Visa, the global leader in payments technology and BillDesk, India’s leading electronic payments company, announced successful enablement of fifty large service providers for BharatQR payments acceptance in a short span of a month, thus extending the digital payment facility to potentially over 300 million consumers.

Some key merchants enabled include Tata AIG, ACT Broadband, Reliance Energy, Gujarat Gas, MTNL, Aircel, Tata Power, Pune Municipal Corporation, and Calcutta Electricity Supply spanning services such as utilities, internet, phone, DTH, insurance, and government services.

T.R. Ramachandran, Group Country Manager, India and South Asia, Visa, said

The core idea that binds technology and payments is simplicity and convenience, and QR code is a great example. Having pioneered QR technology as low cost payments solution for open loop networks, and having worked with the government and the industry in developing BharatQR, Visa’s endeavour is to grow the acceptance network for BharatQR in the country and make digital payments accessible to all. Through our collaboration with BillDesk, we hope to fast-track the transition to digital payments and make less-cash society a reality for India.

BillDesk is delighted to engage with Visa to promote BharatQR. This is a simple yet powerful solution with great potential to shift consumers and merchants from cash to digital payments for everyday spends. It provides the speed, security and convenience that cash payments cannot match. Merchant interest in and demand for BharatQR is growing for it is simpler, faster, and more reliable ways to accept digital payments with BharatQR. We will continue to collaborate with Visa to enable online merchants for BharatQR acceptance and simplify digital payments for consumers.

Bharat QR is a secure, network-agnostic, and device less interface that enables customers to make payments using their bank apps on smartphones. BharatQR simplifies digital payments by eliminating the need for divulging card details at the point of sale. For example, to use Bharat QR to pay their electricity bills, customers will simply need to log in to their bank’s app, and scan the QR code displayed on their electricity bill, enabling instant payment. Alternately, customers may enter their unique Customer IDs online and generate a QR code that can be scanned using their bank app. To date, 30 banks together serving over 90% of India’s population have enabled their banking apps and nearly 400,000 merchants for BharatQR payments.

India will lead the world in smartphone adoption with a net addition of 350 million connections in 2016~20, according to a GSMA report. With the common standards, coupled with the low-cost acceptance method, BharatQR has the potential to accelerate financial inclusion in India.

PayPal, the global leader in online payments have announced a shortlist of five new Financial Technology [FinTech] startups – Finbox, Neoeyed, Paymatrix, Scalend and Tybo as new entrants into its PayPal Incubator in Chennai.

The announcement was made after the final round of pitching during the 5th Incubation Challenge, where 10 shortlisted startups from 250 startups presented to an esteemed panel of judges including Guru Bhat, GM Technology & Head of Engineering – PayPal, Anupam Pahuja, MD – PayPal India and Rama Bethmangalkar, Venture Capitalist, formerly with Ventureast.

As a part of PayPal’s vision to transform and democratize financial services, the Incubator helps elevate and drive innovation across the FinTech industry with a focus on startups in financial technology as well as adjacencies like loyalty, machine learning, big data and logistics among others.

Guru Bhat, GM Technology & Head of Engineering – PayPal said

In its 5th year, the PayPal Incubator has received an overwhelming response with over 250 applications from early stage FinTech startups – a 150% growth from last year, reflecting both the need for an incubation program, as well as the FinTech industry’s potential. Our program is designed to help our newly incubated startups script their own success stories by facilitating access to PayPal’s expertise in cutting-edge technology and by enabling them to leverage PayPal’s market leadership around the world.

Launched in 2013 in partnership with The Indus Entrepreneurs [TiE], the incubator provides a conducive environment for early-stage startups to grow and evolve at PayPal’s Technology Center in Chennai. The program offers startups technology counsel and mentorship, infrastructure support and networking opportunities with both investors and customers. In addition to these, PayPal will also be picking up an undisclosed stake in each of the selected startups this year.

Shortlisted Startups

Finboxis a digital lending software as a service which enables lenders to digitize their user journey and underwrite using alternate data. FinBox’s platform combines multiple APIs to build various digital lending experiences across use cases. FinBox API’s enable lenders validate Identity, underwrite using data from traditional and non traditional sources and cross sell financial products to their customers. FinBox products integrate seamlessly with the lender’s mobile and web properties and also with the loan management system backend.

Neoeyed helps the businesses to generate more revenues and improve users’ security by simplifying the login and registration processes on mobile applications. Using mobile devices, Neoeyed can recognize users by collecting information about human behavior that allows them to login without effort, nothing to type, nothing to remember, nothing to do…Transparent, simple, secure

Paymatrix is an analytics-driven property rental management platform that streamlines rent payments and collections for tenants, landlords and property managers. The platform’s dashboard provides solutions for end-to-end rent management including tenant screening, credit facilitation for rent deposits, rent documentation, rent automation, renters and landlords insurance and also helps in better interaction between tenants and landlords.

Scalend offers a ready to use AI enabled customer insights platform for financial services companies. The platform combines proprietary AI models with Big Data – Hadoop’s unlimited storage and compute power to help BFSI & Fintech companies generate actionable insights around omni-channel customer journey, back-office optimization, in matter of weeks not months or years

Tybo is a cloud based omni-channel e-commerce platform designed for home based and small-sized businesses. It provides the merchant a single view of their evolving business across multiple sales channels. The platform is focused on easy set up, simplicity of use and customizable design to create a beautiful storefront. It also enables end-to-end integration with supplier system and saves time by importing products directly into their store with real-time inventory sync.

Bengaluru based Datasigns Technologies has raised USD 1.5 million Pre-Series A funding from SRI Capital, Beenext and Pravega. Datasigns Technologies, founded by Monish Anand, Rahul Sekar, Anand Barua and Tushar Patel, had earlier raised an undisclosed amount of angel funding from Sanjai Vohra [former MD of JP Morgan], V. Bunty Bohra [Managing Director and India CEO of Goldman Sachs] and Peeyush Misra [Ex- Partner and MD at Goldman Sachs].

SRI Capital’s portfolio includes Fab Hotels, Healthify and Yellow Dig among others, Beenext has invested in – Droom, Citrus pay, No Broker, Faasos and Pravega Ventures has invested in Crofarm – an agri-tech company, Innovaccer – big data platform for enterprises.

