Paytm QR now lets merchants accept Paytm, UPI and Card Payments directly into their Bank Account at 0%. Also, there is no monthly limit on accepting payments from customers. This will in turn make it easier for small and large merchants to accept mobile payments from a wider set of customers, and boost their businesses. It will also give more choice and convenience to consumers as they can now scan Paytm QR at merchant stores and pay using their preferred payment methods.

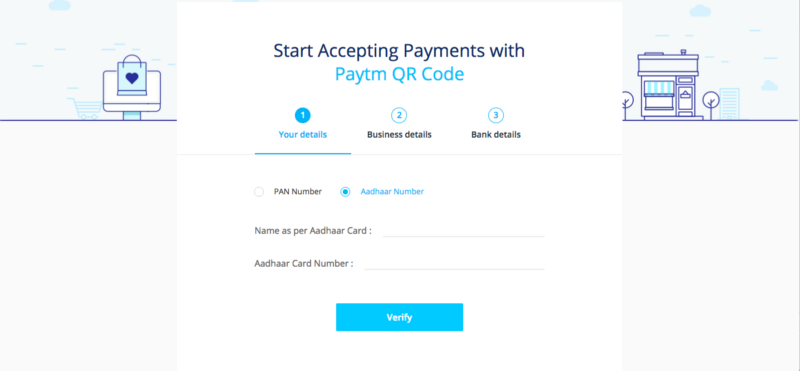

Here’s how to generate Paytm QR instantly

Give a missed call on +919004790047 or follow these steps:

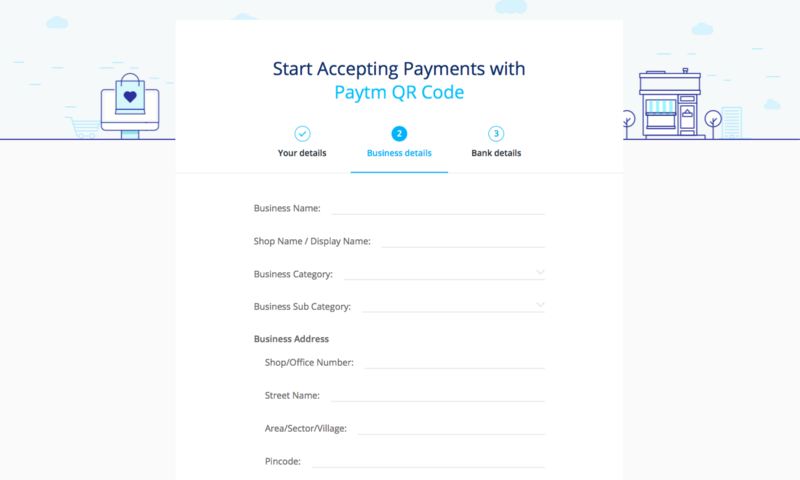

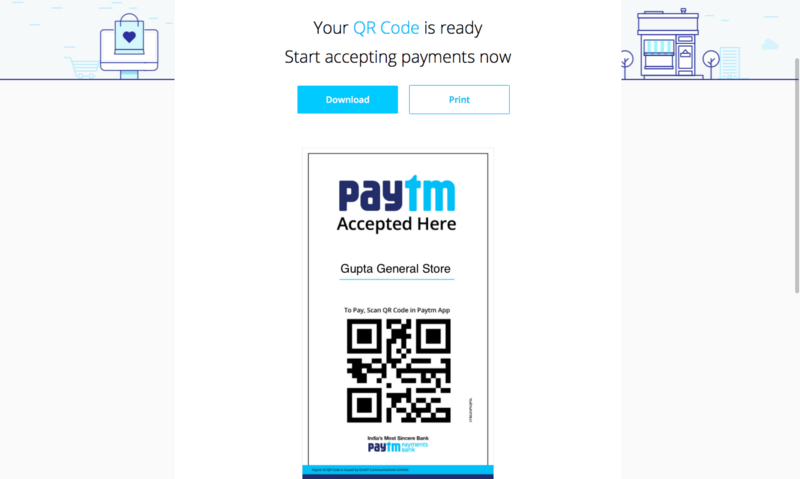

Fill in Business & Bank details, and Paytm QR is instantly generated

Merchants can print the QR and put it up in their shops, and start accepting Paytm

Paytm QR has eliminated the need for additional spends on POS machines for merchants and has been supporting them in their day-to-day business. Currently, Paytm offers customers the widest range of offline and in-store payment use-cases including parking, tolls, kirana stores, utility, temples, local transport, railway & metros, school & college fee and challan among others.

Transacting has come a long way from bartering an item for another to buying everything on credit. Credit used to be a luxury that was provided by vendors, only to customers that had a long history of buying from them.

However, with the evolution of the banks, the availability of credit has expanded, from being provided to select customers by the vendors to customers being backed by banks for all their purchases from all vendors.

This facility provided by the banks is offered through credit cards. A bank provides this facility to almost all its customers with different spending limits, depending on their accounts’ balances and longevity of the relationship with the bank.

Evolution of the credit card

The first token to allow someone to buy stuff on credit was issued in 1947, known as Charg-It, and was accepted at multiple stores in specific areas of Brooklyn. It was a status symbol to have owned this card.

The idea gained momentum particularly with the traveling salespersons going for the Diners Club cards in 1949. It allowed them to travel without having to carry cash for food, fuel, and hotel stays. They were able to use this card only at network outlets though.

Looking at the phenomenal response that Diners Club cards got, banks as well started issuing such charge cards. In 1950 American Express charge cards were launched. Learning from their experiences and expanding aggressively, the charge cards are changing the way we transact, the world over.

