The budget is significant not just for the country but you as well. That’s because it directly impacts you. The changes it makes in its taxation structure can influence your disposable income, investment portfolio and so. This is why tracking the budget can be a useful exercise. You get an idea about what to do with your income. You can plan where to invest, how to save tax and so on.

But, don’t worry if you haven’t. This article will briefly tell you how this year’s budget can affect your investment:

Equity

The Indian government imposed a Long-Term Capital Gains Tax [LTCG] of 10% on equity assets in this year’s budget. This means that if you sell the equity investment after 12 months, you will be taxed 10%. However, you are exempted from paying tax if your proceeds are not over Rs 1 Lakh. You also need to remember that the LTCG tax is applicable from April 1, 2018.

To understand the LTCG tax calculation, you need to understand the meaning of Fair Market Value [FMV] and acquisition cost.

The FMV is the highest price of a listed equity share on an exchange on January 31, 2018. If there was no share trading on January 31, the highest price quoted on the most recent trading day before January 31 will be used. The FMV for an unlisted asset like the share of an unlisted company will be its Net Asset Value [NAV] on January 31, 2018.

The acquisition cost will be the higher of the FMV or the purchase price. If the sale price is less than FMV, the acquisition cost will be the higher of the purchase price or sale price. The difference between the sale price and the acquisition cost will be the capital gain or loss.

Mutual funds

The budget has not changed the tax deduction limit of Rs 1.5 Lakh under Section 80C of the Income Tax Act. This means Equity Linked Saving Scheme [ELSS] is one of those funds that can help you reduce your taxable income.

However, the introduction of LTCG tax has complicated matters. But, you can still save tax if you are smart. As mentioned earlier, gains up to Rs 1 Lakh are exempt from tax. Once the three-year lock-in period is over, sell units partly in a way that your gains do not exceed Rs 1 Lakh in a financial year. This method can help you earn an income every year without paying taxes! You can also choose to reinvest the proceeds in a new ELSS scheme.

Retirement planning

A person turning 60 years can withdraw 60% of the corpus held in a National Pension Scheme [NPS] account at maturity. About 40% of the corpus is exempt from tax. The tax exemption benefit is meant for salaried employees only. The benefit is extended to all subscribers of the NPS scheme from April 1, 2018.

Fixed deposit

Until now, the tax exemption limit for interest earned from post office and bank fixed deposit was Rs 10,000. But this limit will be raised to Rs 50,000 from the next financial year. The tax benefit is applicable to recurring deposit schemes as well.

To sum up

Now that you are aware of the tax impact on each asset class, you can start with investment planning for next financial year.

Ace director and writer Vikram Bhatt announced his venture into the digital space with the launch of his OTT platform called VBontheweb, which brings forth a Theatre on the Web, concept where one pays only for the premium show one wishes to binge watch. Joining him was family friend Mahesh Bhatt who came in his support to encourage Vikram’s new foray. The VBontheweb app was launched on the platform hosted by Brightcove, one of the pioneers of online video streaming and has been developed by Ecreeds.

This is India’s first OTT platform to promote the concept of bringing cinema to the mobile phone with its unique subscription model. It allows users to buy a pass to watch a show/entire series for a fees as nominal as INR 18. This is the first time in India that the viewers would get to pay for particular shows only which they desire to watch and not the entire application. With this, Vikram Bhatt wishes to bring about a substantial change in the digital space and give a choice to the viewers.

Also what sets this platform unique is the opportunity it will be giving to other filmmakers, the power to find a platform to put up their content on the app as a synergy to give them access to a platform where their content can be displayed. The app launched with original series ‘Untouchables’ directed by Vikram’s daughter Krishna Bhatt. Untouchables is a courtroom drama inspired by real life events. The shows available on the app include Maya, Twisted, Rain, Tantra, Hadh, these shows can be viewed free of cost.

Vikram Bhatt commented

We are not leaving any stone unturned to making it big for VBontheweb app. Our digital venture premiered Untouchables which is special to me because it my daughter Krishna’s directorial debut, and it makes me feel extremely proud. Digital is the future and it has arrived, we are ready to seize the day.

Speaking about the app launch, Krishna Bhatt said

Launching VBontheweb app is a big step we are taking to capture the OTT platform. The series of programming also includes Untouchables which is my directorial debut and has already received appreciation from the audiences. I am hoping this platform will become a digital sensation, and I am excited to see the progress.