Datasigns Technologies is a mobile first lending platform, which lends via their android application called Shubh Loans. Shubh Loans is a vernacular language app which builds a proprietary credit score and report for loan applicants, thereby helping them understand their credit standing holistically.

Sashi Reddi, Founder & Managing Partner of SRI Capital said

Proud to back a rockstar team, led by Monish Anand, in the consumer lending space in India. Many massive companies are going to be built in this space, finally being able to lend to the next 200 million consumers—Shubh Loans will be one of them.

Shubh Loans score is dynamic and changes with applicant’s financial and non- financial behaviour. Using the Shubh Loans app, users can apply for a loan of up to 2 Lacs with maximum 2 years tenure. Datasigns has partnered with multiple banks and NBFCs, helping them in building their loans books.

Monish Anand, Founder & CEO of Shubh Loans stated

We are excited to have these great investors on board, at the same time we are even more determined to stay disciplined and execute our plan well.

Rahul Sekar, Co-Founder & Chief Data Scientist said

The lending business in the country is at an inflection point, our focus is on creative and responsible use of data to bring financial literacy and credit to people who deserve it the most.

Shubh Loans takes pride in its aim to democratise credit by making it available to all and believes that an unserved customer doesn’t make for an unservable one. Shubh Loans has set its sight on bringing over 10 lacs people into the formal banking system as part of its mission 2020.There are currently growing at 50% month on month and have tied up with over 9 lending institutions.

Fintech Valley in Vizag, a sustainable global Fintech ecosystem have announced the establishment of government sponsored Fintech Valley Accelerator at Visakhapatnam in collaboration with ICICI Bank and Mahindra Finance as corporate partners and Microsoft as the technology & acceleration partner.

Fintech Valley in Vizag created by APEITA [Government of Andhra Pradesh], is a self-sustainable global Fintech Ecosystem that focuses on converging finance and technology to create large avenues of growth through industry-enablers, world-class infrastructure, entrepreneurship and innovation.

ICICI Bank and Mahindra Finance have always leveraged technology to pioneer digital innovations and provide world-class banking experience to their customers. These institutions are focused on leveraging the current transformational trends in technology to bring value to their offerings. The first cohort of the accelerator program will have 10-12 startups working to develop solutions for ‘Financial Inclusion’, ‘Security and Fraud Prevention’ and ‘Customer and Risk analytics’ for a period of 12 weeks. This will be a resident program based out of Visakhapatnam and will provide selected Fintech startups an opportunity to catalyze their development through a combination of support, guidance and training.

The recruitment process for the accelerator has commenced, and the first cohort will start in first week of October. The program will conclude with a grand demo day in January 2018, in presence of corporates, mentors and investors from across the world. This is in continuation of the vision of the AP Government to bring ecosystem players together in the Fintech Valley and nurture a ‘fintectonic’ culture in the state that enables traditional models of business. The accelerator program aims to act as a catalyst in the growth of startups by connecting them to Fintech ecosystem players and develop the startup community in Visakhapatnam.

Mr. J A Chowdhary, Special Chief Secretary & IT Advisor to the Chief Minister – Govt. of AP said

The Andhra Pradesh Government and Fintech Valley Vizag is excited about the Fintech Valley Vizag is all set to converge finance and technology and create large avenues of growth. The accelerator program aims to act as a catalyst in the growth of startups by connecting them to the leading Fintech ecosystem players.

For application process and other details about the Program, please visit #FintechValleyVizag

Fintech is having a huge impact on the financial services in India. It has been largely dominated by the lending and payments companies in India. Initiatives like the India Stack [UPI, e-KYC, Aadhar] by National Payments Corporation Of India [NPCI] have been instrumental in leading the Fintech revolution.

Many of the fintech companies are leveraging Machine Learning, Artificial Intelligence, Social Data Intelligence, Blockchain, etc. in order to solve critical business problems. For example, with the help of AI, contextual data and transaction data, your wealth managers can come up with a ‘more relevant’ financial plan that suits your requirements.

When we talk about Money, the immediate thought that comes to our minds is ‘How to I multiply wealth via good investments‘. There are significant number of investment options available in the market but the option that you choose depends on factors like your age, dependencies, exisiting investment portfolio, risk apetite, etc. One good investment option is ‘Mutual Funds‘ but as per a report, India’s Assets under management [AUM] to GDP ratio is only 9 percent which is significantly lower as compared to other developed/developing countries. The bright side about this report is that there are rising number of people interested to invest in Mutual Funds given that they get proper hand-holding and guidance.

This is the problem that founders of WealthApp, a Fintech startup aim to solve by amalgamating their vast knowledge in personal finance with technologies like AI, Machine Learning, etc. Today we have a chat with Gaurav Dhawan, Co-founder & Director of WealthApp about WealthApp, Fintech, Personal Finance, etc.

We are ex-bankers from Citi who have decades of experience in personal financial management of individuals across net-worth segments. We understand that while people with higher net-worth have access to good quality financial advice, the middle-income groups in India experience an acute shortage of the same. There are various estimates to suggest that about 30 crore people in India have an ability to invest, a majority of which form the entire middle-income group of the pyramid. Given this huge need gap, we wanted to put in place a solution to reach sound financial advice to the market at large. The next question on our minds was to figure a solution to bridge this gap ? One thing that we realised very soon was that we needed to use technology to reach out to a larger audience.

However, using technology is one thing – but to marry that with quality advice is a totally different ball game. We then studied the entire advisor-client interaction cycle, right from the time of first interaction to the evolution of the relationship over a long term, and broke it down into steps that we could automate. We realised that most of this engagement can be automated using algorithms. Then we started picking elements of this interaction cycle to build algorithms to automate the process – that’s how WealthApp was born. We formally launched the platform in October 2016 for public at large.

Can you please give a background about the team behind WealthApp ?

The founders consist of myself, Subba Rao Telidevara, Sanjay HB and Mitesh Shah. We have a cumulative experience of 50+ years across various forms of money management. This makes us aware that the long winding process, paper work and lack of proper guidance in investment methods puts off people as prospective investors. The team is hard at work to ensure that our platform at WealthApp overcomes all of these barriers and adds value across the personal financial life of our customers.

As per a report, there is very small percentage of investors/would be investors who plan to invest in the Equity market [or MF], how does WealthApp plan to change this ‘resistant’ behaviour from investors ?

