are linked to higher reward points than standard cards. Banks provide additional benefits to the customers who have been with them for a longer time and who use their credit cards for bigger transactions. These credit cards provide their users with even more reward points on selected brand partners.

There is one specific category of credit cards called fuel credit cards. The users of these cards are getting more reward points whenever they swipe these cards to fill fuel at the outlets partnered with their banks. Just like fuel credit cards, there are travel credit cards linked to accelerated reward points for transactions made during travelling.

How can you redeem reward points?

You need to know how many rewards points you have earned by logging to your credit card account or by contacting your bank.

There are reward catalogues where you can find the information on the merchandise you want to buy and rewards points required for them. These catalogues contain a variety of options from different categories like travel, lifestyle, home décor, etc. You have to select the product and redeem your reward points to purchase it. Then, the product gets shipped to your mailing address. The process to redeem any product from the catalogue is similar.

Doubling there number in just ten years, the number of two-wheelers sold in India crossed a figure of 20 million units. A whopping number of a category of vehicles which includes scooters, mopeds, and bikes.

Image Source

As rose the number of two wheelers in use, there increased the number of accidents. The prime reasons established for collision include speeding bikes and no use of helmets. More than the loss of the two wheelers, the value of life lost in an accident is considered more precious.

Also, the new amendment in the Motor vehicle act made applicable from 1st Sept-2019, which increased the traffic penalty by a huge amount.

All above reasons made people buying Two-wheeler Insurance to protect from financial burdens, third party liabilities and avoid heavy traffic fines. Also, the digital insurance companies like Digit Insurance has made the overall process of buying Two Wheeler Insurance Online very easy and simple.

Before buying the two-wheeler policy, understanding the type of insurance is very important as it becomes complex for common people sometimes. Let’s discuss what are these.

What is Comprehensive Two Wheeler Insurance?

A Comprehensive Two Wheeler Insurance policy is the widest possible cover available for a vehicle. This type of insurance policy is said to offer two types of covers; one is Own Damage and the second one is Third-Party Liability. You can seek compensation in any of the following cases:

For the own damage, that is, any kind of repairs needed in the two wheeler after a collision.

For own damage that may arise due to natural calamities like floods, fire, or falling objects.

For total loss of the vehicle which may happen due to theft of the two wheeler.

For Third-Party Liability that arises if you happen to damage someone else’s property or body.

What is Third-Party Liability Insurance?

As per the Motor Vehicle Act,2019, the Third Party Two Wheeler Insurance policy has been made mandatory by the Government. Anyone using their two wheeler on the road should have the TP Liability policy. Failing to do so, the driver will have to pay a penalty and face imprisonment. TP Liability insurance will take care of your legal liability to pay for the losses caused because of you. To put it in simple words, the third-party liability policy will pay for you when you are held legally liable for bodily injury or property damage.

If you are still not sure of which cover is sufficient for your two wheeler, then you must know the difference between the two types of insurance policies. Here is how you can distinguish the two.

Difference between the Comprehensive and Third Part Two Wheeler Insurance Policy

Which is better?

Comprehensive two wheeler Insurance Cover offers dual protection to you that includes Own Damage and Third-Party Liability. Getting two covers is always beneficial as it will save your money in case of damages. Imagine you were taking a U-turn on your bike when the traffic from your opposite left side was flowing. You were in a hurry because of which you hit another biker. It was your mistake as you should have waited for the traffic to stop from the opposite end.

Both you and the other biker fell. Your bikes were damaged. It was your driving mistake and you were held responsible for the loss. But you had taken a Comprehensive Cover so your insurance company paid for both own damages as well as third-party liability losses. Hence, we can say buying Comprehensive is better than Third-Party Liability alone.

Only if your bike is very old then there is no point buying a Comprehensive Cover for it because then you can afford the cost of repairs.

Comprehensive Insurance Policy will pay for your personal damage which is not possible with the Third-Party Liability Policy.