VBontheweb is currently available to download on Android and iOS platforms.

We are honoured and humbled to have received this recognition, which is testimony to the fact that a passionate team, that sets out to solve real issues and doesn’t deviate from its vision despite market forces, makes for a successful organisation. Our drive and commitment to transform the grocery delivery industry in India is relentless and year 2018 will be a transformational year for Milkbasket and the industry.

The Startup of the Year award is dedicated to young SMEs, aged seven years or less, with great potential to become big in local / international markets. Considered as the most coveted awards show complementing the league’s best across SMEs, SMB and new and emerging small scale ventures, Small Business Awards 2018 were organised by Franchise India Group. The award ceremony was hosted in New Delhi.

About Milkbasket

Launched in early 2015, Milkbasket is India’s first and largest daily micro-delivery service. Built on the unique Indian habit of getting fresh milk delivered at home every morning, Milkbasket is today fulfilling the entire grocery needs of a household everyday before 7:00 a.m. To enable frequent and frictionless buying, Milkbasket has innovated flexi-ordering and contactless delivery – both a first in the ecommerce industry – and favourites of Milkbasket customers. Founded by INSEAD alumnus Anant Goel with his co-founders Ashish Goel, Anurag Jain and Yatish Talvadia, Milkbasket delivers only in select areas while expanding its network with new launches every week. With an order fulfillment rate of 99%, customer retention rate of 95% and on-time deliveries of 99.9%, Milkbasket has redefined the industry benchmarks and enjoys envious customer loyalty. For more information, please visit Milkbasket.

Koinex, India’s most advanced digital assets exchange, will now be accessible for users on their smartphones through a new app feature launched by the company. The app will be available on Android now, while the iOS version will be launched shortly.

The app version offers ‘personalized price alert’ which will help users to know when their crypto-currency has hit their desired price listed on the exchange. Koinex is the first exchange app to pioneer this feature, in the crypto-currency segment in the country. Other distinctive features include three step security verification, graphical chart representation of industry trading and an extensive log book for users to plot the current crypto-currency valuation. The app also offers users, the feature of scanning QR code to connect to their payment wallet, which again is a unique feature, apart from the seamless interface allowing them to maneuver through multiple sections on the app.

Talking about the app launch, Rahul Raj, Co-Founder, Koinex said

The smartphone adoption in the country has made it inevitable to have an app service. We have been traders ourselves, and we are working to solve the pain known to all of us, one step at a time. The platform currently is the largest digital assets exchange in the country in terms of trading volume and we want to further accentuate our user experience by allowing them to track and trade at Koinex, on the go.

The key challenge was to create an interface that can sustain the enormous trading volume we have on the portal. The app also has been built using our innate tech expertise and we strive to improve Koinex, build more trading tools, develop more blockchain products, and create a holistic crypto-currency trading ecosystem.

Koinex is the first multi-currency exchange with an open-book ledger format, in the country and it began operations in August 2017. Within a short span of five months, the company grew to be one of the largest trading portal by volume, in the country. Few of the key reasons for their success are their cutting edge technology, proprietary trading engine, wallet and platform architectures, grade A security, user-centric UI/UX and tons of user-demanded features that makes it seamless for the users.

The tremendous growth volume is indicator to the scalability and long tenure of the brand in the market. Today as per industry rankings, Koinex stands among the top 50 exchanges globally and is the only Indian exchange in the list. Koinex aims to make India a hotbed of blockchain technology development and adoption.

About Koinex

Koinex is India’s first and most advanced crypto-currency trading and exchange company. Incepted in August 2017 in Mumbai, the web platform facilitates real-time trading of multiple crypto-currencies like Bitcoin, Ethereum, Ripple, and Litecoin. By operating on a peer-to-peer exchange model, the live, open order book exchange enables users to discover the best price. Koinex facilitates simple on-boarding with quick e-KYC, and enables users to instantly start transacting in their preferred crypto-currency. For more information, please visit Koinex

