MoneyTap [Earlier coverage – MoneyTap review, Q&A with Bala Parthasarthy], India’s first App-Based Credit Line is now available in Kannada for the people of Bengaluru. MoneyTap, which is offered in partnership with banks, enables consumers to get instant credit from partner banks at the tap of a button on the app. The App was launched in English last year and since then has already issued close to 20 crore in credit in Bengaluru alone. The company is also planning to launch the app in Hindi and Telugu soon.

Largely focusing on the vastly untapped Kannada speaking users, the app will allow Bengalureans to avail up to INR 5 lakhs through an easy eligibility process. The company is enthusiastic about their plans to tap into the local market. According to the 2011 Census, Bengaluru’s population is over 10 million and 71% of the population speaks Kannada.

MoneyTap is available on Android Playstore and is targeted at salaried individuals and self-employed professionals earning more than INR 20,000 per month.MoneyTap evaluates the user’s eligibility in less than 4 minutes after which it provides an instant, real-time decision on the application along with the amount they are eligible for.

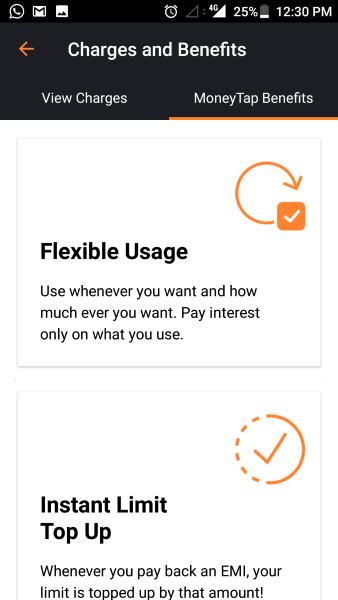

Using the credit line, consumers can choose to borrow as little as INR 3000 or as much as INR 5 lakhs or up to their maximum eligibility limit. Customers can decide their own EMI plans with flexible payback periods ranging from 2 months to 3 years. Interest is paid only on the amount borrowed and rates can be as low as 1.25% per month. If the user does not borrow any amount, then no interest needs to be paid. The credit limit also gets topped up once EMIs are paid back.

MoneyTap along with RBL Bank is able to provide its customers, instant decisions and instant access to money, 24/7. All financial transactions such as billing and repayment are directly dealt with the bank but through the MoneyTap App using secure APIs, thus ensuring 100% secure transactions. As an added convenience for shopping needs, a MoneyTap RBL Credit Card is also provided for the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

The Bengaluru-based startup recently raised a total of $12.3 millionin funding from Sequoia India, NEA & Prime Venture Partners. The credit line is offered in 14 cities across India and the company plans to expand to 50 cities in India by the end of 2017.

We are very enthusiastic about launching our app in Kannada. Bengaluru is one of our biggest markets. Our aim is to reduce the hassles of obtaining credit from banks and in many cases, the paperwork and verification process can delay the process by months. From small business owners to salaried professionals, all require credit at some stage in their life and we want to ensure that credit is available to them whenever they need it, on a tap!

About MoneyTap

MoneyTap is a Bengaluru-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish (sold to Hewlett Packard), which he helped grow to 100M users and $300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 (now Prime Venture Partners) where he helped create companies like ZipDial (sold to Twitter), EZETap, Happay, etc. Kunal (ex Texas Instruments) & Anuj (ex Airtel & JWT) co-founded Tapstart that grew to 300K users and turned profitable in 2 years. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap

As a testament to its continued popularity among its users, MoneyTap is on target to issue credit lines worth INR 300 crores by the end of the current fiscal year. With this fresh funding, MoneyTap plans to solidify its leadership position by improving credit accessibility for other segments of customers, partnering with 6 other Banks and NBFCs and expanding to 50 cities in India by the end of 2017.

Since its launch in September 2016, India’s first app-based consumer credit line has attracted over three hundred thousand [300k] users. The majority of users have a monthly income of INR 30,000~40,000 and are aged between 28~32 years.

The Indian consumer finance market is estimated to grow at a compounded growth rate of 18 percent to become a USD 1.2 trillion opportunity by 2020. Reports also suggest that it is also one of the most underpenetrated markets for lending, with close to 70% of the population being underserved by institutional lenders. Penetration of unsecured personal loans has been extremely poor in India with the organized credit presence at around 1% in the country.

According to RBI data of August 2016, in a country of 1.2 billion Indians, only 26.4 million have credit cards. Comparatively, there are about 600 million active mobile phones in India and mobile banking transactions rose from Rs 4,185 billion in 2012 to Rs 5,243 billion in October 2016. All this data points out to the fact that consumer-lending startups such as MoneyTap, supported by financial institutions, can serve a huge creditworthy but financially excluded customer base previously overlooked by the lending businesses.

MoneyTap is available on Android Playstore and is targeted at salaried individuals and self-employed professionals earning more than INR 20,000 per month. MoneyTap evaluates the user’s eligibility in less than 4 minutes after which it provides an instant, real-time decision on the application along with the amount they are eligible for. Using the credit line, consumers can choose to borrow as little as INR 3000 or as much as INR 5 lakhs or up to their maximum eligibility limit. Customers can decide their own EMI plans with flexible payback periods ranging from 2 months to 3 years. Interest is paid only on the amount borrowed and rates can be as low as 1.25% per month. If the user does not borrow any amount, then no interest needs to be paid. The credit limit also gets topped up once EMIs are paid back.

MoneyTap along with RBL Bank is able to provide its customers, instant decisions and instant access to money, 24/7. All financial transactions such as billing and repayment are directly dealt with the bank but through the MoneyTap App using secure APIs, thus ensuring 100% secure transactions.

These are exciting times at MoneyTap. We deeply believe that the rapidly growing middle-income group in India is largely underserved by financial institutions. They are app-savvy and very demanding. We have been fortunate to partner with Sequoia, NEA & Prime – all of whom are top tier investors with deep fintech and operational expertise to take us to the next level.

Abheek Anand, Principal, Sequoia Capital India Advisors said

Consumer credit in India is highly under-penetrated and is a complex problem to solve. MoneyTap combines an experienced team with a thoughtfully designed product – and their strong early traction is a testament to the efficacy of their approach to address this massive market opportunity.

MoneyTap is using the power of technology to provide a seamless lending experience to what currently is a largely broken discovery process with long execution timelines for consumers. Also, MoneyTap works with banks & NBFCs instead of competing with them therefore getting access to large amount of lending capital while managing the consumer journey throughout the lending lifecycle.