India’s AUM to GDP ratio stands at about 9 percent. In comparison, US markets boast of an AUM to GDP ratio of 70 percent. Even if we consider the global averages, 37% is the AUM to GDP ratio. While this clearly indicates the huge potential that our country has to channelize a significantly higher proportion of an individual’s savings into efficient financial products, India has been catching up very quickly.

This is due to a variety of reasons such as increase in financial awareness of the customers, efficient evolution of the regulatory framework and technology percolation across the country. WealthApp plans to use these broader trends to reach out to people and help them join the investment bandwagon. To keep the entry barriers low for our customers, we offer investment plans with as low as Rs. 100 investment minimums. We will also add more investment products in the future that we believe our customers will be able to benefit from.

Can you please talk about the funding of WealthApp ?

WealthApp raised about USD 440,000 in seed funding in December 2016. The startup’s investors include some very marque names such as NuVentures managing partner Venk Krishnan, Daksh eServices co-founder MJ Aravind, Vikram Kotak, Managing Partner at Crest Capital and Investment, Jayant Davar, Co-chairman & MD at Sandhar Group, Ramkumar Nishtala, MD & CEO at Vistaar Finance, and Arjun Sharma, chairman of the Select Group.

Can you share some insights into the customer demographics of WealthApp ?

An extremely large part of the unexposed population resides in the tier II and III towns where people have no access to professional financial advisory. WealthApp came up with the concept of Online Robo Financial Advisor for all kinds of investors ranging from youngsters or first time investors to a family man and seasoned investor. Moreover, WealthApp’s internal survey of a few remote towns in Karnataka revealed that about 80 percent of the population there spend at least 20 percent of their income on smartphones and data usage. Rest is reserved for household expenses and cash savings.

People there are actually very tech savvy, largely on mobile phones. And contrary to our belief they have a decent appetite for investment. But most invest in chit funds and other inefficient instruments since they have no one to guide them.

Once user has created an account on WealthApp [and all his investments from various AMCs are under one window], what other services does your team provide to the investors so that they can get more returns from their investments ?

WealthApp analyses an individual’s risk appetite, need to take risk and tolerance for risk based on factors such as income, assets, savings and financial goals that one may have. After an investment is made, the app tracks and monitors the complete cycle, alerting and suggesting investors on due payment, or any change in rules. The app also updates users over the need for liquid cash and provides options to obtain it. The platform is being enhanced further to accommodate more such situations that a customer may face over an investment lifecycle.

Can you give a small glimpse about the tech behind WealthApp ?

WealthApp has developed sophisticated iOS and android mobile apps to help the middle-income groups and retail investors in India simplify their financial planning and wealth management process. Sophisticated algorithms automate the entire advisory process thus ensuring top notch and timely advise for the investor. That the smaller cities and towns face data connectivity issues doesn’t deter WealthApp.

The app is built to use data efficiently. It is a light app that works on 2G bandwidth also. Currently, WealthApp’s user interface is English. There are plans to go vernacular, primarily to target the smaller towns and cities in future.

Are there any competitors of WealthApp, if so what are some of the USP’s of WealthApp vis-a-vis the competitors ?

The segment is growing as more people start lookingfor financial investment products to broaden their portfolio beyond traditional products such as gold and real estate. Some of the USP’s of WealthApp vis-a-vis the competitors are below:

Prospective Clients made investment ready via KYC in a thoroughly paperless manner with a very simple and streamlined on-boarding process

Sophisticated algorithms automate the entire advisory process thus ensuring top notch and timely advice for the investor

Knowledge and experience of the founding team work to provide customized portfolio most suited for investors and their goals based on thorough research and strategy

Ongoing monitoring 24/7/365

Supported with convenience of doorstep service offered via web and mobile apps

Equipped with a team of seasoned professionals for those that require the age old personal human touch

WealthApp is currently limited to MF’s, are there any plans/timeline on whether it would be expanded to cover other financial instruments ?

WealthApp Financial Advisors is an automated investment service, conceived over a year back. It makes use of its user friendly online platform to offer best in class investment portfolio to its clients. This is based on their financial goals and ability to take risk, and mutual funds offer various advantages to build customized investment portfolios. Having said that, the company plans to add more investment options in the near future.

What are some of the methodologies that your team plans in order to keep the investors hooked on to the platform [primary reason being investments are mostly planned by investors and most cases, they would not invest more unless required, unlike shopping which is more adhoc and also more repetitive and hence more stickiness.] ?

It’s our endeavour to engage our customers meaningfully while adding value to them. A slick and customized dashboard makes it convenient for them to see their investment status on the go and they keep coming back to it often to review their portfolios. They like the fact that we don’t use jargon and provide them all the information that they need in an easy to understand manner.

We also write articles and blogs frequently on topics that are of high relevance to our customers. Again, simplicity of conveying the messafge is the key so they keep coming back to read up and make themselves more knowledgeable on areas of personal finance. Our customers also appreciate the value in our periodic automated reports that reach their mailboxes.

There are various investor initiatives like #MFDayon7th by Reliance MF and CNBC TV18, does WealthApp have plans of starting an investor education initiative [or something else] in order to widen the horizon of passive investors [that could be an integral part of the investors eco-system, but dont know where to get started] ?

WealthApp has been at the forefront of customer education right from the start. We have conducted more than 50 roadshows [in metro cities and beyond] till date to spread awareness and provide simple solutions to people’s money problems.

Our platform is coded with complex algorithms by our engineering team and they have kept it up to date with the ongoing developments in the policies and reforms in our economy. The idea is to reduce the human intervention while we interact with our customers and be fully transparent.

With growing investor and entrepreneur interest in Fintech, many wallet companies like Paytm, FreeCharge, MobiKwik, etc. are plannig to have a boutique of finance products on their platform, does this growing competition have an impact on a startup like WealthApp and how it could result in expansion of the fintech ecosystem ?

Since the evolution of technology and start-up boom, Indian economy has been a huge market place for various types of businesses. Every entrant in the start-up space has been looking at diversifications based on their growth and funding options available around them. Also with the growing economy and huge population, fintech ecosystem has so much potential yet to be unlocked.

At WealthApp, the team comes with a tremendous domain knowledge and experience in the financial sector. We are glued on to the ongoing actions and want to be the best in the market with providing right products and offerings with a remarkable customer service. The market looks extremely responsive for WealthApp at the moment and we would like to be focused on our current service offerings instead of diversifying into many portfolios at this point of time. Currently, WealthApp deals only with mutual fund portfolios because MFs are very well regulated, are very difficult to understand, and the seed money requirement is very less.