The global expansion

In order to push the use of charge cards, the Bank of America mailed a plastic charge card to all its customers in Fresno, CA with a credit limit of USD 500 each. A lot of these were stolen and/or misused, thus creating huge losses for the bank. The experiment came to be known as the ‘Fresno Drop’ and was not a complete failure though. It was a learning that highlighted the security issue and propelled the evolution of the cards with higher security.

The present-day chip and credit card pin is the most secure and accepted mode of payment.

The Indian market

Up until the last decade, carrying out cashless transactions was a luxury, enjoyed only by a select few who were educated enough to understand how it worked and owned cards. The use of plastic money has been consistently on the rise during the last decade; however, it got a boost post the demonetization rolled out by the ruling government in 2016.

The cards are increasingly used for most online transactions. Additionally, people swipe their cards to pay for fuel, groceries, and other daily items. Several institutions offer special rewards points program for increased usage. The Indian population has come a long way from the barter system to the plastic money especially with the government promoting digitalization in the country.

The card culture has penetrated urban India but still has a room for expansion. Rural India is a vast untapped market that is still reluctant to switch to plastic money. Don’t have a card? Apply for one today and enjoy the freedom from paying in cash.

India Energy Storage Alliance [IESA], India’s leading alliance on energy storage, announced start up pitch competition and innovation pavilion for Energy Storage India [ESI] 2018 during Jan 10th to 12th in New Delhi. This is India’s first start-up competition focused on energy storage, electric vehicles & charging infrastructure and micro-grids.

The competition is supported by Startup India, Mumbai Angels, TiE-Delhi-NCR, Sangam Ventures & Global Energy Storage Alliance [GESA]. ESI is the leading international conference and expo addressing the need for energy storage, micro-grids & EV solutions in India. It provides first-class networking event to drive energy storage market expansion in profitable applications – highlighting the synergies, inter relationships & new business opportunities for transmission, distribution, customer-sited, micro-grids/campuses and e-mobility applications.

ESI 2018 will also feature Innovation pavilion to showcase next- gen products and solutions from startup companies. To enter the competition, start-up companies having annual revenue < Rs 3.25 crore [$ 0.5 million] and operations of < 5 years can submit the start-up details in 500 words by 30th December 2017. Shortlisted companies have to submit 5 slide presentation by 8th January 2018 and the top 3 winners will get complimentary IESA membership for a year.

Process of the competition

Application form submission by 30th December 2017

Shortlisted companies will be informed by 2nd January 2018

Up to 10 shortlisted companies will present their concept at the Investors Forum on 11th January

2018 at ESI2018

Top 3 companies will receive IESA awards with cash prize and expression of interest from

investors

Dr. Rahul Walawalkar, Executive Director, Indian Energy Storage Alliance [IESA], said

We are excited to announce first of its kind startup competition for the Indian startups in energy storage space. Today, India has more startups than before and is on the cusp of transformation. Certain challenges are faced by them due to limited direction and access. With this competition, we want to bridge the gap using IESA network and I invite the Indian entrepreneurs to take advantage of this opportunity.

We are thankful to Startup India and other partners for their support to us. India is anticipated to become one of the best markets for the adoption of energy storage technologies due to several drivers like the fastest growing economy, increasing the share of renewables, transmission constraints, need for providing 24*7 quality power and electric mobility mission. IESA has set a mission to also make India a global hub for innovation and manufacturing of advanced energy storage, micro-grids sand EV technologies by 2022.

The Government of India has clearly decided to prioritize electric vehicles with a goal of having 100% Electric Vehicles by 2030. Energy Storage is a key component of this and there are number of ways in which EV adoption could be transformative for the grid. With better tariff structures and use of right storage technologies in EVs, one could also use EVs as distributed storage and provide grid balancing services. This transformation will not only help in greening the transportation fleet by reducing diesel/petrol consumption and associated emissions but will also help in greening the grid if EVs are used for better integration of renewable resources in the grid. Many Indian automobiles companies have plans to adopt EVs.

The 5th International Conference & Expo on Energy Storage and Microgrids is scheduled from January 11 ~ 12, 2018 along with Pre – Conference Workshops on January 10, 2018 2018 at India Habitat Centre, New Delhi, India. Shri Suresh Prabhu, Honourable Minister for Industry and Commerce will be inaugurating the conference & exhibition. Mr. RV Deshpande, Minister of Large and Medium Scale Industries and Infrastructure Development, Govt. of Karnataka [First state to release electric vehicle and energy storage policy in India] will be the keynote speaker for electric vehicle session. This year, it is poised to get 2000+ industry experts, 100+ speakers from over 25 countries and 50+ exhibitors.

IESA was launched in 2012 to assess the market potential of Energy Storage Technologies in India, through an active dialogue and subsequent analysis among the various stakeholders to make the Indian industry and power sector aware of the tremendous need for Energy Storage in the very near future. It aims to make India a global hub for research and manufacturing of advanced energy storage technologies by 2022. For more information, please visit IESA

India currently has around 3 million developers and has the second largest Android developer community in the world after the US. As per a study from Deloitte, India will have the largest base of developers by 2019. Developers will be drivers of customers’ adoption of cloud and cognitive solutions. About 60% of the developers in India have been experimenting with AI [Artificial Intelligence] and machine learning, compared to 39% in the rest of the world. This shows developers in India are receptive towards AI, Cognitive and data science technologies.

AI, Machine Learning, Cognitive computing, Data analytics, etc. are some of the emerging technology trends and they are now observing widespread adoption. Today, IBM stands at the forefront of a worldwide industry to lead the next phase of change revolutionizing the way in which businesses work and grow. With rapid changes in the technology landscape and open source movement, top-down approach is no longer being followed in organizations and developers are now playing role in the entire technology eco-system. Cloud related technologies are a boon for the developers and the barrier to entry has become limited.