MoneyTap’s strong growth since its inception is testament to both the innovative nature as well as rapid consumer adoption of their solution which addresses a monster opportunity – providing effortless credit to worthy consumers entirely through an app. We are privileged to be associated with this stellar team from the start of their journey and be part of their vision to reinvent the unsecured consumer lending landscape.

About MoneyTap

MoneyTap is a Bengaluru-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish (sold to Hewlett Packard), which he helped grow to 100M users and $300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 (now Prime Venture Partners) where he helped create companies like ZipDial (sold to Twitter), EZETap, Happay, etc. Kunal (ex Texas Instruments) & Anuj (ex Airtel & JWT) co-founded Tapstart that grew to 300K users and turned profitable in 2 years. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap

MoneyTap[earlier coverage MoneyTap Review and Interview with Bala Parthasarthy, CEO – MoneyTap], India’s first app-based consumer credit line along with its partner RBL Bank, announced that the credit line is now available for Self-Employed professionals. The opening of the new segment is in line with the company’s plans to expand into 30 cities in India over the next six months. After lowering the minimum salary eligibility to INR 20,000 per month, this is MoneyTap’s next move to enable easy access to credit.

In a country of 1.2 billion Indians, 26.4 million have credit cards as of August 2016, according to RBI data. The penetration of unsecured personal loans has been extremely poor in India with the organized credit presence at around 1% in the country. On the other hand, according to a survey done by the TransUnion Cibil, a credit information firm, Indian credit card customers have improved their payment behavior with about 78% of them paying off monthly bills completely and about 92% of credit card holders often pay a greater amount than the minimum due. Thus, there is enough scope for a product like MoneyTap to thrive and scale.

MoneyTap’s app-based credit line provides a customer with a credit limit, anywhere from INR 25,000 to INR 5 lakhs, without any collateral. The value of the credit limit depends on the individual’s profile and the credit policy being used. With a patent-pending chat interface, the free app rapidly evaluates the user’s credit eligibility in just a few minutes and instantly informs them of the decision, along with the amount they are eligible for. Using the MoneyTap app, consumers can choose to borrow as little as INR 3000 or as much as INR 5 lakhs, or up to their upper credit limit. They also get to decide their own EMI plans with payback periods ranging from 2 months to 3 years. Interest is paid only on the amount borrowed and rates can be as low as 1.25% per month. If the user does not borrow any amount, then no interest needs to be paid. The credit limit also gets topped up once EMIs are paid back.

MoneyTap along with RBL Bank is able to provide its customers, instant decisions and instant access to money, 24/7, irrespective of holidays. Moreover, as per RBI guidelines, all financial transactions such as billing, repayment or withdrawals are directly dealt with the bank but through the MoneyTap App using secure APIs, thus ensuring 100% secure transactions. Consumers do not have to hold a bank account or any other account with the partner bank to avail MoneyTap. As an added convenience for shopping needs, a MoneyTap RBL Credit Cardis also provided to the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

It gives us immense pleasure to be able to spread our services across cities, various earning groups and people of different professions. We are glad that the credit line app has been appreciated and adopted vastly. We aim to expand further by opening MoneyTap for newer segments that are currently underserved and in need of credit. We have a vision of making credit accessible to 1 Million Indians in the next few years. Hence, this expansion is part of that vision. We believe we have a product that works well for the mass market – flexible, affordable credit available in a convenient way.

Harjeet Toor, Business Head – Microbanking, Credit Cards, Retail & MSME Lending, RBL Bank said

India is a largely informal and an unorganised economy with about 90 per cent of people employed in the informal sector. A majority of these are self-employed. The government’s recent initiatives, such as Startup India and Skill India, are aimed at promoting financing, encouraging entrepreneurship and generating employment among the micro, small and medium enterprises. The MoneyTap app will give the self-employed quick and easy access to a credit line they can use both for their personal as well as professional needs.

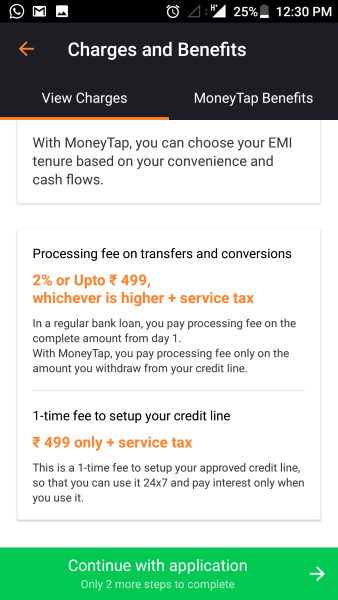

The MoneyTap app is available on Android Playstore to all salaried employees and now self- employed. Qualified customers, after completing the KYC [right from the app with no paperwork involved], will pay a one-time Line setup fee of INR 499 + tax in their first month e-settlement. There are no hidden fees or charges and every time the customer chooses to take an EMI, they will be shown the interest & any other applicable charges and the customer will be required to provide explicit consent before borrowing.

About MoneyTap

MoneyTap is a Bengaluru-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and $300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 [now Prime Venture Partners] where he helped create companies like ZipDial [sold to Twitter], EZETap, Happay, etc. Kunal [ex Texas Instruments] & Anuj [ex Airtel & JWT] co-founded Tapstart that grew to 300K users and turned profitable in 2 years. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap

Few weeks back, we reviewed MoneyTap which is India’s first app based credit line. You can find the MoneyTap review here. As mentioned in the review, MoneyTap offers unsecured loans for salaried professionals in association with its partner banks.

Unlike P2P lending companies, the interest rate is much lesser and the loan process is fast & simple 🙂 Today we have a chat with Bala Parthasarathy, Co-founder & CEO of MoneyTap about MoneyTap, the P2P lending market, opportunities in Fintech, impact of Digital India & much more. So let’s get started with the Q&A….

How did you come up with the idea of MoneyTap ?

It was a combination of personal experiences as well as general observation. Growing up in India in the 80’s & 90’s and coming from middle-income group families, we have all faced shortage of additional funds at some point. We observed the market need and realised that the middle income group [the salaried class] has always been facing challenges with respect to credits, especially small amounts. People are not comfortable going to banks for loans for minimal amounts-this could be anywhere from Rs. 3000 to Rs.50,000 to 1 or 2 Lakhs.