You mentioned earlier that there is a growing demand of products like WealthApp in tier-2, tier-3 cities [and beyond], what are some of the marketing initiatives that your team has taken in order to penetrate into that particular market ?

The tier 2 towns and beyond is where the potential lies untapped. The revolution in technology and touch of power has reduced the distance between both the worlds. It has digitally enabled the end customer to gain access to the knowledge and information today. This has opened up new dimensions for them to look into new avenues of investment options.

It has created inroads for WealthApp to proceed further and we are equipped with sound knowledge on the subject. We have created a team of experts who reach out to the end customers in these markets, helping them in communicating the knowledge on investments, building portfolios and managing them. We have been working with the target audience in various parts of the country.

Along with the integrated AMC approach, building investor porfolio as per his requirements, etc. your team also provides advisory services to your customers. Are these services charged and how has been the customer response to these services [since none of the finance platform provides such tailor-made services] ?

At WealthApp, the platform is equipped to build a persona of the customer on its platform and provide advisory recommendations for investments. The automated investment service has been kept free of cost while some specific value added serives are being developed that may be on a chargeable basis. Market response to our platform has been terrific so far and we are extremely encouraged to serve our customers in the best possible manner.

What is the revenue model of WealthApp and does it follow the Freemium model ?

WealthApp does not charge its customers for the automated investment service platform. It charges the fund houses a small fee. There are a number of tools and products in various stages of development and testing that may be used by the customer for a fee.

Are there are any RBI guidelines regulating the app based businesses [P2P, Line Of Credit, etc] in India or to put it the other way round, is there a requirement to regulate them ?

The app is a channel to reach out to people conveniently. The entire advisory on our platform are fully regulated by SEBI while the payments are governed with the rules laid out by the RBI.

2016 was a tough year for startups [especially from funding point of view], how according to you should entrepreneurs deal with such adverse situations ?

Having recognized a real need gap in the market and put in place a solution that adds real value to the customer, what remains critical for an entrepreneur to tide over such times is an ability to evolve as they learn alongside persevering.

After demonetization, there has been a huge demand for payment apps [including UPI], wallet providers providing investment options like Digital Gold, etc. do you see that trend working in favour of apps like WealthApp [that makes an investor’s life smoother] ?

Absolutely. As more and more people become aware of digital platforms and become comfortable using them, it helps us explain the delivery mechanism of our service to our customers in a more contextual fashion.

As per your entrepreneurial experience, when should an entrepreneur look out for external funding ?

A couple of common circumstances when one should seek external funding could include situations when you either need funds to build/improvise your product/service or when your own revenues are not sufficient to sustain growth.

Some books that you highly recommend for entrepreneurs

Some of my recent reads that I recommend for entrepreneurs are Shoe dog by Phil Knight, Predictably irrational by Dan Ariely and The Inevitable by Kevin Kelly.

Some closing thoughts for our readers!

Effective financial management is key to meeting various life goals. This could include various aspects of our lives such as savings, expenses, investments, budgeting et al. To do any or all of this, one should seek the help of qualified financial experts to guide them through the process.

Choosing the right financial advisor is key and you must ask all questions that you need answered to make a well-informed decision. Keep in mind that the amount of wealth that we build is less a function of our income and more a function of our savings rate. And while they say money can’t buy happiness, I beg you to reconsider.

We thank Gaurav Dhawan for sharing his insights with our readers. If you are planning to put your money to work via smart investments, then you should download WealthApp. If you have any questions for Gaurav or the WealthApp Team, please email them here or share them via a comment to this article.

Fin-tech is having a huge impact on the financial services in India. It has been largely dominated by the lending and payments companies in India. Initiatives like the India Stack [UPI, e-KYC, Aadhar] by National Payments Corporation Of India [NPCI] have been instrumental in leading the Fin-tech revolution.

There are several companies in the Fin-tech sector that have innovative business models in the areas like Wealth Management [WealthApp], Digital Payments & other services [Paytm, Freecharge, etc.], Payment Banks [Paytm, Airtel, FINO], P2P Lending [i2iFunding, Lendbox, i-lend, etc.], Personal Finance Services [BankBazaar, Capital Float, etc.], Alternate/Unsecured Lending [Qbera, Loan Frame, etc.], Lending based on Credit-Line [MoneyTap], etc. Many of the fin-tech companies are leveraging Machine Learning, Artificial Intelligence, Social Data Intelligence, Blockchain, etc. in order to solve critical business problems. For example, with the help of AI, contextual data and transaction data, your wealth managers can now come up with a ‘more relevant’ financial plan that suits your requirements.

With the rising interest in fin-tech, there is a constant debate on whether Fin-tech would kill banks, but the fact of the matter is that mainstream financial institutions are also embracing change by inking partnerships with these players in order to utilize their services. Even after eKYC, there are significant challenges [that add up to delay] in customer onboarding, a problem that is being solved by few fin-tech start-ups. There is been a rising investor interest in this sector, with fin-tech topping the funding charts of H1 2017. Traditional banking institutions are utilizing this opportunity to co-create innovative solutions with entrepreneurs for building breakthrough banking products and solutions.

Last July, Axis Bank launched its flagship Accelerator Program for start-ups, the very first Indian Bank to do so. The program is run from Thought Factory, Axis Bank’s co-innovation Lab, which is located in the city of Bengaluru. Axis Bank has partnered with Amazon Internet Services, Payments product company VISA and Singapore based Oversea-Chinese Banking Corporation for co-innovating in the rapidly evolving fin-tech space. The core ideology of the lab is #UnimaginedIsUndone. The ThinkTank for Thought Factory comprises of thought leaders, change agents, serial entrepreneurs, namely Sharad Sharma of iSpirit, Manish Chokhani of Enam Holdings, Vishal Gondal of GoQii & Shankar Narayan, a Singapore based serial entrepreneur along with Axis Bank Senior Management that guides the Thought Factory team in its various functions.

Over the past year, Thought Factory has been a major Fin-Tech ecosystem enabler in Bengaluru, hosting multiple events, workshops, international visitors and other corporate clients; thereby enhancing industry-start-up collaboration.