IBM, as a part of the ‘Developer Relations Group‘ works with clients, students, developers, startups amd support them in understanding technology, helping them and get their job done effectively. Seema Kumar leads the IBM Developer Relations group which is a part of the IBM Digital Business group. We had a chat with Seems Kumar about IBM’s eco-system efforts, its involvement with startups, role of Watson in shaping up AI industry, etc. So, let’s get started with the Q&A…

Every organization is involved with top tier institutes, what are some of the steps that IBM Evangelism team is taking in order to connect with the student community in lesser known institutes ?

Every student is important to us, irrespective of whether the student is from IIT/IIM or from colleges that are located in tier-2/tier-3 cities. This is mainly because lot of innovation is happening from universities that do not carry the IIT/IIM tag. Students from these colleges are continually learning and the credit goes to the low barrier to entry. IBM has a developer platform called OnTheHubwhereany university can enroll, students get IBM Credits and they can also use IBM tools for software development.

In some colleges, we also have some development courses as a part of the curriculum where we train faculty members on Watson, Chatbots, AI, etc. and most of the association is with tier-2 institutes.

What are some of the initiatives that IBM is taking to connect with the startup and the entreprenurial community in India [be it TiE, NASSCOM, etc.] ?

Startup eco-system in India is very vibrant. IBM works directly with startups as well as with other partners. IBM has partnered with TiE, NASSCOM 10000, etc. where in some cases, IBM participates in community events.

In case of NASSCOM 10K, IBM works with startups where we monitor and mentor them. Our programme is called as Global Entrepreneur Programme [GEG], there are different plans namely Standard, Basic and Premium Plan. IBM has been actively involved in mentoring startups across different sectors like EdTech, HealthCare, etc. from technology, business expansion, market readiness, etc. point of view.

More than 200 startups are working with IBM in the technology space. In fact, lot of startups are using Watson API’s for building meaningful apps around Chatbots. For example, a startup that we are mentoring built a chatbot named ValleyBotto identify fake news and they are getting good amount of traction.

There are lot of cloud solutions available in the market, what are some of the major advantages for moving to the IBM cloud [both from the developer as well as enterprise perspective] ?

IBM has various solutions for different audiences. IBM’s cloud offering is a combination of Public, Private and Hybrid cloud. As a matter of fact, lot of apps available in the existing data centers are not cloud ready i.e. Even if they are migrated to the cloud, they cannot capitalize on the benefits of virtualization, effective resource utilization, etc. Cloud solutions from IBM helps you build cloud native applications. Developers are always on the look-out for their own choice of technologies.

IBM Cloud is a Platform As a Service [PAAS] offering that has various API’s for different programming languages. Choice, flexibility to use what developers want and the way they want are some of the key differentiators. Most of the apps of the future would have some sort of cognitive capabilities built into it and Natural Language Processing [NLP], visual recognition features to build conversation interfaces would be some of the basic building blocks to build a cognitive application. These features are available in the Watson APIs and using these APIs, apps are enterprise ready from day one of development!

To summarize, choice of catalogue, breadth of services, flexibility to choose between Public/Private/Hybrid cloud and ability to build secure, cognitive, enterprise ready software on the cloud are some of the inherent advantages.

Can you comment on Chatbots and what are some of the core ingredients of a Chatbot kind of application ?

Context of conversation and Intent are very important ingredients in building a Chatbot and hence, training & design of the oervall interface are very important factors when building a Chatbot. Watson APIs are very powerful and are specifically designed by keeping these important factors in mind. With every interaction, learning happens and it gets better with more data.

There is buzz about Blockchain, what according to you are some of the ideal use-cases where Blockchain might be useful for a ‘Digitally Growing’ like India ?

Blockchain as a technology is constantly evolving and it is definitely here to stay. Blockchain offers powerful Usecases for any usecase that involves multiple parties and multiple transactions. In a nutshell, it is nothing but a distributed ledger. Initial usecases have obvisouly evolved in the Finance sector but Blockchain would be relevant in other sectors as well.

Blockchain when used in conjunction with IoT, lot of powerful usecases would eveolve. For example, IBM recently worked with the Mahindra Group to build a Blockchain solution for supply chain finance across India. This solution improved the transparency of overall operations. IBM also announced a Trade Finance platform using the IBM Blockchain platform that can be used by banks. Blockchain can also be extended across other sectors like Healthcare, Insurance, etc.

Your comments on Digital India and how IBM’s involvement in the overall journey ?

There is definitely a robust infrastructure in place with Aadhar API’s, eKYC, India Stack, UPI, etc. have led to a huge thrust in digital payments in India. As far as IBM is concerned, we work closely with iSpirtwhere we also participate as an eco-system partner.

India is a country with rich amount of data and this is where the aspect of Data Science becomes very critical as we need to draw valuable insights from the data. IBM has also tied-up with NASSCOM and Government Of Karnataka to build Center Of Excellence [COE] in Data Science where IBM will be the core technology partner. IBM will not only groom talent in data science but will also work on Proof Of Concept [POC] and support startups in that category.

What are some of the certifications that a student/professional can opt for, in order to gain expertise/know-how in Cognitive Computing, Machine Learning, Cloud Computing, IBM BlueMix, etc. ?

IBM has partnered with an EdTech partner where we launched Cognitive Class previously called as Big Data University. IBM has also tied-up with JigSaw Academywhere they use IBM’s Big data expertise for all their courses. In the area of certification, IBM has partnered with Global Knowledgethat offers on Cloud computing, DevOps, AI, etc.

There has been lot of scepticism that AI, Robotics & other ‘Automation/Machine related technologies’ would wipe off many jobs in future, what are your thoughts on the same and how can AI [and other technologies] go hand-in-hand with human jobs ?

Ginni Rometty, IBM CEO believes in three principles that are applicable in the cognitive era – Purpose, Transparency and Skills. The purpose of a cognitive app is to augment human intelligence and not to replace humans. Products and Services from IBM are built with this principle in mind and human intelligence is a key aspect.