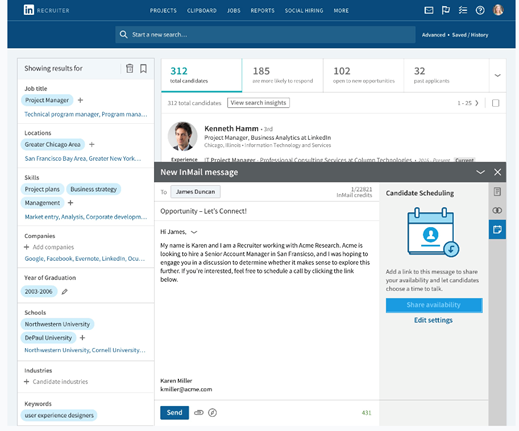

One of the biggest pain points for recruiters and candidates is locking down on a time suitable to both for an interview. Scheduling a time to setup an initial interview is often burdensome, time-consuming and can lead to candidates dropping off from the hiring process due to the back and forth.

To ease the hiring process and avoid fallout’s, LinkedIn launched ‘LinkedIn Scheduler‘, a tool that automates initial interview scheduling for recruiters and candidates, directly via InMail. It helps candidates and recruiters save time spent on scheduling a meeting and helps recruiters focus their energies on hiring strategically and on-boarding the best candidate.

LinkedIn Recruiter

Using this feature, candidates or recruiters can reach each other via InMail to see one’s calendar availability and reserve an interview time that works best for both. It also gives candidates the liberty to feed in their contact information to accelerate this process.

Here’s how it works

First, recruiters are prompted to sync their calendar [Office 365 or Google Calendar] with LinkedIn.

Then, using a new InMail message, recruiters can easily send a scheduling link directly to the candidate of interest.

The link shares a real-time view of the recruiter’s calendar availability with candidates who can then choose what time works best for them, add their phone number and confirm the meeting.

Advance settings allow recruiters to manage preferences such as time zones, availability, length of meetings and same-day meetings.

Candidates can easily and automatically reschedule meetings with the recruiter through the confirmation link.

A very famous quote on investing says – ‘Risk & Rewards are two sides of the same coin’. This means that in most of the cases, higher the amount of risk involved chances of maximizing the returns are also very high! The investment portfolio of every person would differ since it is dependent on various factors like risk appetite, assets, liabilities, dependencies, etc. and hence, it becomes virtually impossible for any investment firm to cater to varied investment requirements of such a large audience.

This is where emerging technologies like Machine Learning and Artificial Intelligence can play a vital role in creating a tailor-made investment plan based on your long-term and short financial requirements. Machine Learning has already the paved way into the Fintech market, be it approving loans, documentation, managing assets, etc. Many Fintech startups are leveraging machine learning, AI, Chatbots and helping banking institutions to either enhance the existing banking experience or creating kick-ass products in the areas of wealth management, personal finance, customer service, etc.

According to a report by Bloomberg, less than 1.5% of the Indian population invested in equity markets and only 2% of India’s household savings were exposed to equity. However, there is a rising interest to invest in financial instruments like Mutual Funds if they are given proper guidance.