Asking for money from family and friends always has an embarrassment factor. The needs are what most of us have, that could be anything from medical, birth, death, school fees, deposit to take a rent on house, etc. In many cases, people even have fixed deposits that they just don’t want to break for a small need. This is where we thought of MoneyTap and wanted to be like a friend who could be reached out at fingertips.

At MoneyTap, we are on a mission to change this and make credit accessible to those who deserve it. The ubiquitous presence of smartphones and initiatives such as Aadhaar has made it possible for us to develop a truly powerful and disruptive financial instrument. The credit line for consumers with accessibility through an app is a new concept in India and we are excited about the opportunities it can bring to thousands of millions of Indians. MoneyTap is like a friend who gives you money when in need, be it marriage, birth sudden death in family, school fees, hospital bills or sudden cash crunch during the month end. We, at MoneyTap, want to make credit available for deserving and eligible candidates.

Can you share some details about the team behind MoneyTap ?

MoneyTap is based in Bengaluru and all the three of us have been entrepreneurs before with an IIT/ISB background. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and USD 300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 [now Prime Venture Partners] where he helped create companies like ZipDial [sold to Twitter], EZETap, Happay, etc.

Kunal [ex Texas Instruments] & Anuj [ex Airtel & JWT] co-founded Tapstart that grew to 300K users and turned profitable in 2 years. They exited this venture in 2015.

What is the TAM of the consumer debt market that MoneyTap is trying to address ?

Consumer debt is growing fast in India. According to the last available consolidated data from the Reserve Bank of India [RBI], personal loans – extended by banks grew at 28.7% in 2015 and credit cards grew at 23.6%. But if we look at the actual numbers, there are just 24 million credit cards for a country of 1.2 billion! Middle income customers making Rs. 25,000 per month or more, facing frequent cash crunch for regular needs like education, medical, birth/death, etc. are not serviced by financial institutions today without putting up collateral such as gold.

Large needs, such as buying a vehicle, house, etc. are addressed by financial institutions unlike online and offline shopping. Though the latter often involves very high credit card interest rates of 40% if one doesn’t pay on time. This is the clear unaddressed need.

How different is lending based on Line Of Credit vis-a-vis P2P Lending or taking a loan [any type of loan, personal/housing/education,etc.]

We see the following major differences

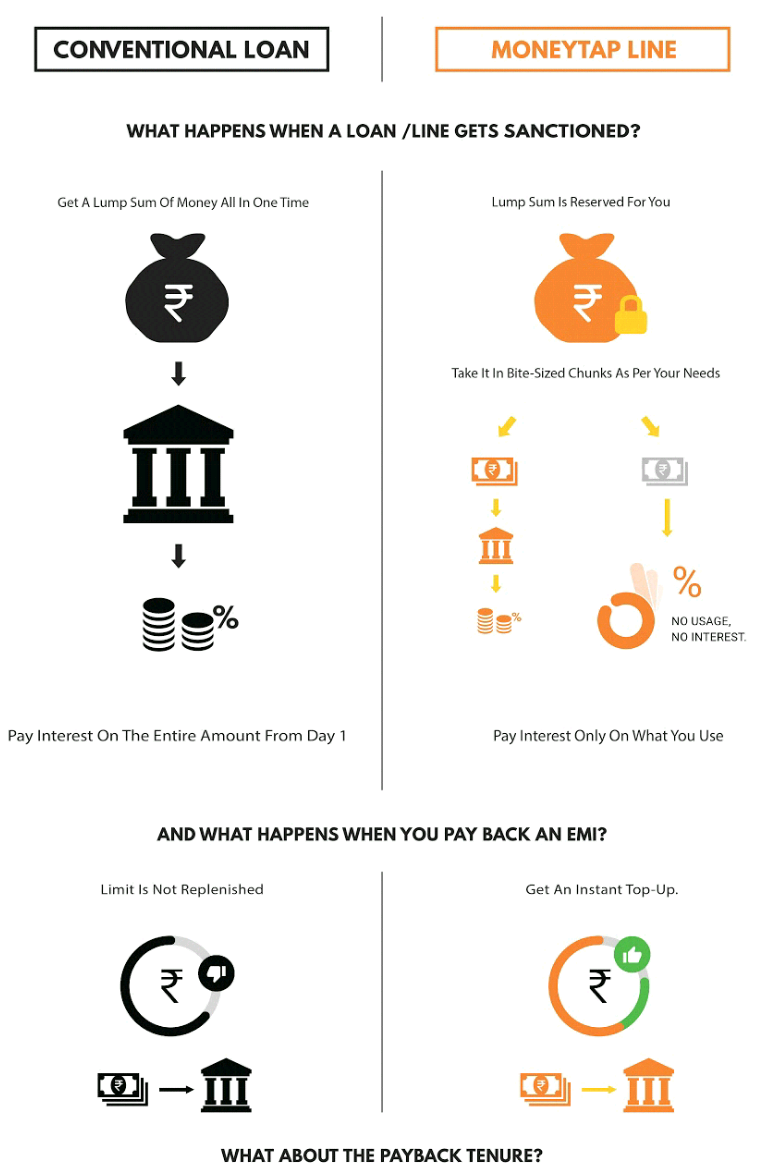

1. Once a credit line is sanctioned with an upper limit, one can decide any amount of money from that limit and choose to withdraw only that specific sum from the credit line. So, if there’s an approved credit line of say Rs. 3 Lakh, one could withdraw a small amount like Rs. 5,000 or Rs. 50,000 and so on.

In contrast, a typical personal loan would force one to take the entire Rs. 3 Lakh in one shot, even though the need for money is spread over a period of time.

2. Interest would be charged only on the small amounts borrowed and not on the full Rs. 3 Lakh. Thus, if amounts of Rs. 5,000 and Rs. 50,000 are borrowed separately, then one would only have to pay interest on the total of Rs. 55,000 and not on the entire amount of Rs. 3 Lakh sum. This would have made a world of difference to a person’s monthly cash flows and overall financial condition.

The obvious contrast with a typical loan is that interest would be charged on the full Rs. 3 Lakh amount from day one. Usually a person has no choice in this scenario.

3. In most cases, the flexible borrowing options in a credit line come with the convenience of deciding payback periods for the separately borrowed amounts. Thus, for an amount of Rs. 5,000 borrowed from the credit line, one could choose to repay in 2 months and pick a longer tenure for the amount of Rs. 50,000, say anywhere between 12 months.