For the first cohort of its Accelerator Program, Axis Bank’s Think Tank, from an application pool of 108, selected six emerging start-ups. Once on-boarded, the start-ups were given a structured mentorship program and access to Axis Bank’s Thought Factory office space. Axis Bank’s aim behind the program was to expedite the overall growth of these emerging start-ups along with exploring novel banking ideas with them. Axis Bank celebrated the Graduation Day of the first cohort start-ups, namely S2Pay, Pally, Perpule, Fin-techLabs, Paymatrix and GIEOM. All these start-ups target different business problems in the areas of Offline mobile payments, Analytics in lending space, Credit in rental space, etc.

Startups pitching their idea to the audience at the Thought Factory

Below are the startups that graduated from the Thought Factory

S2Pay: Enabling Offline mobile Payments [Category – Payments]

S2Pay forms a layer over payments app and enables the end consumer to make secure payments from their mobile app, even when the consumer is offline. The technology is especially useful in remote areas where there is low data connectivity thus making digital payments a reality for everyone. For more information, please visit S2Pay

Pally: AI Stack based Chatbot for Investment Advisory [Category – Investments]

Pally has created a chatbot that on the input of an image of salary slip creates an investment portfolio which maximizes tax saving for the end customer. It uses AI, Machine learning along with other proprietary algorithms to come up with a customized investment plan for each customer. Pally was also selected for the EIR program at KStart. For more information, please visit Pally

Perpule: Self-checkout on mobile app [Category – Payments]

Perpule’s app lets end customers scan the shopped products from their mobile app, and pay from within the app once the list is complete. Perpule integrates with retailer’s campaigns, thus automatically applies discounts/offers on the go. It has partnered with stores like Hypercity, More, Spar etc. For more information, please visit Perpule 1Pay

Fin-techLabs: Analytics in lending [Category – Lending]

Fin-techLabs is a financial technology innovation start-up, with a vision of providing easy access to financing across the world by powering the lending ecosystem with technology. They make the lending process swift and optimized by automating repetitive management tasks like sending emails, managing files, preparing reports, complying with regulations, etc. For more information, please visit Fin-techLabs

Paymatrix: Credit in rental space [Category – Real Estate, Payments, Credit Cards, Liabilities]

Paymatrix is an analytics-driven property rent management platform that is trying to solve the problem of credit involved in Indian rental market via enabling payments to land lords via credit cards. They also help landlords in rent/property management. For more information, please visit Paymatrix

GIEOM: Software solutions on the Cloud [Category – Analytics]

GIEOM is a cloud based software solutions and analytics company. They offer a unique business visualization technology with Intelligent linking that monitors, controls and optimizes Operations while reducing risk and increasing compliance. For more information, please visit GIEOM

The past six months have been very eventful for the start-ups, Perpule won the semifinal round of Next Money Fin-techFinals 2017 and raised a seed funding of USD 650K from Kalaari Capital, S2Pay and GIEOM on-boarded multiple new clients, Fin-techLabs and Paymatrix expanded their services portfolio while Pally evolved in its product idea and expanded its team.

We were invited for the Graduation Day at the Thought Factory, where we pitched some questions to Rajiv Anand, Executive Director of Axis Bank. Below is the brief Q&A round he had with the media/bloggers where he shares his insights about the Thought Factory, impact it has on the fin-tech eco-system, etc.

Axis Bank has always been keen on adoption of technology in its systems and solutions. Besides the Accelerator start-ups, Axis Bank along with the Thought Factory team has been working with other upcoming start-ups too. With Active AI [a Singapore based start-up specializing in AI stack], Bank is building a chatbot that can take banking & customer service to the next level.

Axis Bank’s innovation team is working on recruitment of start-ups for the second cohort of the Accelerator. For a much quicker implementation, Axis Bank is also developing a Development Platform – a sandbox environment of its APIs, which can be used by start-ups.

Additionally, they also conduct a start-up boot camp, a two-month program for grad start-up ideas under its ‘Future of Jobs’ initiative where five student teams of two members each will receive mentorship to convert their ideas into real businesses.

MoneyTap [Earlier coverage – MoneyTap review, Q&A with Bala Parthasarthy], India’s first App-Based Credit Line is now available in Kannada for the people of Bengaluru. MoneyTap, which is offered in partnership with banks, enables consumers to get instant credit from partner banks at the tap of a button on the app. The App was launched in English last year and since then has already issued close to 20 crore in credit in Bengaluru alone. The company is also planning to launch the app in Hindi and Telugu soon.

Largely focusing on the vastly untapped Kannada speaking users, the app will allow Bengalureans to avail up to INR 5 lakhs through an easy eligibility process. The company is enthusiastic about their plans to tap into the local market. According to the 2011 Census, Bengaluru’s population is over 10 million and 71% of the population speaks Kannada.

MoneyTap is available on Android Playstore and is targeted at salaried individuals and self-employed professionals earning more than INR 20,000 per month.MoneyTap evaluates the user’s eligibility in less than 4 minutes after which it provides an instant, real-time decision on the application along with the amount they are eligible for.

Using the credit line, consumers can choose to borrow as little as INR 3000 or as much as INR 5 lakhs or up to their maximum eligibility limit. Customers can decide their own EMI plans with flexible payback periods ranging from 2 months to 3 years. Interest is paid only on the amount borrowed and rates can be as low as 1.25% per month. If the user does not borrow any amount, then no interest needs to be paid. The credit limit also gets topped up once EMIs are paid back.

MoneyTap along with RBL Bank is able to provide its customers, instant decisions and instant access to money, 24/7. All financial transactions such as billing and repayment are directly dealt with the bank but through the MoneyTap App using secure APIs, thus ensuring 100% secure transactions. As an added convenience for shopping needs, a MoneyTap RBL Credit Card is also provided for the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

The Bengaluru-based startup recently raised a total of $12.3 millionin funding from Sequoia India, NEA & Prime Venture Partners. The credit line is offered in 14 cities across India and the company plans to expand to 50 cities in India by the end of 2017.

We are very enthusiastic about launching our app in Kannada. Bengaluru is one of our biggest markets. Our aim is to reduce the hassles of obtaining credit from banks and in many cases, the paperwork and verification process can delay the process by months. From small business owners to salaried professionals, all require credit at some stage in their life and we want to ensure that credit is available to them whenever they need it, on a tap!