IBM is helping human beings being more productive, realize their potential and focus on more important jobs rather than working on mundane & repetitive jobs. You must be clear as you build AI platforms how they are trained, and what data was used in training. When we talk about transparency, IBM has always been cognizant of data. AI platforms must be built with people in the industry and companies must prepare to train human workers on how to use these tools to their advantage.

We thank Seema Kumar for sharing her insights with our readers and walking us through the awesome work done by IBM for shaping up the developer ecosystem. If you have any questions for Seema about Watson, Chatbots, how solutions from IBM can accelerate your development, etc. please share them via a comment to this article.

There is a very famous saying when it comes to investing – ‘Never put all your eggs in the same basket,‘ which in simple terms means that you need to have a diversified investment portfolio. Higher the risk, higher are the chances of yielding better returns, but as an investor, you need to formulate the entire plan based on various factors like age, assets, liabilities, existing investments, risk appetite, etc.

We are always on the lookout for investments that would give the maximum ROI [either in the short-term or long-term], but in some cases, you need to park aside the factor of ‘short-term gains’ and opt for an investment plan that can safeguard your near & dear ones when you are not around. There are pure play ‘Term Insurance Plans’ that provide insurance for a certain period of years, and the payout is done only if the policy holder is no more. However, what if there existed a plan that is an amalgamation of the two worlds – Term Insurance and Wealth Creation?

When we talk about investments, we cannot rule out the role that ‘technology’ is playing in every aspect of the spectrum – financial planning, tax saving, insurance, etc. Renowned financial institutions are now leveraging the power of AI, machine learning, deep learning, etc. in order to serve the digitally savvy investors who now seek to manage their money in a digital world. Rising internet and smartphone penetration, push for Digital India, rise of Fintech are some of the factors that contribute to the growth of the overall financial sector. Financial companies are becoming more agile to meet the changing needs of digitally savvy young investors by rolling out products to that particular market segment!

We had earlier hinted about a product that is an ideal fit from investment as well as insurance point of view. Edelweiss Tokio Life has come up with an #Unyakeenable Unit Linked Insurance Plan [ULIP] called the Wealth Plus Plan.Whether it is about securing your child’s future or saving for long term, Wealth Plus has the answers. So, let’s delve deeper into features of Wealth Plus, its benefits, etc.

Wealth Plus – High Level Features

Wealth Plus from Edelweiss Tokio Life is a market-linked insurance plan aimed at digitally-savvy customers. It is an industry-first product that is aimed at wealth creation and has no premium allocation & policy administration charges. The only assurance that the company needs from its customers is:

Paying the premium on time, and

Staying invested.

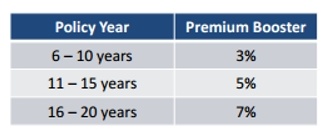

As a percentage of Annualized Premium, there is additional premium allocated on every premium paid and that increases over a period of five years. Additional 1% allocation is added with every premium installment in the first 5 policy years.

Another useful feature of the Wealth Plus is the ‘Premium Booster’. Premium Booster is added at the end of each year starting from the 6th Policy year till the end of the Premium paying term.

The reason why the company advises it’s investors to stay invested for a long term is that over a 20-year premium paying term, 80% of the one-year premium is reinvested via additional allocation. This means that a major portion of your premium is being paid via the interest earned on the earlier premiums paid by you.

Wealth Plus – Investment Strategies Suited to Your Requirements

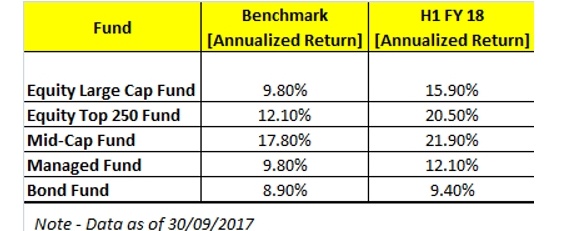

Investing in any fund becomes less beneficial if there are stringent terms associated with the fund. However, in case of Wealth Plus, the investment terms are very flexible, and the policy holder is free to invest the premium in any of the available funds based on his/her risk appetite. This is termed as the ‘Self-Managed‘ option. The funds available are below:

Equity Large Cap Fund

Equity Top 250 Fund

Equity Mid Cap Fund

Managed Fund

Bond Fund

The policy holder has the option to seamlessly switch between funds based on his/her choice. Also, your future premiums would be redirected to the newly chosen fund. Even if you are a passive investor in the equity market or just have knowledge about investing in the equity market, you can maximize the benefits of the Wealth Plus by switching between funds since it covers small cap, mid cap, and bond funds which have a different risk to returns ratio.

Just imagine that you are 40 years old and would remain invested for the next 20 years. Also, nothing wrong happens to the policy holder during the tenure. In such circumstances, as the age of the life insured increases and the remaining policy term reduces, ‘Life Stage & Duration Based’ strategy ensures that the sum invested is moved from riskier funds to safer funds over a due course of the time. As you are approaching 60 years, you can plan a graceful retirement since you have reaped benefits from the sum that you invested for the past 20 years 🙂

Under the Life Stage & Duration based investment strategy, the fund value is divided between the following:

Wealth Plus – Rising Star Benefit

If you are a parent, your child becomes your top priority. You ensure that your child is always happy and (s)he is given the best education so that (s)he can fulfil his/her dreams. Life is uncertain, and hence, it is left up to the parents to ensure that the child’s life is not adversely impacted when you are not around. Wealth Plus caters to these customers where the policy holder can avail the ‘Rising Star Benefit‘, where on the untimely death of the policy holder [the parent/grandparent], following benefits are paid:

Lump sum amount [based on age of policy holder] becomes payable immediately

Sum of all the future premiums are credited to the Fund Value

All future premiums waived off

Additional allocation will be added to the Fund Value as and when due

Maturity Benefit becomes payable on maturity

There would be a lingering question – What happens if nothing happens to the Policyholder? In such circumstances, on Maturity, you get the Fund Value. In case the Life Assured dies before the policyholder, the nominee would get either the Fund Value or Higher of the sum assured [whichever is higher].