In contrast, a personal loan tenure would be fixed upfront with little or no flexibility in most cases. The advantage of a credit line is that as soon as EMIs are paid back, the credit line gets replenished automatically and one can continue the cycle of borrowing and repayments without needing to apply gain.

The infographic also explains how a credit line differs from a conventional loan:

What are some of the data points that MoneyTap uses in order to check whether an individual is creditworthy to be approved as a borrower on MoneyTap ?

Firstly, an individual needs to qualify the MoneyTap eligibility criteria mentioned below:

23 years and above age

Salaried individuals with minimum salary of 20,000 pm.

Credible KYC documents

Residents of Delhi, NCR, Mumbai, Bangalore, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara and Bharuch [will be launching in other cities soon]

Secondly, our partner bank check the creditworthiness of the applicant based on their credit history and thereby the applicant is approved/ disapproved basis all the steps. Once approved, their credit limit is set according to their credit history.

Few years back, there was huge wave about MFI’s (like SKS Microfinance), in 2016~17 the wave is around fin-tech sector (NBFC’s), what are your thoughts about the Fintech space in the coming years ?

Fintech will see significant growth and innovation in the next few years. Innovations like IndiaStack and deregulation in the form of GSTN, payment bank licenses and demonetisation along with a massive governmental push to move payments to digital will spur a significant growth in multiple areas in finance.

[L to R] MoneyTap founders – Kunal Verma, Anuj Kacker and Bala Parthasarathy

There is a general question with borrower, what happens if they are unable to pay an EMI on time/not able to return the money. How is the lingering question of Credit Risk taken care of ?

The same consequences of not paying one’s credit card bill or bank loans apply in this case as well. The Reserve Bank of India has nominated 4 credit agencies [e.g. CIBIL] that track an individual’s financial credit scores. If one does not repay or delay the repayment, our partner bank will automatically report it to these agencies, which will record the information. This can lower the borrower’s credit score.

Once an individual’s credit score is affected, they will not only lose MoneyTap access, but all future loan applications will be negatively impacted. He might not be able to get loans easily to buy a house, a car or a two-wheeler or get a credit-card, as all the lending institutions in the country check with these agencies before approving any loan. The bank might also initiate legal recourse to recover the money from the individual.

Can you please share some insights into the min/max loan that a person can avail on MoneyTap, interest rates, pre-closure charges, association with RBL Bank and any other details that would come in the mind of a personal availing a short-term credit

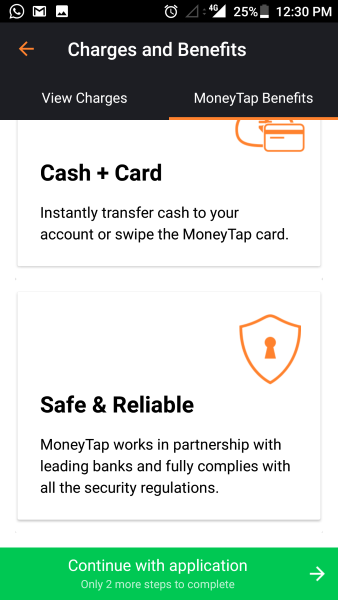

MoneyTap enables consumers to get instant credit from partner banks at the tap of a button on the app. Credit Line, a facility that was only available for businesses until now, is now being made available to consumers. The ‘Credit Line’ means that the bank will issue a limit of up to INR 5 lakhs, without any collateral or charging any interest. Against this limit, using the MoneyTap app, consumers can borrow as little as Rs. 3000 or as much as Rs. 5 lakhs and repay it as EMIs from 2 months to 3 years. The interest is paid only on the amount borrowed and the rates can be as low as 1.25% per month. The limit also gets automatically replenished as soon EMIs are paid back.

Any salaried employee can download this free Android app and in a few minutes, using a patent-pending Chatbot interface, provide all the information typically required by banks. The app securely connects with the banking systems to give them not only an instant approval but also a credit limit, depending on individual credit history.

The RBL Bank is the launch bank partner of MoneyTap. RBL’s technology enables MoneyTap to provide instant decision and instant access to money, 24/7, irrespective of holidays. Though all actions are initiated on the MoneyTap app, per RBI guidelines, all financial transactions such as billing, repayment or withdrawals will directly be with the bank using secure APIs.

As an added convenience for shopping needs, a ‘MoneyTap RBL Credit Card‘ is also provided for the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

According to your data, which is the biggest category where customers have opted for loan based on Line of Credit/MoneyTap ?

Our Top-3 categories are Wedding spends, Household related purchases and Education.

Currently MoneyTap is available only for working professionals, any time-line or plan on when you plan to open up this avenue for entrepreneurs, SMB’s, freelancers, etc.

As of now our only target is to expand our customer base among the salaried class. We have lowered the minimum salary limit for eligibility from Rs. 25,000 per month to Rs. 20,000 per month. MoneyTap now is also available for people staying in shared accommodations.

Normally Banks & other financial institutions take couple of days~weeks for KYC, how does technology [behind MoneyTap] ensure that the entire process of validation of credit-worthiness of an individual is expedited ?

The first step in our evaluation process is to understand the person’s credit profile. We are able to do this under 7-minutes on the MoneyTap app that you can download for free from the PlayStore. After that, qualified applicants who have their Aadhaar card and updated mobile number with Aadhaar, can eSign their documents so that absolutely no paperwork is required.

We are able to do this because of our advanced technology as well as the increasing adoption of Aadhaar and IndiaStack.

MoneyTap is currently present in how many cities in India ?

MoneyTap is currently present in Bangalore, Delhi, NCR, Mumbai, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara, Gandhinagar, Anand and Bharuch.

Are there are any RBI guidelines regulating the app based businesses [based on Line Of Credit] in India or to put it the other way round, is there a requirement to regulate lending based on Line Of Credit in India ?

Lending, whether they’re on an app, website or physical branches is regulated in the exact same way. There must be a bank or NBFC that meets all of RBI criteria. MoneyTap also meets with RBI from time to time to provide inputs so that the regulators can draft appropriate policies.

What are some of the things that a borrower needs to keep in mind while opting for repeated loans on MoneyTap [or for that matter any medium offering loan based on Line Of Credit] ?

Whether it is MoneyTap or not, basic rules of finance that we learnt from our parents and grandparents apply. Borrowing money to tide over medical emergencies or invest in things like education are good. Buying and spending things beyond the ability to pay it back will always have a bad ending.