About MoneyTap

MoneyTap is a Bengaluru-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish (sold to Hewlett Packard), which he helped grow to 100M users and $300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 (now Prime Venture Partners) where he helped create companies like ZipDial (sold to Twitter), EZETap, Happay, etc. Kunal (ex Texas Instruments) & Anuj (ex Airtel & JWT) co-founded Tapstart that grew to 300K users and turned profitable in 2 years. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap

Earlier on this blog, we have reviewed a couple of Investment Plans, Stocks, etc. and so far we have received encouraging comments. Many of the readers touch based over Facebook and informed us that they have invested in one of the stocks that we have reviewed & have yielded excellent returns! Such news motivates us to write more about Finance 🙂

When it comes to investing, we take precautionary steps like reading review about investment plan/stock/insurance online, consult known experts in the domain, consult known people who have already invested in the same, etc. However, the problem is that there is a plethora of information available online that can really confuse an investor. Same is the case with investing in stocks.

Way back in the late-1990’s or early-2000’s, investors were heavily reliant on the brokers or sub-brokers that were present in their locality. They had a good amount of information about the markets, stocks, etc. and could guide investors in person as well. However, once the technology became a key player in the complex field of investments and stock trading, traditional brokerage houses like Indiabulls, ICICI Direct, ShareKhan, etc. became the torch-bearers of this change. A majority of these brokers, also known as full-service brokers used to charge a certain percentage from the trade amount. Fast forward now, with the evolution of Artificial Intelligence, Machine Learning, Big Data and other modern technologies, the brokerage space is also disrupted by new-age fintech startups as well as established financial institutions.

There are a number of trading platforms from the likes of Zerodha, ICICI Direct, India Infoline, Edelweiss, Angel Broking, etc. and each of them has various types of Trading accounts [Standard, Prepaid], different brokerage charges, transaction charges, demat account charges. When it comes to trading, brokerage fees, website usability, yearly maintenance fees, etc. play a vital role in the growth of the platform and customer retention. We have a look at some of the trading platforms available for investors from the perspective of account opening & maintenance charges, brokerage fees, fees of stock delivery, intraday trading, etc.

Note: Review based on usage, interaction with existing users of these trading accounts, research, and other parameters.

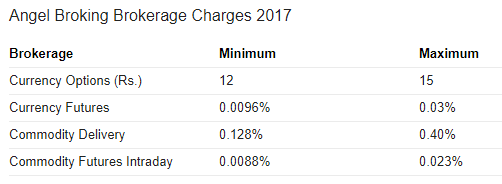

Angel Broking

Angel Broking is one of the oldest brokerage companies in the country. It is operational since 1987. They have a PAN India presence and along with technology enabled DEMAT & Trading account, they also provide offline services where investors can place orders via a phone call or by visiting their sub-brokers facility.

Account Opening Charges: No account opening charges. You can start trading in one hour. Yearly maintenance charges: No charges levied for the first year.

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX & NCDEX

Weekly research reports from financial experts

Supports both browser and app-based trading. Platform is available across mobile, tablet and desktop

Personalized customer support

Different brokerage plans Angel Classic, Angel Preferred, Angel Elite & Angel Premium available for a different set of investors. Further details can be found here

Intraday Trading: Intraday trading, as the name suggests, is trading stocks within trading hours in a single day and investors can do intraday trading on Angel Broking platform. More details about Intraday Trading on Angel Broking can be found here

5paisa.com

5paisa.com provides a single account for all your investments. They charge a flat rate of Rs. 10 per order irrespective of the segment you trade or the value of your trade. They charge Rs. 750 as account opening fees and the annual fees [for Demat and Trading account] is Rs. 400.

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX & NCDEX

Weekly research reports from financial experts

Trading platform accessible across mobile, tablet and desktop

Personalized customer support

Further details about the pricing can be found here

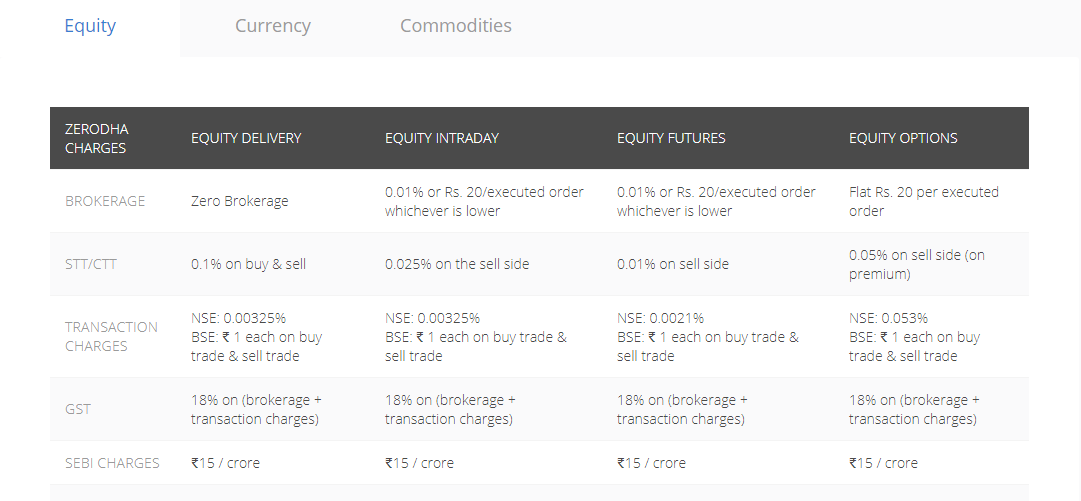

Zerodha

Zerodha is a Bengaluru based bootstrapped startup that has pioneered the concept of discount brokerage. With Zerodha, an investor can open an account instantly and start trading. They are also called as Flat Fee Share Broker since they charge Rs. 20 or 0.01% [whichever is lower] per executed order on intraday trades across equity, currency, and commodity trades across NSE, BSE, and MCX. They do not have any minimum brokerage.

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX, MCDEX, Mutual Funds, etc.