Let us create a hypothetical scenario – You are around 30 years old and you pay an annualized premium of 1 Lakh. The sum assured is Rs. 10 Lakhs, investment strategy is Self-Managed and Payment mode is Annual. The premium paying term and Policy term is 20 years. With this input, on maturity you would make around Rs. 41.41 Lakhs. This number indicates that Wealth Plus is a ULIP that you can opt for both insurance as well as investment purpose.

Disclaimer: Information provided in the article is based on my research and I do not have any holding in it.

SharkID, the Smart Phonebook app, achieved 1 lakh downloads; with their network database zooming past 1,75 cr. A bootstrapped StartUp with capital investment of $ 2 million, SharkID is a joint venture between e-Procurement Technologies and Silver Touch Technologies, founded by Ramesh Sinha, a technocrat and serial entrepreneur.

SharkID is a smart phonebook app backed by a highly scalable Service-oriented architecture with full stack technology, SharkID deploys a Big data Database Mongo and Redis for storage and Encrypted streaming for data security.

Speaking on the occasion, Ramesh Sinha, Founder – SharkID, said

Crossing a lakh downloads is a defining moment for SharkID. It reaffirms our core belief; that, given a best-of-breed, secure and smarter technology, User migration is inevitable. Every smartphone User will migrate to a smarter, easier and meshed experience, if someone provides it. And that is precisely what we do.

When 50,000 network connections get added every day and they zoom to 1.75 cr, it validates our belief many times over and is testimony to our technical array expertise and user experience. SharkID stands committed to provide bleeding-edge technology support and a secure, user immersive experience.

Elaborating further, he added

SharkID is geared to provide an immersive experience – based on your usage and communication pattern, our data analytics pack will smart-search for you and refer people with whom you can network. Added to this, you can also check your connects to the persons suggested, tightening the reference cycle and generating productive conversations.

Currently the company plans to deepen the user experience and expand the userpool across India to 10 million by March 2019

About Shark Identity Private Ltd

Shark Identity Private Ltd is a JV between Silvertouch Technologies and eProcurement technologies. A bootstrapped startup founded by Ramesh Sinha and Jignesh Patel, SharkID aims to replace physical visiting cards with digital cards over the next few years. For more information, please visit SharkID

There is a very interesting thread on Quora about the ‘Percentage of Salaried Class’ in India and though the thread has very interesting answers, one thing that is common across any salaried person [be it employee in the organized or unorganized sector] is that each one of them wants to maximize their take-home salary. Salaried professionals who are paying tax are always on the look-out to save extra so that can pay less taxes. If you consider the Blue-collar workers, many workers might not fit in the ‘Tax Slab’ and some of them might still not even have a salaried account.

There was a definitive requirement for a product – ‘Digital Banking system‘, that could cater to both the White-collar and the Blue-collar segment. There has been very little innovation made in the banking requirements for the SME and MSME segment. This is where two entrepreneurs Vinay Bagri and Virender Bisht sensed an opportunity and they co-founded NiYO, a fintech company based out of Bengaluru. NiYO helps you maximize your take home salary by enabling you to track, manage and claim various tax benefits like food, gift, medical, fuel, travel, phone etc. NiYO consists of three important components, namely NiYO app that makes mobile banking easy, NiYO corporate portal that is accessible by its corporate clients and NiYO all-in-one card that has role-based entity.

The core-objective of NiYO is ‘Put salary where it truly belongs – in the employee’s hands.’ We had a discussion with Vinay Bagri, Co-founder and CEO, NiYO Solutions about the NiYO app, the overall market being addressed, how NiYO can help employees increase their take home salary, their fintech platform, future road-map, etc. So, let’s get started with the Q&A…

Can you walk us through the NiYO platform that can be used by white-collar employees ?

NiYO is a digital platform for salaried employees. When we talk about salaried employees, they are broadly classified into two categories – White collar employees and Blue collar employees.

NiYO started with a product for white collar employees that is primarily into taxation. There are total 22 items where tax can be saved by the employees. Employees can avail tax benefits across 10~11 items like LIC Premium, Savings under 80C/80G, HRA, etc. Employees have control over other 10~11 items namely LTA, medical allowance, gift vouchers, meal vouchers, etc. Employee and Employer have to work in tandem in order to avail these tax benefits.

How does NiYO helps in maximizing an employee’s take-home salary ?

What NiYO does is that it optimizes these taxation items for employee as well as employer. For employer perspective, NiYO makes these items paperless, easy to maintain and ensure that they are audit and tax compliant.

From employee perspective, employees can avail more benefits since the employer is now able to pass more benefits to the employee. In that process, emoployees are now able to significantly increase their take-home salary. NiYO also offers a virtual bank account.

What are some of the core components of the NiYO platform and what are some of the USP’s of the product ?

The core product of NiYO consists of three main components:

NiYO offers a virtual as well as physical card. Unlike other cards that are offered by other companies, the card offered by NiYO is a combination of debit, credit and prepaid card and it plays an appropriate role based on the outlet/location where the card is being used. For example, when a NiYO user tries to withdraw money, it acts as a ‘Debit Card‘. When user swipes the card at a food outlet, it automatically pulls money from the ‘Food Wallet‘. When an employee/user uses the card for a transaction when (s)he is on an official trip and swipes the card for a reimburseable item, it takes the shape of a ‘Credit Card‘.

In a nutshell, the card that is offered from NiYO is a combination of Debit card, Prepaid card and Credit card.