In case of Loans, interest rates vary from Bank to Bank and are also dependent on external factors like market volatility, etc. can you let us know whether the interest rates are fixed on MoneyTap or whether it is like a normal loan [where for certain number of years interest rate is fixed and later it is variable] ?

A borrower has to pay interest only on the funds he uses. At the time of withdrawal, he can choose the terms of repayment, which can be anywhere between 2 months and 3 years. The repayment tenure he chooses will determine the EMIs.

The interest rate is equivalent to market rates for any ‘personal loan’ with zero collateral or security. It can be as low as 1.25% per month depending on the partner bank and the credit profile of the user.

Who are some of the competitors of MoneyTap ?

MoneyTap is the first credit line app in India. Until now the concept of credit line was present for traders through money lenders. We have introduced the concept for consumers for the first time. There is no competition that we see at present.

2016 was a tough year for startups [especially from funding point of view], how according to you should entrepreneurs deal with such adverse situations ?

Grin and bear it. Markets are always cyclical and the sky high valuations backed by even higher expectations were bound to come back to earth sooner or later. This is actually a great time to get excellent talent who are not overpaid and build great businesses.

Can you share some tips for building an effective team for startups [especially the initial core team].

There are three big rules:

Hire very, very smart people. You can’t substitute intellectual horsepower with anything else. And give them a lot of autonomy.

Smart people are rarely easy to work with. The ‘brains-premium’ is worth paying, up to a point.

If and when they get disruptive or if you made a mistake in hiring, quickly let them go. It’s better for both parties in the long term.

How important is it for early stage startups to pivot their business model [in case things are not working out as per their plan] or when is the right time to pivot ?

It is critical. But the problem with Indian entrepreneurs is not in recognizing the importance of pivoting. It is the execution of a pivot. They typically just add on the new business and keep the old one. That’s a ‘khichadi’ strategy, not a pivot strategy.

After demonetisation, there has been a huge demand for payment apps [including UPI], do you see that trend working in favour of apps like MoneyTap [that offer different services compared to e-wallet apps].

Absolutely. We are not a merchant or consumer UPI app like others. We are in the business of providing credit. UPI is a terrific way for our customers to take money out and pay back without the hassle of net-banking, etc.

Bala’s earlier venture Snapfish was acquired by HP, what according to you should entrepreneurs look for when there is interest [from other companies] for their startup getting acquired [and not acqui-hired].

Again, there are three rules for selling your company:

Good companies are bought, not sold. In other words, if you are actively out there selling your company, you will have to settle for peanuts.

You should always have multiple parties engaged, not just have one buyer.

Sell on a high note-when the company is doing great, potential buyers will extrapolate to value your company at an even more glorious future.

As per your entrepreneurial experience, when should an entrepreneur look out for external funding ?

When they really don’t need the money. It’s always the best time!

Some books that you highly recommend for entrepreneurs

There are lots of good books. The two I recommend are, ‘Zero to One’ by Peter Thiel and ‘Hard things about Hard Things’ by Ben Horowitz.

Some closing thoughts for our readers!

Entrepreneurship is not easy and not for everyone. But it is addictive and some of the most creative moments in your life will be during this journey. And there is no other [legal] way to have a huge financial windfall besides running your own company.

We thank Mr Bala for his time and sharing valuable insights with our readers! If you have any questions for Bala about MoneyTap, Fintech, scaling up, etc., please email them to himanshu.sheth@gmail.com or leave your question in the comments section.

How many of us have landed in a cash-crunch situation where you wanted a certain amount of cash as a short-term loan but felt awkward to borrow from your friends/relatives or they refused to lend due to some unimaginable reasons! With growing disposable income, rising expenses, etc., such scenarios are very common, especially with the urban population. You might require a loan for paying your rental deposit, starting a business, shopping, going on a vacation, buying home appliances or simply because you have run out of cash towards the month end.

Image Source – MoneyControl

Opting for a bank loan or securing an unsecured personal loan [from P2P companies] might not be feasible due to the higher interest rate. What if there existed a solution where borrowers can opt for loans based on their Line Of Credit.

Line of Credit and its advantages

A line of credit, abbreviated as LOC, is an arrangement between a financial institution, usually a bank, and a customer that establishes a maximum loan balance that the lender permits the borrower to access or maintain.

The main advantage of a line of credit is its built-in flexibility. Borrowers can request a certain amount, but they do not have to use it all. Rather, borrowers can tailor what they spend to their needs, and they only have to pay interest on the amount they spend, not on the entire credit line. In addition, consumers can also adjust their repayment amounts as needed, based on their budget or cash flow. For example, borrowers can repay the entire outstanding balance at once, or they can opt to just make the minimum monthly payments [Source].

Loan based on Line of Credit : A market opportunity

As mentioned earlier, young Indian urban population is and will continue to be driven by aspirational living and the basic standard of living will increase drastically. On similar lines, Indian consumers are also extremely credit-starved; they are either denied or pay a heavy premium for accessing the financial services due to sparse data, high transaction costs and poor trust infrastructure.

Many salaried urban Indians can easily co-relate to the situation shown in the video below

Unsecured personal loans offered by banks is still relatively slow-growing credit product that stands at around Rs. 45,000 crores. The informal market that includes moneylenders and family is roughly estimated to be around 50~100 times bigger. Some of the primary reasons for the gap are below:

Lack of reliable credit information available for banks to be able to offer credit

Credit cards, even when available only solve the ‘Shopping’ problem. Day-to-day needs like paying school fees, emergency expenses, rental deposits, etc. are largely cash-based

Applying for an unsecured personal loan is time-consuming for the consumer and expensive for the banks to process. Banks then prefer giving higher ticket loans to fewer people.

There clearly existed a market opportunity if a Bank/NBFC could provide an efficient solution to provide personal loans to Indian consumers based on their line of credit and solve the existing credit problem for Indian middle-income group. This is the opportunity that led way to the founding of MoneyTap, a Bengaluru-based fintech startup that has stellar serial entrepreneurs-Bala Parthasarathy, Anuj Kacker, and Kunal Varma as it’s founders. MoneyTap is India’s first startup that provides loans based on consumer’s credit line. A couple of months back, the MoneyTap app crossed 100K installs in three months since launch.

Today, we review the MoneyTap Android app from the perspective of usability, ease of securing a loan, communications with the customer-support team, etc.