All your equity delivery investments [NSE, BSE], absolutely free

Trading platform accessible across mobile, tablet and desktop

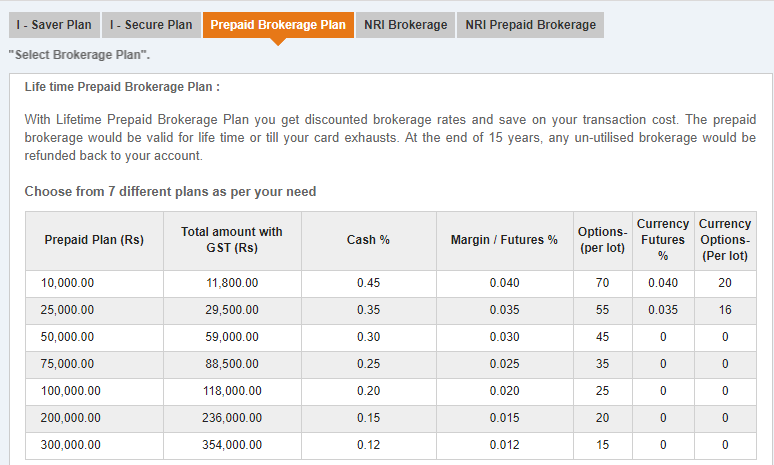

ICICI Direct from ICICI is an old and preferred broker due to its brand image. The 3-in-1 trading account gives you the convenience of opening a demat account, trading account as well as a bank account all in one go. The demat account is linked with your trading and bank accounts.

You can earn an interest of 4% on the allocated unutilized amount for trading. They have more than 150 branches which means that their services are accessible both online as well as offline. Yearly maintenance charge is Rs. 600.

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX, MCDEX, Mutual Funds, etc.

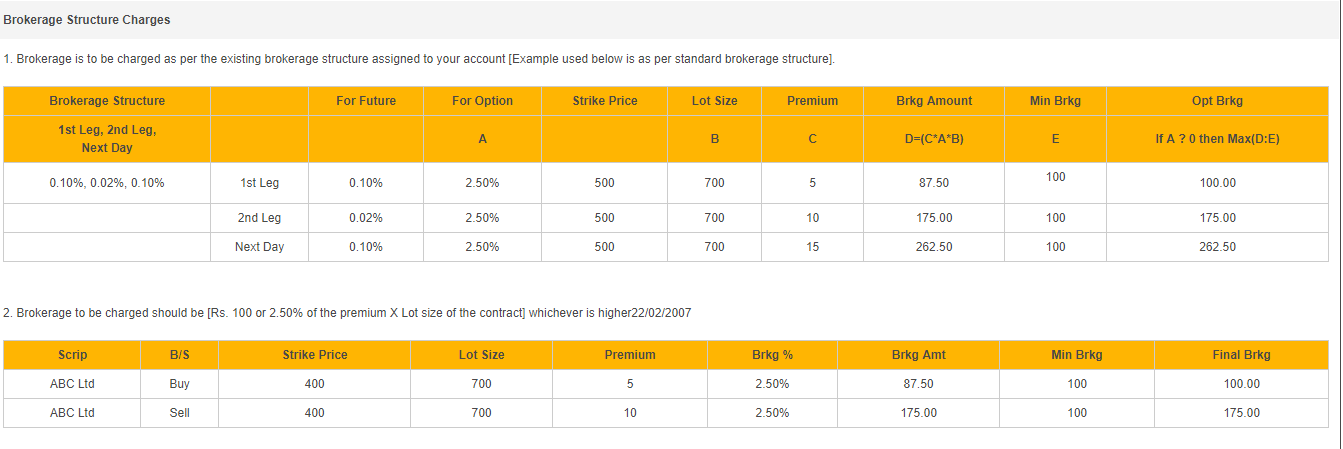

Brokerage includes DP charges of higher of 0.04% or Rs. 25 every time shares are debited from your demat account

Trading platform accessible across mobile, tablet and desktop

There is call and trade facility

More details about ICICI Direct brokerage plans [Server Plan, Secure Plan & Prepaid Brokerage Plan] can be found here

UpStox by RKSV is another popular discount broker like Zerodha. Its trading platform Upstox Pro offers zero brokerage on stock investments. With Upstox, investors can create a custom watchlist of their favorite stocks. Upstox is backed by top investors namely Ratan Tata, Kalaari Capital & GVK Davix

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX, MCDEX

Free delivery trades. Only Rs. 20 per trade brokerage

Trading platform accessible across mobile, tablet and desktop

Further details about UpStox Pro pricing can be found here

Just like ICICI Direct, ShareKhan is one of the oldest brokerage companies in India. It was acquired by BNP Paribas in 2015. There are no account opening charges but there is a yearly maintenance charge of Rs. 500.

Brokerage features and charges

Access to all market segments of BSE, NSE, MCX & NCDEX

Trading platform accessible across different devices

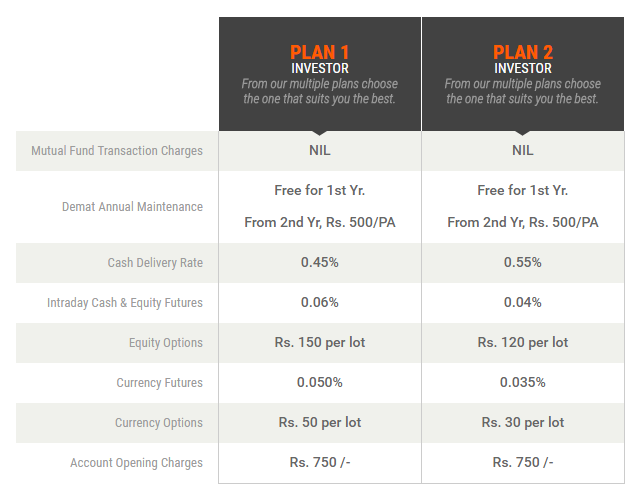

Edelweiss Financial Services Limited is a diversified financial services group. The firm has five major businesses, namely Capital Markets, Credit, Asset Management, Life Insurance, and Commodities. Its main focus is on credit. Edelweiss Broking was founded in the year 1995. They have different brokerage plans for different kind of investors.

Account Opening Charges: Rs. 750 is charged as opening a trading account Yearly maintenance charges: Free for the first year, Rs. 500 for the subsequent years Intraday Cash & Equity Futures: 0.06% [Plan 1] and 0.04% [Plan 2]

Brokerage features and charges

Access to all the market segments of BSE, NSE, MCX & NCDEX

Weekly research reports from financial experts with access to various finance Edelweiss platforms that solve deep-rooted customer pain-points

Though there are so many trading and brokerage platforms, the real pain-point that investors/stock market traders face is that most of these platforms provide detailed analysis on stocks but all the features required by investors do not exist on a single platform, some of which are mentioned below:

Market information in a single view: Due to the huge amount of ‘scattered’ information available online, it becomes painful for traders/investors to perform ‘meaningful’ research of a particular sector or stock. For example, I use MoneyControl app to keep myself updated about the happenings in different sectors. There is no single platform that gives such kind of granular information.

In-depth Technical Analysis: In addition to the point mentioned above, there is a dearth of trading/investment platforms that also cater to technical and sentiment analysis of the market. This is a gap that needs to be filled for the investor community.

Trading Execution: When an investor is trading, he executes trades from the broker’s website [examples mentioned earlier] but the broker’s terminal is entirely different. This delay might cost dearly to the trader. Hence, when it comes to trading, execution is of top-notch priority.

There was a requirement for a trading platform that could solve these problems for the investor community so that even novice investors in future can become seasoned investors. This is the problem that financial firm Edelweiss wants to solve via Edelweiss Traders Lounge. Let’s have a look at the features of Edelweiss Web and Edelweiss Traders Lounge.

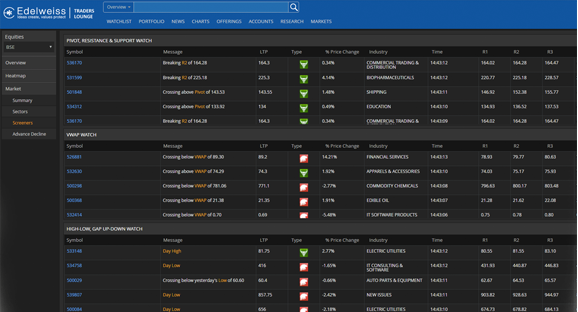

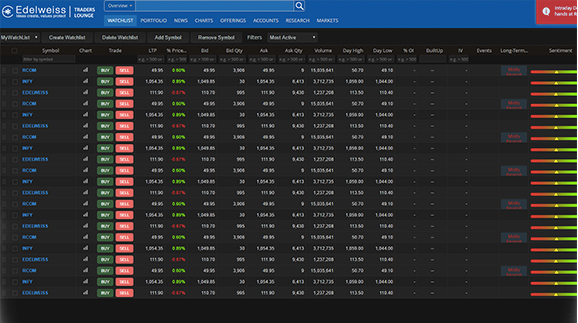

Broker’s terminal like experience: Though traders would access this platform via the web, the look & feel is similar to the broker’s terminal. The terminal supports customizable shortcuts so that you can trade faster than ever before.

Customizable watch-list combined with the power of data: In one single window, investors can get a wholesome view of the stocks that they have invested and the stocks that are on their watch-list. As mentioned earlier, the real power lies in presenting a holistic view to the traders and that is what Edelweiss Traders Lounge solves with the watch-list. It provides you with stock performance with real-time filtering & analytical parameters i.e. Sentiments, Events, Technical Alerts, etc.

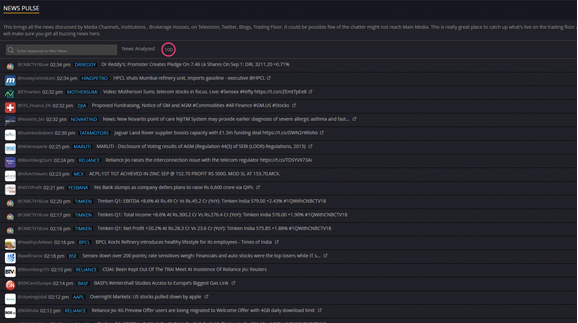

Useful information in a single-view: As mentioned earlier, investors have to scout for meaningful information like company performance, changes [if any] to the RBI monetary policy, sector performance, impact of the global economy on the stock market, etc. available on the internet and it might result in a never ending process. Edelweiss Traders Lounge solves this problem by using the power of Data Analytics.

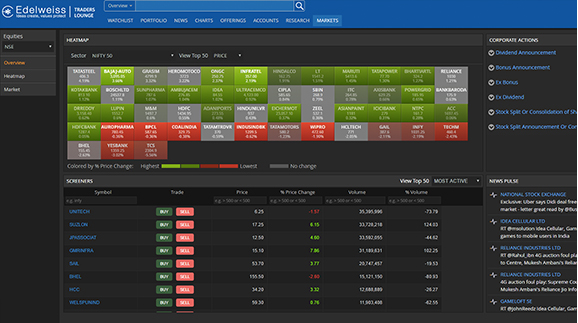

It provides Charting, Broker calls, News/Corporate Announcements/Events, Sector-wise performance, Live OI build-up, Moving averages, etc. in a single window so that you can Buy/Sell a stock after having in-depth information about that sector and the stock.

News sentiments, Broker Recommendations and Health Indicator: When it comes to investing in the stock market, it becomes primarily important to study the sector and also how various stocks are performing in that sector. With the ‘Peer Comparison‘ feature, you can compare the performance of the stocks that belong to a similar sector. With Edelweiss Traders Lounge, there is a deep level of sentiment analysis that gets done on the latest news on equities, currency & global markets, so that as an investor you can analyze the sentiment attached to the news. The expert opinions along with the sentiment analysis play a crucial role in impacting your ‘Buy/Sell behavior’.

Edelweiss is the only platform that provides in-depth information about the stocks, financial information, technical graphs/charts, detailed news related to stocks and more. This enables the investor to analyze, identify and trade on the same platform. Along with these features, the platform also gives whether a particular stock is listed as BUY [Green in color] or SELL [Red in Color] by the broker community.

If you are a heavy-duty trader and looking for an efficient desktop trading software then you should look no further than Edelweiss Xtreme Trader. It is a terminal based trading platform that is loosely based on Edelweiss Traders Lounge. The interface is highly customizable and can be changed to suit your requirements. The tool has advanced charting tools so that you can track the performance of your stocks.

The tool also has SMS and email alerts that can be customized as per the sector that you have opted for. Xtreme Traderensures that the research calls are flashed instantly on your screen, the moment research team generates so that you do not miss out on any trading opportunity.

When it comes to brokerage charges, exchanges that are enabled, account opening costs, etc. Edelweiss Trading scores lesser than Zerodha but significantly higher than ShareKhan. However, from a usability perspective, Edelweiss trading platform scores significantly higher than the other trading platforms! The trading platform from #Edelweiss facilitates #EasyTrading, a requirement which is the need of the growing investor community!

What is the brokerage platform you use for trading, please leave the message in the comments section…