What are some of the main pain points that are solved by NiYO ?

NiYO solves two major pain points:

Users now have the convinience, where they need not carry more number of cards since the card offering from NiYO is an all-in-one card.

Since our system is intelligent enough to identify the ‘type’ of transaction, it helps employees in saving more from their salary.

Founders of NiYO [L to R] – Virender Bisht and Vinay Bagri [Source]

Please walk us through the NiYO mobile app and walk us through some of the interesting features of the app ?

The mobile app from NiYO has all the major mobile banking features. Employees can attach bills/other expense reports used for official purpose as a proof of expense to the mobile app. In order to ensure that there are no submission of fake bills by the employees, employer gets an intimation when the card is swiped for a transaction. This step acts as a ‘Proof of Payment‘. To take the security to the next level, employee has to also attach the copy of the bill at the location where the card is used. This mechanism is termed as a ‘Proof of Expenditure‘.

This lethal combination of Proof of Payment and Proof of Expenditure is an ideal way for our customers/organizations to make the reimbursement process tax & audit compliant and at the same time ensure that there is ‘zero fraud’ done during the time of submission of bills.

How do your ‘corporate’ clients ensure the authenticity of the transactions and facilities available at their front ?

HR department from NiYO’s client organizations would have access to the corporate portal where they can view the details of the transactions incurred by an employee ‘X’. The employer would have access to the details of the transactions where employees have applied for a reimbursement.

What are some of the advantages of the NiYO card over offerings by players like Sodexho ?

There are number of benefits of the card offered by NiYO when compared to offerings from Sodexho, some of them are listed below:

Sodexho is a single wallet card that can only be used for food items. On the other hand, the card from NiYO can do much more as already discussed earlier and these facilities are availble on a single platform.

With NiYO, you can use the card at any food outlet where they accept payment via VISA/Master/RuPay cards. Sodexho can only be used at around 40K food outlets where they have tie-ups. NiYO has more reach which is close to around one million outlets.

NiYO also has a very interesting feature – split wallet. For example, if 3K is spent at a food outlet but NiYO’s customer [Employee] has only 2K in the food wallet, split wallet feature comes into action. In such a scenario, NiYO would automatically deduct 2K from the the Food card and remaining 1K would be deducted from the Credit card. In this process, a single transaction is automatically optimized for taxation benefits. NiYO acts as a technology provider and for the card, NiYO has tied-up with couple of banks.

Can you talk about the market size for a service like NiYO ?

There are close to 27 ~ 30 million salaried people in India who pay some kind of taxes. NiYO can be used as a salaried account/travel expense product/a fintech product where an employee can do ‘Financial Planning‘. Hence, NiYO would become a full fledged banking product for the employee.

Please share some insights into the Gift card aspects of the NiYO card ?

As far as corporate gifting is concerned, gifts worth INR 4900 are tax-free, beyond which the expense becomes taxable. There is a ‘segregation’ feature on the gift card wallet in order to ensure that an employee gets maximum tax benefits. Hence, there is no requirement for a seperate gift card and NiYO’s client [organization] can seamlessly load money in the gift wallet.

Morever, all the features on the card are customizable and they can be controlled via the ‘Employer portal’. Employers are free to keep it as an ‘open system‘ or a ‘closed system‘. To summarize, NiYO is currently the only player that has all these features with no competition as of now.

What are some of the features around financial planning on the NiYO platform

For tax and financial planning, NiYO has tied-up with H&R Block, which is one of the largest tax planning companies in India. From the NiYO app, an employee can do tax planning, plan savings, etc. There is an option for ‘Self tax planning & assisted filing‘, where someone from the H&R Block would call NiYO corporate customer and provide necessary support.

How has been the overall response to the NiYO App ?

Feedback has been very good, but there is an increasing demand for features like add-on card, etc. The core USP of the NiYO app is the best in-class ‘field process’. For example, you can attach a proof of insurance towards 80D on the NiYO app itself and the review would be either performed by the employee’s finance team or finance experts from the NiYO team. With such facilities at their persual, employees need not visit any other portal for financial planning.

As of today, NiYO has more than one Lakh customers/corporate employees using the NiYO platform. Out of one Lakh customers, around 60K customers use NiYO as a ‘salary account’. NiYO is also used by blue-collar workers that have salary of less than 15,000. None of the financial institutions want to open salary accounts for blue-collar segment and even if the bank does so, they charge fees and there is a minimum balance requirement.

With a nominal fee, NiYO can open a digital salary account. Everything is eKYC compliant and there is no paperwork involved. Messages sent to NiYO’s blue-collar customers are in vernacular language i.e. Hindi since NiYO for blue-collar workers is only rolled-out in North India. Card is charged for everyone, which is close to around 200 INR per year.

Can you share the product roadmap of NiYO?

In the future, NiYO will provide our customers with all the advice related to taxation and financial planning. Unlike other financial platforms, NiYO would consider taxation as a major factor for financial planning. For example, investing in a good Mutual Fund would yield 12~14% returns on a CAGR basis whereas investmets made via the NiYO platform would result in much more returns on the same investment.

Also, our customers can use the NiYO app to do a QR Code transaction since it would be leveraging the Bharat QR code mechanism. Our customers can opt for doing a payment via Unified Payment Interface [UPI]. The end goal of NiYO is to encourage employees go shift to ‘Spend and Forget mode’ since NiYO would be responsible for complete tax planning and savings.

We thank Vinay Bagri for sharing his insights with our readers. If you are an SME and on the look-out for some good payroll solution, do give NiYO a spin. If have any questions for him or the NiYO Team, please email them here or share them via a comment to this article.