MoneyTap : Money on your tap

MoneyTap is India’s first App-based credit line. Currently, it is open only to salaried professionals and loan is given to the consumers in partnership with banks. Unlike loan process which is very tedious, MoneyTap makes the entire process painless since it all happens on the app including the verification of eligibility, eKYC, etc.

The app is built on patent-pending technology, it is very secure and uses AI, NLP, ChatBot, etc. for providing a better experience to its customers! Some of the salient features of MoneyTap are below:

Credit Limit – Minimum credit limit of Rs. 3000, maximum credit limit of Rs. 5 Lakhs.

No Usage, no interest – Interest is charged only on transfer or EMI conversion. The remaining limit is available to the customer at no additional cost.

Low Interest – Interest rates vary from 1.25%~1.5% per month with no hidden charges.

Decide your own EMI – Customers can choose the tenure from 2 months to 36 months

Rewards & Benefits – MoneyTap credit card is loaded with rewards and other benefits

No collateral, no guarantors, 100% unsecured

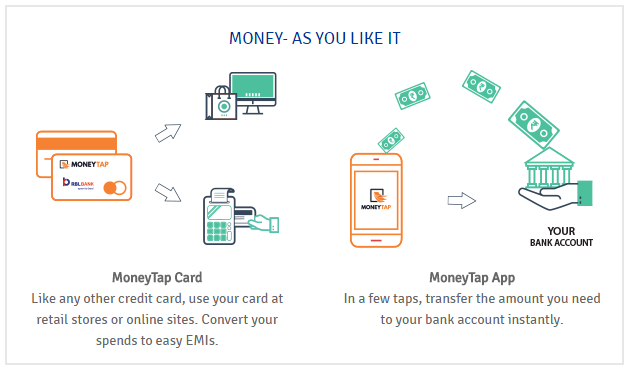

Swipe, Tap and Convert – Customers can shop online or swipe at a store, one tap to transfer money instantly to the bank.

Keeping track of the transactions – EMIs and available credit can be tracked right from the app. It combines the best of personal loan, cash, and credit card, all under control through the mobile app!

There is a one-time setup fee of Rs. 499 plus taxes and the customer would get a MasterCard powered credit card by RBL Bank. The lingering question that comes to mind is ‘Why should someone pay for a credit card in times when other banks are offering credit cards for free‘. I checked with the RBL bank executive as well as customer happiness team at MoneyTap and they informed that customer would receive equivalent credit points that can be redeemed across retail outlets or on e-commerce platforms [so ideally the credit card is free].

As mentioned earlier, any salaried employee [with a monthly salary above Rs. 20000] can avail loan via MoneyTap. The immediate question that comes to mind is “Why only salaried professionals?”.

We had posted this same question to Bala Parthasarathy, CEO of MoneyTap and the answer lies in ‘Probability of guaranteed repayment’. He also informed us that since ‘Unsecured loan based on credit line’ is a relatively new concept in India hence, partner banks, as well as MoneyTap want to ensure that they create a market ‘one customer segment at a time’. Bala Parthasarathy did inform us that soon entrepreneurs, freelancers, designers, etc. could avail loans via MoneyTap but for the time being their target market segment is salaried professionals.

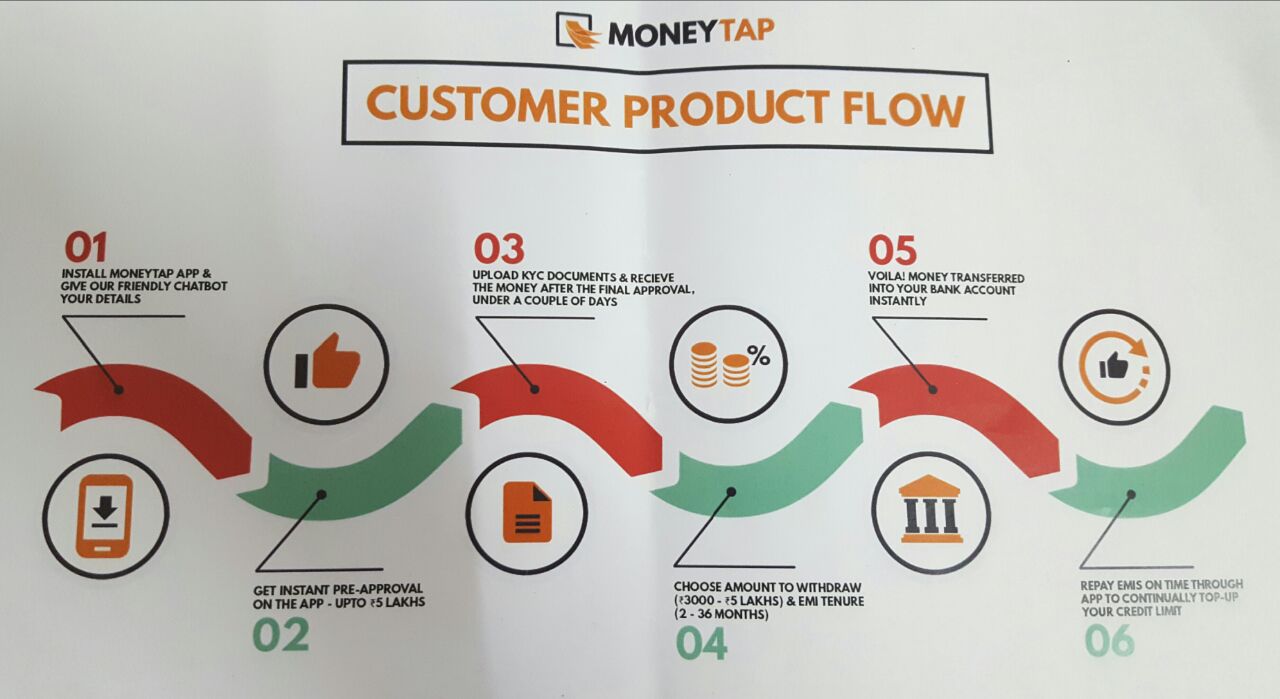

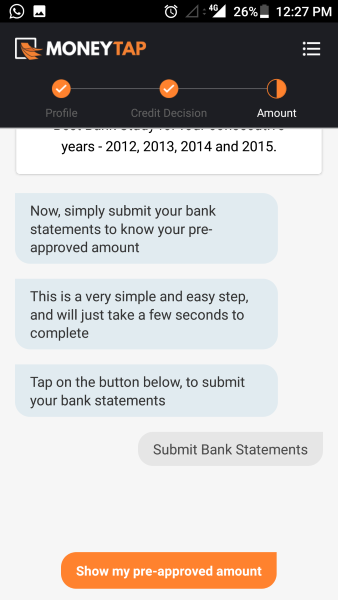

Once the user downloads the MoneyTap app from the Play Store, (s)he needs to upload a selfie for the application form, PAN card photo and current residence proof for eKYC. The MoneyTap app has three main sections:

Profile creation

Credit decision

Loan Amount

Profile Creation

The app is built on a patent-pending chat bot interface and would ask for all the relevant information that is required by banks. However, unlike traditional loans from banks where you need to fill a lot of information & submit tons of documents, with MoneyTap the process looks fast & breezy. You need to also enter the purpose for which you require a loan [further studies, business, house deposit, pay existing loan, etc.].

