Start-up culture is at its’ boom in India. Start-up attracts Venture Capital [VC] or Private Equity [PE]. VC/PE investment sometimes requires hiring specialists. For Start-ups, it’s not easy to offer competitive pay to attract talent. Employee Share Option Scheme [ESOP] as part of salary package offered, comes in handy. At other times, ESOP is offered to retain talent and give a sense of ownership.

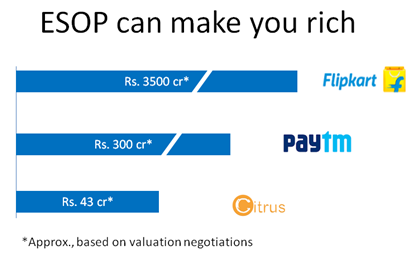

Flipkart deal has showered fortune on its employees holding shares under ESOP. Paytm and Citrus are other examples. But it’s the positive part of the story. Some startups shut down after receiving investment. Their ESOPs never get listed on any exchange or are bought back by any investor. ESOPs are not always about startups. Most of the big corporate like HDFC, ITC, Wipro, L&T etc. have awarded shares to recognize and reward employees.

Like many other things, ESOP story is two sided as well. This article talks about ESOP from employee side. The article will cover following aspects of ESOP:

- What is an ESOP?

- ESOP as part of offered package [Remuneration negotiation]

- Eligible employees

- Procedure of ESOP

- Pricing of ESOP and lock-in period

- Taxation

- When you losses your rights under ESOP?

- ESOP vs bonus

In the following article, we will discuss ESOP from the view of employer i.e. company.

What is an ESOP

ESOP is usually known as Employee Stock Option Plan in legal terms it may be called by different names as

- Employee Stock Option Scheme

- Employee Stock Purchase Scheme

- Stock Appreciation Rights Scheme

- General Employee Benefits Scheme

- Retirement Benefit Scheme

By whatever name called, all the above schemes offers shares/securities of the Company for direct or indirect benefits of its employees. Here the important thing to be noted by an employee is that the ESOP needs not to be necessarily offered by the Company at whose payroll you are working. You may also receive ESOP from your holding company or from any other company of the same group.

In layman’s language an ESOP is an offer given to employee by his employer to buy shares of the Company at a predefined price and in a phased manner.

ESOP as part of offered package [Remuneration negotiation]

Always analyze risk associated with accepting an offer having ESOP. Startups are unlisted entity. So, ESOPs by startups will not have liquidity as is available in case of listed entities.

Pay package is often structured such that shares under ESOP are granted at the end of first year [like retention bonus] and then you must wait for vesting period of shares to benefit from share grant. This means you are investing for long term.

Last but not the least, under ESOP, shares are not given to you for free. You must pay the predefined purchase price. If all does not go well with the organization, the predefined price may be a higher price than the face value and market value of those shares, resulting in loss of speculated gain. Though, we all know that higher the risk the higher the gain.

ESOPs can be offered only to permanent employees.

My advice is to take calculated risk. Research ESOP grant timing, purchase price, eligibility and vesting period before accepting ESOPs as part of pay package.

Eligible employees – ESOP can be offered to below types of employees

- A permanent employee of the company who has been working in India or outside India

- A director of the company, whether a whole time director or not, but not to an independent director

- An employee of holding company

Options under ESOP can’t be granted to promoters or person belonging to promoter group.

Most inquired questions about ESOP is – Can the new employee receive options under ESOP? Well, Compensation Committee of a company has the power to decide who will receive options under ESOP. A company is free to decide criteria for granting ESOP. ESOP scheme may be structured in a manner that option can be granted to senior employees to reward their loyalty, to young talent to retain them and to new employees to attract talent.

Procedure of ESOP

The implementation on ESOP consists of three steps-

- Grant of option

- Vesting of option

- Exercise of option

Let’s take an example. Mr. A received 100 no. of options from his Company which will vest @25% each year from the end of first year of grant.

Here no. of grant is 100. Vesting each year at completion of one year of receiving of grant will be 25. Mr. A can exercise his right to buy shares/options so vested at the end of each year. Please note Mr. A can’t buy the shares/options before their vesting.

Some employee wonder if they can claim the difference in the share price [i.e. ESOP price – Market price] on exercise date. It can be done only if ESOP is managed by a trust, securities of the company are listed on stock exchange and ESOP scheme has such provision.

At the time of receiving ESOP always check whether your Company is listed or unlisted and options so received give you right to invest in shares of your company or your subsidiary/holding/group company. Please remember that shares of unlisted public company or private company can’t be sold in stock market. In that case, the only liquidity left is when an investor of the company is ready to buy those shares or the company itself decides to buy-back its own shares.

Pricing of ESOP and Lock-in

As an employee you are not going to receive any free share under ESOP. Exercise price is the price at which you can buy the options vested in your name. Current regulation gives freedom to the company to determine the exercise price provided accounting regulation is taken care off. Thus, the company can give you shares at discounted price.

ESOP scheme may specify a lock-in period. Lock-in means after buying the shares under ESOP you cannot sale it till the lock-in period is over. This is usually one year from the date of exercise of option.

- Taxation – Shares purchased under ESOP are taxed twice:

- At the exercise of option – At the time of exercise of option the price difference between the Fair Market Price of said shares and the exercise price is treated as perquisites in the hands of employee and shall be taxed under the head income from salary. That tax will be deducted at source by the employer and will reflect in Form 16 of the employee.

- At sale of shares – ESOP shares will be liable for short-term capital gain or long term capital gain as the case may be, at the time of sale. For calculation of tax the price difference between fair market price at the date of sale of shares and the fair market price at the date of purchase of these shares will be considered. As at the time of purchase the difference between exercise price and fair market price would have already been taxed as perquisites.

When you lose your right under ESOP

If you retire, resign or die, ESOP is governed by specific terms of scheme. Below is a general discussion of these circumstances

i.) Termination – The options not vested on that date expire. Options already exercised by the employee, remain with the employee. A period is provided for exercise of options already vested.

ii.) Resignation – The options not vested on that date expire. Options already exercised by the employee, remain with the employee. A period is provided for exercise of options already vested.

iii.) Death or permanent disability – All the granted options will immediately become vested in the name of legal heir of the employee to whom the options were granted.

As an employee you shall also check the clause for treatment of bonus/right shares, if any, offered during the period of grant till the time of exercise of option. Effect of change in capital structure or corporate restructuring like mergers/amalgamations shall also be checked.

ESOP vs bonus

Indians prefer higher package or bonus than ESOP. ESOP only gives an option to invest in shares of the company at a pre-determined price. If ESOP is granted as a reward for your loyalty or to retain your without compromising the bonus or incentive structure, it is an added advantage.

Note – The article was originally published here and is reproduced with author’s consent. The author is Nikita Singh who is a Corporate Legal Advisor with expertise in overseas acquisition, IPO, ESOP, M&A, buy back and share swap FEMA compliance. She is attempting to make the legal world a layman’ walk through her articles and extensive exposure to corporate world. She can be contacted here and her LinkedIn profile is here.