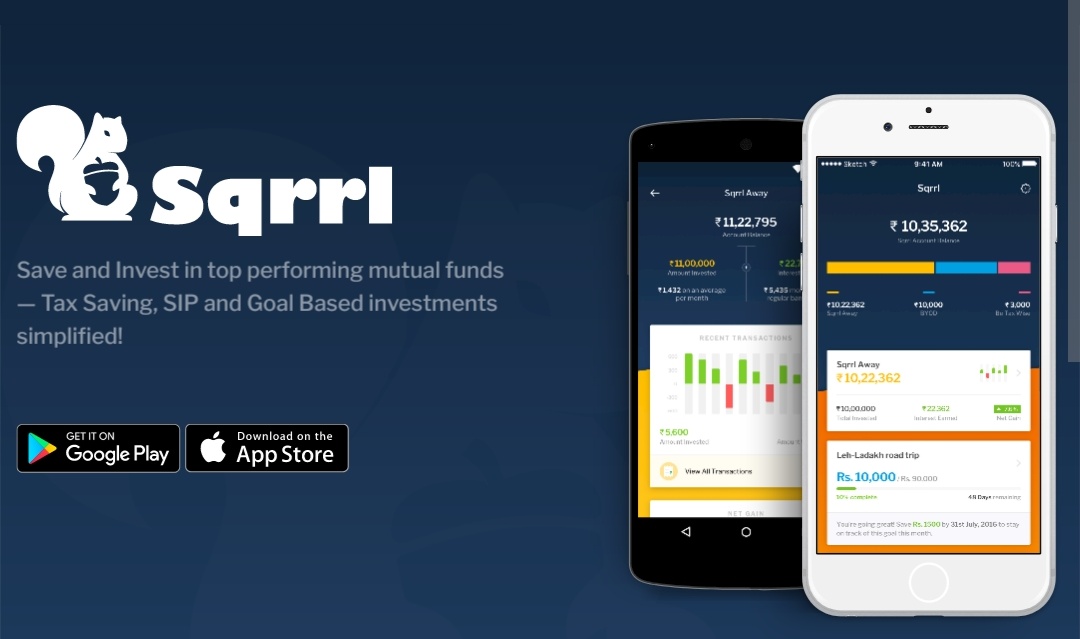

This is the problem being solved by Sqrrl, a Fintech startup that was incubated at Reliance GenNext Hub and seeks to help young people save & invest in Mutual Funds in a hassle-free manner. Sqrrl also recommends great tax saving investments for its customers, keeping in mind a seamless experience. All this with the aim to help young Indians financially prosper! Today we have a chat with Mr. Samant Sikka, Founder of Sqrrl about the app, Fintech, Personal Finance, etc. so let’s get started with the Q&A…

How did your team come up with the idea of Sqrrl ?

Having spent almost two decades in financial services domain one was constantly exposed to challenges of building distribution in a country as diverse as India. I was always intrigued by the fact that in spite of six decades since independence financial services ecosystem was still struggling to provide access of financial services to its citizens. To my mind the single most important reason that came in the way of expanding financial services footprint was ‘Unit Economics’. Unit economics basically dictated who got access to financial products & services and also which type of products got sold.

Sometime in 2015 I started to absorb the impact that culmination of technology & internet was starting to have on democratizing ‘access’. E-commerce was starting to grain traction and people started getting access to goods and services hitherto restricted to larger cities and towns. 2 things stood out, given the economic prosperity over the 2 decades people had both aspirations and means to consume and were demanding better experiences. Internet had started to travel deeper in the country and social and digital were starting to have an impact on consumers behavior and consumption patterns.

Meanwhile, silently but surely there the impact of #RegTech and benefits of India Stack which were started to make tremendous traction on the two biggest friction areas in financial services, on-boarding & payments. The timing seemed to be just right neither too late neither too early.

Can you take us through the founding team of Sqrrl ?

Putting the challenges & opportunity together gave birth to the idea of Sqrrl. The vision being to build a digital platform aimed at millennials with an Initial offering is around savings & investment products powered by Mutual Funds and will expand to Loans, Insurance, Payments ultimately aspiring to morph into a digital bank. The idea aligned the founding team which brought wealth if experience & complementary skills sets .

Sqrrl is an interesting name for a ‘Fintech startup, how did you zero in on the name and how does the brand ‘Sqrrl’ get along with the moto of ‘building financial literacy among Indians’ ?

Sqrrl name was chosen with care. The animal embodies certain character that we stand for

Doer and Prudent,

Natural Intelligence,

Hi-Energy-Active-Nimble,

Saver and plans for future. hoards for winters in summers,

Good at balancing work & play,

Social

What is the TAM of the Fintech market that Sqrrl is trying to address ?

India’s Asset management Industry has grown at a CAGR of 21% over the last 17 years [ 2000-2017] is expected to grow to USD 700 billion by 2022.

Sqrrl aspires to be amongst the Top 10 players by 2022 with an Asset Under Management [AUM] of approx USD 14 billion and 12 million customers

There are number of Fintech platforms that are targeting a similar problem [as well as market], what according to you are some of the core USPs of Sqrrl when compared to its competitors ?

Sqrrl is different from existing players in many ways. Important ones are highlighted below:

Sqrrl has a customer persona which is in the age group of 25-35 years, salaried class, upwardly mobile and digitally savvy.

Sqrrl is a not a marketplace unlike many others. We personalize investments needs of individuals and match them with funds available in the industry.

Can you please walk us through the funding of Sqrrl ?

We have been bootstrapped from beginning of our journey. We are currently in funding raise discussion of about 1M USD with some VCs.