If you have an Aadhar Card, things become much easier since you could simply scan the Aadhar card bar-code and all the relevant information would be fetched from the card. Bala Parthasarathy’s learnings during his tenure with UIDAI would have come in handy during the development of MoneyTap!

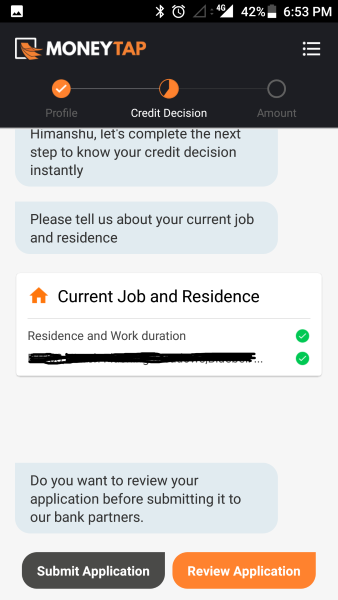

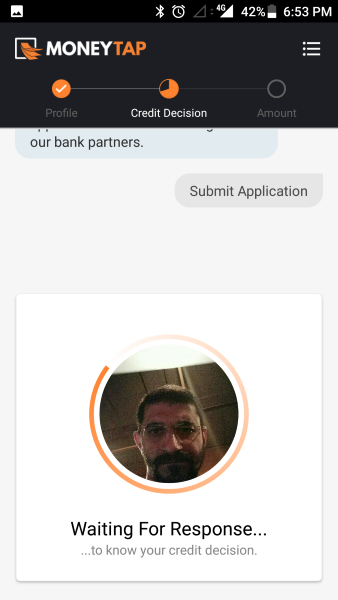

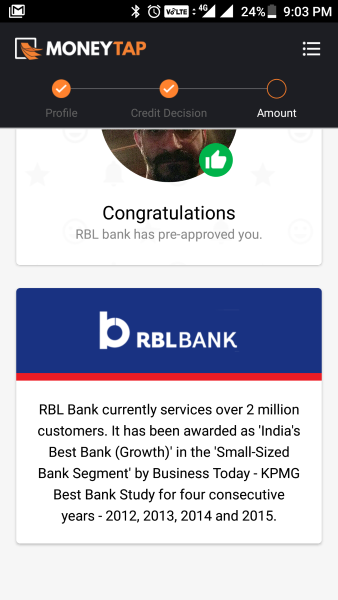

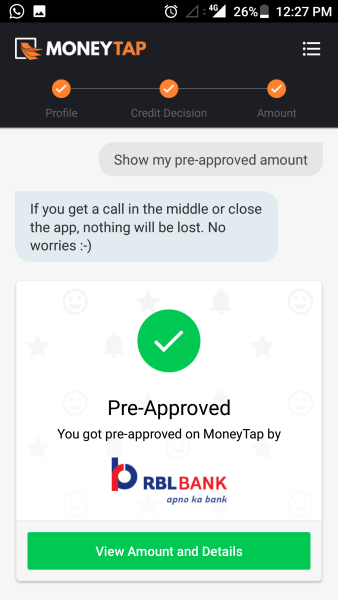

Credit Decision

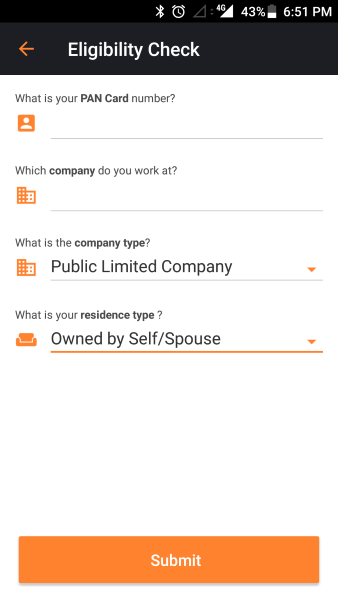

Once the eKYC is done than the app takes the user to the next step where important decisions are taken and the customer would come to know about the eligibility for the loan [as well as sanctioned amount]. You need to enter your PAN details, current organization & residence type. Once these details are submitted, the patent-pending algorithms fetch your Credit [CIBIL] score, social score, etc. in order to perform ‘Eligibility Check’.

For some reason, if you fail to pass the eligibility criteria e.g. here, here you need not proceed to the next step. Similar to traditional bank loans, CIBIL score might be the first data point used by MoneyTap for checking eligibility for a loan.

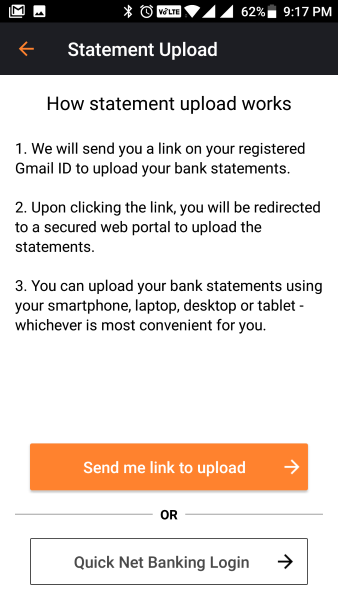

Once the first step of eligibility check has passed, the user/loan applicant would need to submit last six months bank statements [salary account preferred]. The user has the option to either ‘Login to net-banking account’ inside the context of MoneyTap or upload bank statements via secure upload link provided by MoneyTap. Immediately, a lingering question about security would come to your mind since you are uploading your bank statement but as stated in the T&C of MoneyTap, their team takes security very seriously and all the back-end APIs comply with mandated security standards and robust protocols.