With business processes becoming more human centric in their ways to deal transactions, it has become crucial for entities to invest in corporate travel – a key operational business activity for Indian enterprises as they visit clients, suppliers and investors and pursue the ongoing aim of building their business both domestically and internationally. However, a recent study done by the CFO Innovations Asia reveals that as large as 74% organisations have more than 21 people that travel on business purpose on a regular basis leading to a need for greater visibility and control over the travel and expenses process.

Indian enterprises are at a tipping point of technology adoption in terms of managing their Travel and Expenses [T&E] expenditure. Organisations deploying automatic T&E processes, have an in-house platform and are not linked to any cloud-based architecture. The present system for Travel and Expense function cites difficulties in obtaining more granular information on individual employee patterns of usage and compliance, and a lack of flexibility in obtaining best pricing for hotels, car rental and airline costs.

Compliance and showcasing information ready for the audit process happens to be other relevant challenges that this industry needs to overcome at the earliest. With successful cloud adoption, systems and processes for the travel business in organisation will see a streamline of operations, resulting in a greater compliance, visibility and control to deliver better data management to senior managers, and also into improving the audit process. This is where Concur, a SaaS company providing travel and expense management services to businesses is creating a dent in the T&E space. We spoke with Neeraj Dotel,Managing Director, India and SAARC Concur around the current challenges that is faced by the Travel and Expense industry in the market and how cloud adoption can act as a transforming wave in the T&E sector. So let’s get started with the Q&A…

Note : ‘I’ in the interview refers to Neeraj Dotel.

Can you give a brief introduction about yourself and some insights into Concur India

Am currently working as the Managing Director for Concur Technologies for its India and SAARC operations. Prior to Concur, I have worked with Compuware as their MD for a period of 3 years and earlier before that, I was associated with Microsoft in different roles for almost 11 years.

With more than 21 years’ experience in sales and marketing overall, my expertise also lies in financial services and technological transformations in the banking sector. In my current role, I have been helping Concur diversify its business in India.

Concur, n SAP company, is a global leader in travel and expense management and is in its fifth year of operations in India. Our founder is of Indian origin and along with Mike Eberhard our President, we are very passionate about our focus in the country. We are continuously increasing our presence in India with stronger investments and in roads.

We have setup the Bengaluru delivery centre with over a thousand employees working there. India is an evolving market for the travel and expense segment and one of the top 20 markets for business travel globally. The estimated expenditure last year on business travel alone was $33 bn and expected to grow at double digit rates [Source]. Eyeing this opportunity, we have been planning several investments around business travel through booking websites, with the recent one being an equity investment in Cleartrip.

Concur has helped companies to recover Input Tax Credit taking companies of all sizes and stages beyond automation to a completely connected spend management solution encompassing travel, expense, invoice, compliance and risk. In India, post GST implementation, Indian companies have become very sensitive towards their employees and clients. Customer experience and bottom of the pyramid is the most crucial element here. Indian enterprises are looking out for methods to reduce investments and operational costs, at the same time provide a superlative employee experience. We tend to leverage this, and provide them with tools that cater to the aspirational needs of their employees and ensure business growth in the process.

Even in large MNC’s in India, the Business Travel & Expense Management is not yet automated [i.e. still there is lot of paper work involved], how can Concur help such organizations so that they can take the Digital leap in the T&E process ?

Digital transformation is not just a process but a philosophy of business. It is a drive to make a complete paperless economy. It impacts a CFO’s job in terms of expense visibility, employee productivity and policy compliance. About 98% of business travellers in India feel that it is painful to not only deal with the stress of travel but also with the stress of claiming expenses.

We at Concur believe that digital transformation of an organization should be such that it is easy and intuitive to use and the people using it should be able to reap its benefits. We provide these CFOs with advanced solutions that automatically synchronise their financial data of the entire spend process. The automation of these processes enhances the experience of business travel, reduces time, and increases transparency and visibility. Our intention is to become the most preferred application for business travel and expense management. We abide by the philosophy that you cannot save what you cannot see, and try to deliver on the same lines.

Can you touch upon the current scenario of Travel & Expense industry, especially from an Indian perspective ?

The travel and expense industry is evolving in response to the growth of mobile technology. Travel professionals are realising that they need to modernize their tools and programs for improved efficiency. A study by GBTA foundation, explores that direct booking behaviour in employees is becoming increasingly popular, with nearly 40% of business travellers regularly contacting the suppliers directly. Employees are sometimes not satisfied with company-preferred tools and therefore they are adopting a self-service approach.

Companies realising this are now looking towards integrating mobile technology and corporate travel processes, realising the importance of implementation of streamlined solutions to cater to the needs and requirements of their employees, to ensure the safety and security of employees, especially those traveling on behalf of the company and minimise cost. When it comes to corporate travel, Duty of Care is an important business challenge. The Business Travel Show 2017 forecastreveals Duty of Care as one of the top concerns for organizations in managing business travel, along with curbing spends and enforcing compliance [Source]. Duty of Care is defined by organisational culture and the local context under which an organisation operates. In all of Asia, as also in India, relationships with co-workers are highly valued.

Another trend is that many business travellers are using ride sharing services – Uber, Ola and shared accommodation like Airbnb, while on a business trip. The sharing economy is a big push towards being business relevant. Through our robust travel and expense management solution, Concur is providing clients with greater control and application of travel policies, and enabling seamless processes through an integration of Concur’s online booking tool and travel request authorisation.

Concur now offers access to low cost carriers like IndiGo, SpiceJet and GoAir along with hotel options like Accor and Airbnb, all of which is absent in traditional channels. With disruption present in every sphere of business today, the relevance of a sharing economy is also growing considerably.

What are some of the major advantages of taking the T&E to the cloud [using solutions from Concur] and how would it benefit [in terms of savings] to the organization adopting your solution ?

The most basic advantage for companies to take travel and expense to the cloud is to reduce the cost of operations. The traditional methods of capex investments, building your own solutions, and customising is not just complicated, but also consumes a lot of time and money. Concur’s idea is to make travel and expense management easier. Our innovative solutions improve customer experience for the modern business traveller. We integrate the T&E process to give managers visibility, compliance and control over expenses. It enables you to compare spend data, analyse cash flow and eliminate any errors. It’s not just about automation, we also care about the customer’s needs as well, understanding the relevancy of the approach to be taken.

One of the major issues that companies face while dealing with Travel Expenses is ‘Submission of Fake Bills’ from employees, how does moving to the cloud curb such malpractices by employees ?

A research conducted by Concur observed that 20% of expense reports submitted have some problem or other which might be a compliance default or a fraud or fake bill that caused it. In India the risk is higher because we are also operating with hand written bills, which are admissible most of the time. An employee can easily use this to get wrong bills into the system. So, the magnitude of the problem is huge and we believe that if a solution like ours is not adopted to manage those bills and eliminate errors for on the T&E process. Inflating bills or submitting forged bills which happen in every company, whether it’s unintentional or intentional which eventually exposes the company to litigation and fraud of things.

Concur captures expenses which prevents unintentional padding [inflating expenses] and there is no scope of inaccuracy. Additionally, certain things cannot be captured at source, especially fraud analytics, however, we have invested in a technology that analyses the patterns and numbers that people are putting in the expense reports with regards to the point of events.

There are various ways by which Concur curbs padding, such as manager and auditor approval, or keeping track of bills and tickets. Employees who do not have receipts will have to submit an affidavit which has to also go through the approval process. Lastly, we have app centre partners who provide sophisticated recording of journals and study and detect the patterns by tracking the actual number of miles travelled through synchronization with google maps. So, this is the sense of promise and vision we offer to our clients.

Neeraj Dotel, MD – Concur (India)

There are lot of fin-tech startups that are integrating payments, T&E, Insurance/Finance services, etc. into a single product, how does Concur plan to stay ahead of its competition in terms of innovation and adaptability ?

Mobile micro services is the next big thing with the ability to capture expenses at source and the ability to sync with your email and Outlook calendars. Gaining popularity amongst Indian enterprises, it will be the next big tool in business travel. Concur provides an integrated approach towards management, tracking and evaluating employee expenses. For example, hotels, airline ticketing and conveyance. We have partnered with 100 plus service providers globally and in India which includes financial integrators, payment companies, hotel and restaurants, travel management companies, cab aggregators and ground transportation companies to benefit our customers.

In the Indian context, we presume to have spreadsheets as our only competitor. Spreadsheets are typically adopted by companies who haven’t understood the concept of spend management and not figured out a way to optimize cost. Concur proposes an array of solutions to ease the management process: Invoice Capture using

SAP Leonardo

The tool helps to capture expense at its source, by letting the end user capture invoice data real time and provides a wide scale accuracy.

Expenselt Pro App

The tool has the ability to leverage several data points [card data along with OCR, user history, company history etc.] to analyse the type of expense when formulating expense reports.

Fraud Detection Analytics with Concur App centre partner Oversight

Oversight proprietary software applies multidimensional artificial intelligence techniques to monitor and report on the behaviour related to cardholders, merchants, spend categories and items purchased. The tool detects risk activity including unusual spend patterns, duplicate expenses, split transactions and suspicious out-of- pocket expenses.

Rocketrip: Real-time pricing algorithm technology

Rocketrip gives employees real time budgets and allows them to save from the estimated budget. The algorithm tracks actual prices for transportation and incorporates this information with the available budget. It provides the company with insights and analytics about travel spend, irrespective of which travel site used by the employee for booking.

Mileage Rate Service

With Concur Drive, employees will be able to automatically capture the routes travelled using GPS. The user can set days/times in order to capture their mileage. They are then provided a log of mileage that they can select the trips they wish to expense. This is seen as a huge time-saver for employees while granting approvers visibility into actual mileage and hence prevent misuse and padding.

Your views on Digital India and how that movement has paved the way for automation in Travel, Expense, Invoicing, etc.

India is in the throes of a digital transformation with digital adoption spanning all businesses across the corporate spectrum. IDC reports that work process automation in companies is leading to increased employee productivity, more cost savings and reduced time spent on expense management with a lesser propensity for errors. Automation is also resulting in better compliance practices in organizations through efficient management. A recent CFO Innovation Asia Study reveals that in India, about 39% organizations are fully automated, with online processes for employee travel and expense [Source]. Around 23% organizations use a mix of methods for travel and expense, indicating that automation is catching up in India.

Digital transformation is positively impacting the CFO’s job, in terms of value proposition, visibility, employee productivity and compliance. Concur is offering CFOs end-to-end solutions that automatically synchronize financial data across the entire employee spend process, from pre-spend approval to reconciliation. With Concur, companies can automate expenses and streamline business travel, save their employees’ time, and have more visibility into important line items, helping them focus on what matters most.

There are still lot of issues with GST [both implementation and understanding based], how does Concur support its customers to make their Bill Submission, Invoicing and other processes smoother and less time consuming ?

We have dealt with countries with similar tax reforms such as Canada, Australia, and UK and do understand the pain points associated with tax reforms. We have built experience of 38,500 customers across the globe in over 60 countries. We keep ourselves very well prepared and with the tax reforms.

With GST in India, we have been constantly responding to the need of our customers and guiding them on the impact of GST on T&E and the efficient use of budget. With end-to-end spend transparency, companies can uncover insights that lend to more effective spend management. As a result, business leaders can make smarter and more informed decisions.

We thank Neeraj Dotel for sharing his insights with our readers. If your organization is planning to adopt the more tech-savvy route to T&E functions, please have a look at Concur. If you have any questions for Neeraj or the Concur Team, please email them here or share them via a comment to this article.