Once user has created an account on Sqrrl [and all his investments from various AMCs are under one window], what other services does your team provide to the investors so that they can get more returns from their investments ?

Sqrrl keeps monitoring all of the funds recommended by its team. We stay with our customers in their investment journey and keep guiding him with right decisions from time to time.

Can you give a small glimpse about the tech behind Sqrrl ?

We are app only offering on iOS and Android

Our API layer is powered by Python [Falcon framework]

Our database is AWS RDS on PostgreSQL

Other than this we use many third party APIs

Sqrrl is currently limited to Mutual Funds, are there any plans/timeline on whether it would be expanded to cover other financial instruments ?

Yes, we have plans to launch loans and insurance products in future.

What are some of the methodologies that your team use in order to keep the investors hooked on to the platform ?

We have a way to connect with customers in 360 degree way. Our customer success team keeps talking them on Email, Phone, SMS, Whatsapp in addition to in-app communications.

Sqrrl was incubated in Reliance GenNext Hub, how was the experience in the accelerator program and how did the program help your team to validate & scale the startup ?

The program was really of great help in helping us with product market fit study and beyond. They really helped in methodical product market fit. In addition to product market fit, customer traction strategy and its execution planning was done with them.

Are there any setup charges or any other charges that customers have to pay to use the Platform ? Do you charge any withdrawal or closure charges for the Sqrrl’s recommended funds ?

There are no setup charges to use Sqrrl. However there may be early withdrawal charges for some funds before initial lock-in period.

Which are some of the AMC’s that are currently on-boarded on the Sqrrl platform ?

There are 17 AMC that are there with Sqrrl. It covers 91% of the industry AUM

As you have mentioned earlier, Sqrrl aims to encourage Indians to save more. There are various investor initiatives like #MFDayon7th by Reliance MF and CNBC TV18, does Sqrrl have plans of starting an investor education initiative [or something else] in order to widen the horizon of passive investors [that could be an integral part of the investors eco-system, but don’t know where to get started] ?

The ecosystem is doing a great job in educating investors. AMFI is doing great job in communication like ‘Mutual Funds Sahi Hai’. AMCs themselves have different plans. Sqrrl plans to use these and some of its own to launch education awareness. We are working on them.

Many fintech companies, namely PayTm [or PaytmMoney], FreeCharge, PhonePe, etc. are planning to have boutique of finance products on their platform, does this growing competition have an impact on a startup like Sqrrl and how it would the competition result in expansion of the fintech ecosystem ?

It is good that this space is getting its validation by entry of bigger players. There will always be space for early movers like Sqrrl based on its customer service differentiation.

Can you comment on the ‘Customer/Investor’ demographics that are currently using the Sqrrl Platform ?

90% of the users are under age 40 years.

61% of the users are from B15 [beyond top 15] cities.

We have coverage from over 700 cities of India.

What is the revenue model of Sqrrl and does it follow the Freemium model ?

We get distribution fee from the underlying Mutual Funds.

Along with the integrated AMC approach, building investor portfolio as per his requirements, etc. does your team also provide advisory services ? If not, what are some of the services that you plan to offer in future [especially with the Mutual Fund Products] ?

We are not providing advisory services now but we are open to embrace this in future.

How Fintech is shaping up the Financial Eco-system in India and how technologies like Blockchain will bring the next wave of Fintech revolution ?

Blockchain and its acceptance is in very early stage. Most of the work is happening in Crypto exchanges. We are open to exploring something on blockchain which is widely accepted.

Some books that you highly recommend for entrepreneurs

Zero to One by Peter Thiel

The Lean Statup by Eric Ries

Traction : How Any Startup Can Achieve Explosive Customer Growth by Gabriel Weinberg

Some closing thoughts for our readers!

As Bill Gates says, ‘If you are born poor its not your mistake, But if you die poor its your mistake.‘ Sqrrl is a platform available for every Indian to manage their money.

We thank Mr. Samant Sikka for sharing his insights with our readers. If you are planning to put your money to work via smart investments, then you should download Sqrrl. If you have any questions for Samant or the Sqrrl Team, please email them here or share them via a comment to this article.

‘Ownership’ is a word that has a lot of sentiments attached to it. Whether it is owning a commodity like a car, bike, mobile phone, electronic appliance, etc. or owning a house, it brings a deep sense of accomplishment to the owner. Many years back, owning either of them would be considered a herculean task, but with the rise in urbanization, increase in the overall disposable income of the urban Indians, changing lifestyle and easy access to financial tools [like Equated Monthly Installment], the rate of consumption has increased rapidly.

If a consumer has a good financial track record and an exceptional CIBIL score, getting a home loan/personal loan/vehicle loan is a piece of cake and consumers can pick and choose from the best possible options, since financial institutions do not want to lose the customer and they would try their best to retain/bring a new customer on board. However, EMI comes with a baggage full of responsibilities and missing the EMI on a consistent basis can have serious implications on your financial track record. In some scenarios, you might be looking for a short-term loan or a relatively smaller amount for which you might not want to take a bank loan. In such scenarios, you either lend money from family, friends or from companies operating in the burgeoning fintech sector.

The overall financial landscape is also changing at a very rapid pace in order to accommodate the changing sentiments of the customers. Innovations like Unified Payments Interface [UPI], India Stack, India Chain, push towards Digital India, increasing internet penetration, etc. have resulted in many innovations in the Fintech Space. Though startups catering to Payment services [PayTm, FreeCharge, PhonePe, etc.], P2P Lending [LendBox, EasySalary, etc.], Personal finance [BankBazaar, Capital Float, ScripBox, etc.], Lending based on credit-line [MoneyTap] have resulted in major customer and investor interest, there is still a lot of room for innovation in the fintech sector. In many cases, Banks and Fintech players are working together and utilizing their relevant expertise to create a better experience for their customers.

#SmartlyOwn – Better Option to Own Things

As reiterated earlier, ownership brings a sense of pride, but it comes at a cost. Though consumers have options to buy furniture, bike, electronic appliances, etc., by utilizing the financial services of banks as well as fintech companies, they still have to worry about repaying their loan on time. Unlike in the past, young population is more comfortable to switch cities in case they find better career opportunities. In case they opt for relocation, they need to take the important decision on whether they carry the commodities they own like car/bike/electronic appliance along with them or sell them at the best possible price. Since each of these is a depreciating commodity, hence their overall value depreciates from the very moment you own them.

Hence, consumers need to take the important decision on whether they need to own them or use options like ‘renting’ so that they can save money and #SmartlyOwn the items. This is the problem being solved by new-age rental companies that are using technology to offer better options to their customers. Even if you own a house, you still need to worry about setting up the home and good home interiors might burn a hole in your pocket. L Rather than blowing up hard-earned savings in owning up such items, the millennial generation has better investment options like Mutual Funds, Stocks, CryptoCurrency, etc. Due to all these factors, many urban Indians are switching to a #SubscriptionLifestyle since they have options to rent bikes, appliances, furniture, etc.

RentoMojo – Consumer Leasing Company to a Fintech Startup

Rentomojo, India’s leading consumer leasing company has various plans so that customers can buy a bike, furniture, electronic appliances on rent for a minimum period of three months. Founded by IIT alumnus Geetansh Bamania, RentoMojo is a first-of-its-kind consumer product leasing business that raises lease-capital from financial institutions for products rented to consumers for long-term periods, typically 12-18 months.

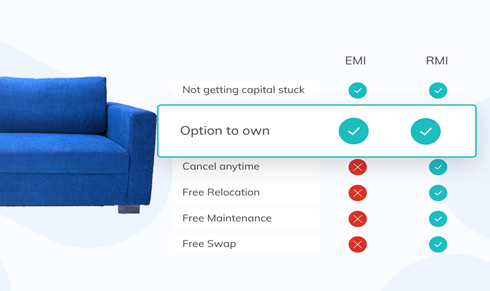

With an option like Rental Monthly Installment [RMI], you can own a product like a piece of furniture, a bike or an appliance without being bonded with a lifetime commitment. How is RMI better as compared to EMI? There are so many benefits that come along with it, which are not available with EMI and flexibility and non-commitment to the products is the biggest of them. You can take the products till the time you want and return when you don’t. The other important benefits include free delivery and maintenance, a swap of the products and much cheaper payouts monthly as compared to EMI. This is how the concept has broadened to a wide universe of the customers who have always considered renting as a financial decision.

Since many customers rent products for a long-term period of 12~18 months, they might want to increase the rental tenure or own the products as well, making a lot more financial sense. This is the thought with which they announced an exciting proposition of Rent-to-Own [#RentToOwn], where now the customers will be able to rent till whatever time they want, return or own the products. This is a whole #NewWayToOwn!

#RentToOwn – A Smarter Way to Ownership

Though it was started as a rental business, Rentomojo has evolved as a fintech model where the customers can lease furniture, appliances, and two-wheelers by paying an extremely affordable RMI. With the new offering of ‘Rent-To-Own’, the customers will have a new way of ownership, where after paying some RMIs if the customer feels like buying the products, it can be done. Customers also have an option where they can ‘try and then buy’ through product trials at their doorstep.

Eminent content contributors were invited for the launch of this event where the idea and concept was introduced for the first time to a larger audience. Sharing his views on being the first fintech startup to have this feature, Geetansh Bamania, Founder & CEO of Rentomojo, said

Usually renting is considered for a longer duration. A lot of customers also get a strong sense of ownership once they buy the products. What we also realized that, although the perception of renting could be for a smaller duration, the average rental tenure of our customers is 12-18 months, which itself makes us very different than a typical rental model. With an option of owning if the customer wants to after he has rented, where he is paying a nominal RMI, is a new way of ownership.

The below table summarizes the advantages of RMI as compared to EMI and ‘Option to Own’ is definitely a feature that would lure customers who rent for a longer duration since they now have an option to own the item they have been using on rent!

Some of the questions asked during the launch event were:

Should customers opt for renting items even if they have the financial capability to own them?

Since Rentomojo provides ‘Free Maintenance’, how does it educate its customers about product quality so that maintenance expenses are kept to the bare minimum?

Who are the partners of Rentomojo in the bike, electronics appliance sector?

Does Rentomojo plan the omnichannel route in future so that customers can also get a touch and feel of the products [especially the furniture]?

Does Rentomojo service only the B2C sector or they also have B2B customers?

What are some of the unique offerings of Rentomojo as compared to other companies operating in the same sector?

Geenatsh Bamania explaining the ‘RentToOwn’ concept

Geetansh and his team answered all these questions with ease since they are very confident about their offerings. Since their team has extensive experience in technology, e-commerce, retail, their main focus has been on unit economics rather than chasing a vanity metric like Gross Merchandise Value [GMV].

What are your thoughts about the RentToOwn concept? Do leave your feedback in the comments section.

Eduvanz Financing Pvt Ltd, a skill development loan provider, has announced that it has been granted the NBFC Licence by the RBI to start providing Loans in the multi-billion skill development sector. The Firm has raised $500,000 investment led by Blinc Advisors. Eduvanz will utilize the funds for strengthening it AI based Lending technology for loan appraisal and expands its operation pan India.

Eduvanz is a pioneer in using proprietary AI-based algorithms and complex predictive analytics to collate financial & socio-economic data from conventional and non-conventional sources to make lending easier for skill development. A successful pilot phase where over 12000 leads worth over $8 Million were assessed to fund over hundreds of students, Eduvanz has validated its concept.

With the non-banking financial company [NBFC] status approval from the Reserve Bank of India [RBI], Eduvanz is bringing much needed financial support in the Skill development ecosystem using analytical tools and advanced risk management capabilities to extend loans without any paperwork in a matter of minutes.

Varun Chopra, Co-founder, Eduvanz Financing Pvt Ltd, said

We are solving problems that are directly linked with nation building and growth of Indian Industry. Over the next four years, more than 200 million Indians will undergo some form of skill training before they enter the work force. At Eduvanz, our mission is to financially empower every individual to chose the vocation, skills and career of their choice.

With this approval from RBI, Eduvanz has moved one step closer to becoming India’s leading lender for vocational courses, on-job training programs and certifications programs.

??Eduvanz works with Training Partners, Top Corporates and Certification Providers spanning more than 16 Industry Sectors to increase their enrollments by providing innovative financial solutions to students and skill-seekers looking to skill up for their careers.

About Eduvanz Financing Private Limited

Eduvanz is a innovative finance company, which is completely revolutionizing the educational loan market. Eduvanz has won the the Judges Award at the Wharton Indian Economic Forum’s Startup Challenge where it competed with over 500 other start-ups. For more information, please visit here