Security & Protection of Privacy

Protection of your privacy and your data security is our primary concern. Our back end APIs comply with mandated security standards and robust protocols. Our security measures have been tested and certified by our partner bank’s IT team. Your credentials are only used to retrieve your bank statements for verification. Alternatively, you can also upload a PDF of your bank statements which is eco-friendly and time-saving [Source]

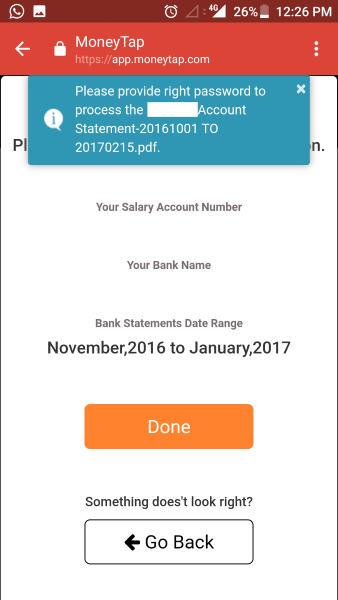

MoneyTap has tied-up with a 3rd party company through which ‘Net Banking Login’ as well ‘Secure Bank statement upload’ is made possible. In order to test the security of the app, I downloaded my bank statement and uploaded the pdf after removing the password and the MoneyTap app rejected the bank statement since there was an author signature mismatch. When I dropped an email for the rejection, the MoneyTap customer success team member called me and clarified the reason for rejection.

Once I uploaded the proper bank statement, the application got approved after a couple of days. In this entire process, there was no interaction with the bank partner and entire process took place on app & email.

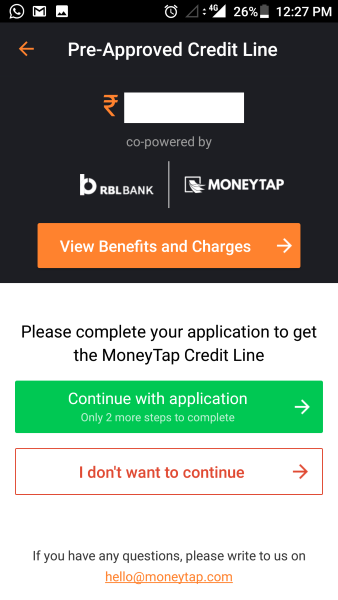

Loan Amount

Once the important steps of eKYC and Credit Decision are complete, the final step is disbursal of approved loan amount. As mentioned earlier, interest is only charged on the amount borrowed with interest rates as low as 1.25~1.5% per month. The customer would also receive a Credit Card from RBL Bank and this is the only step where you have to interact with the bank executive.

During the interaction that I had with the executive, he called me from his mobile phone & asked me to send bank statement over WhatsApp which is against security norms of the bank. Since MoneyTap acts as an ‘Unsecured loan enabler’, it becomes important for their customer success team to ensure that the bank officials adhere to all the necessary standards since as a customer you are dealing with MoneyTap with RBL Bank being a black-box. The official did call me from bank’s landline after which communication was smooth.

Even though the technology behind MoneyTap app is awesome and the entire approval process was completed with a blink of an eye, efficient communication with bank partners holds the key else it could result in negative reviews More details about the RBL MoneyTap credit card can be found here

Currently, MoneyTap is available in Bengaluru, Delhi NCR [Delhi, New Delhi, Noida, Greater Noida, Ghaziabad, Faridabad, Gurgaon], Hyderabad and Mumbai [Mumbai, Navi Mumbai, Thane] and Chennai. However, there are requests from users from other cities and in order to track the incoming requests, MoneyTap could add a Notify Me page where the user enters his/her city information which can act as important data for their team to identify next logical expansion [coupled with data from their partner banks].

As mentioned earlier, detailed communication about the application status [from MoneyTap Team] could be very important for creating a WoW factor. Though my application was processed in a couple of days, sometimes the partner banks might take more time in processing the application which might act as a spoil-sport. Hence, timely communication becomes a very important factor!

MoneyTap:Conclusion

The overall experience of using the MoneyTap was great. The technology behind MoneyTap makes the entire loan application process less cumbersome. Banks and financial institutions are bullish on chatbots and MoneyTap uses chatbot technology very effectively. Though P2P lending, loans on credit line and other mechanisms of obtaining unsecured loans are still in nascent stage, MoneyTap does have a first-mover advantage since it is India’s first app-based credit line and provides loans at lesser interest rates!

If you have used the MoneyTap app, please leave your feedback/reviews in the comments section…

MoneyTap, India’s first App-Based Credit Line, has been awarded as the leading FinTech company, in the lending category, at PICUP Fintech 2017. PICUP Fintech is an event by FICCI to recognize the best innovations from Fintech companies in diverse areas like Wealthtech, Lending, Payments, Artificial Intelligence and Robotics. The event witnessed diverse groups of FinTech players, leading bankers, technology experts and policy makers. The event was organized by a joint effort of NASSCOM, FICCI, IBA and BCG in Mumbai.

Six companies from each category were shortlisted after applying for a product demonstration. MoneyTap, Faircent, Cropin SmartRisk, GraduFund, FlexiLoans, FinTechLabs were the six shortlisted companies in the Lending category. These companies presented their latest innovations and overall business to the audience and industry jury members comprising of Sunny KP-General Manager, Federal Bank, Jayant Kshirsagar-Director (Marketing), SAP and Ashish Garg-Partner, BCG. MoneyTap was the top company to be selected by the jury members’ basis the presentation and product demo.

We feel honored to be recognised as the leading FinTech company at PICUP Fintech 2017. It gives us immense pleasure to be recognised by the top officials of the industry. This recognition gives a boost to our motto of providing a convenient credit line to the middle income group of our country and making the availability of money easier and faster.

MoneyTap introduced the concept of a Credit Line [personal line of credit for consumers] for the first time in India when it launched in September 2016. The ‘Credit Line’ means that the bank will issue a limit of up to INR 5 lakhs, without any collateral or charging any interest. Against this limit, using the MoneyTap app, consumers can borrow as little as Rs. 3000 or as much as Rs. 5 lakhs and repay it as EMIs from 2 months to 3 years.

The MoneyTap app is available on Android Playstore to all salaried employees, living in Ahmedabad, Vadodara, Delhi NCR, Mumbai, Bengaluru, Pune, Hyderabad and Chennai. The company is continuously expanding across India.

About MoneyTap

MoneyTap is a Bangalore-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and USD 300M in revenue. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap