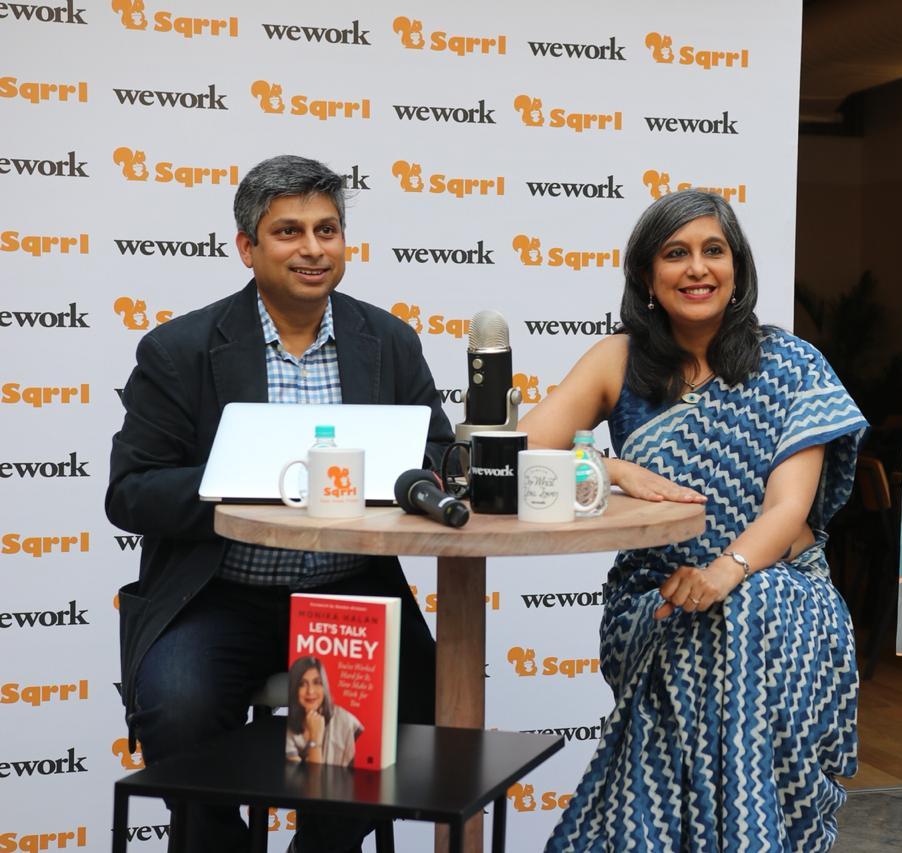

Sqrrl – an intuitive DIY digital platform aimed at getting Indians into the habit of investing and learning about personal finance, launched a Personal Finance talk show Sqrrl Chatter at WeWork, a co-working space in Gurugram. The chat series is aimed at people who want to learn about investments by starting small and get better at money management.

This launch event attracted 30+ startups from Delhi NCR and gave the attendees an opportunity to increase their wealth by understanding what goes into taking the right and personalized investment strategies.

Currently, Sqrrl has a strong foothold in more than 600 cities of the country. With 2,50,000+ application downloads of Sqrrl, the focus of the company is to raise financial awareness in the country and encourage people to invest more, by starting small.

Sqrrl Chatter, conducted at WeWork Gurugram, paved a new way of gaining financial wisdom from the Industry Experts, who have been there and seen it all. The Event also saw the book launch of “Let’s Talk Money“, by Ms. Monika Halan, Consulting Editor of Mint Newspaper, who talked about some of the interesting aspects of the book and also gave worthy suggestions regarding investments and money management.

According to Monika Halan, Author of Let’s Talk Money

Considering the fast-paced era we are living in today, it’s very important for millennials to start saving early in life. Although it’s advisable to not get too ambitious about saving all at once. Instead one should divide his/her salary in three types of accounts – inflows, consumption and saving/investment. This way it will be easier to set yourself to start saving.

Money is one of the most enigmatic subjects. Just thinking of it evokes a wide variety of emotions. Most young Indians find handling money to be complex. On top of that, the financial services industry has heavily jargonized everything to drive a knowledge wedge between itself and consumers. The need of the hour is to make the subject simple, easy, relate-able, relevant & automated.

About Sqrrl

Sqrrl is making honest and differentiated efforts to help millennials save and grow their money effortlessly! It is using automation as a tool to help users make saving money, a habit; be it saving up for a dream holiday, their startup or any one of the several hundred reasons one might need money for. Started in March 2017, Sqrrl reached the milestone of 2,00,000+ users within a fairly short span and is expanding aggressively, making new inroads across more cities. Sqrrl is also the world’s first mobile app platform, in the finance space, operating in Hindi, and currently supports in a total of 9 Indian languages.

LALA World, the leading fintech organization aiming to develop an AI and Blockchain powered global, digitally-decentralized financial ecosystem, has partnered with TransferTo. TransferTo is a leading global digital value services network. A first for a Blockchain-based company, under this collaboration, LALA World will have direct access to TransferTo’s services network to offer its customers mobile top-up solutions in over 150 countries.

Globally, there are over 5 billion mobile phone users and the demand and need to stay connected – with call, text and data access – is high. This key partnership with TransferTo will enable LALA World to access over 600 mobile operators, across more than 150 countries and offer its customers a safe and reliable solution to seamlessly top-up the mobile phones of their loved ones back home – all credited in real-time, directly to the recipients’ mobile, and in local currency.

LALA World has a mission to touch more lives every day and connect people through digital financial services. By partnering with TransferTo, we are able to accelerate our global expansion as we grow our product portfolio, thereby enabling easier solutions for our customers to stay connected across the world. TransferTo is a digital value services leader and innovator, and we are thrilled to be joining such a successful network.

We are very pleased to be welcoming LALA World into our global network. Our technology will enable it to seamlessly connect to our platform, through a single API connection, and by interconnecting it with our network partners, LALA World will have the ability to expand its portfolio, grow its business and deliver new solutions to customers.

LALA World iOS and Android app users can use the services not only in India, but they can now recharge the mobiles of friends and family in 150 countries across the world. TransferTo first launched its digital value services network in 2005 and has since processed more than 450 million transactions.

About LALA World

LALA World is an established and fast-growing Asian technology company using Blockchain to create a connected financial ecosystem for the unbanked, migrants and refugees around the world. Founded in 2016 and headquartered in Singapore, LALA World is a social business with a presence in 5 countries and over 100 global partners including government agencies and NGOs. LALA World’s vision is simple – to touch 100 million lives by 2020 and make them better. For more information, please visit LALA World

Investec India had also advised Kissht on its Series B led by Fosun in November 2017. Investec India has built a strong advisory business over the last few years within the Indian Venture Capital ecosystem. Investec India has advised companies across a wide range of sectors on Equity Fundraises at Series B and above, including Kissht, Bizongo, Treebo Hotels, OfBusiness, BigBasket, Pepperfry and Quikr. The firm also advised on the sale of CitrusPay to Naspers – one of India’s largest Fin-Tech M&A, and on the sale of Sokrati to Dentsu – one of India’s largest Digital Media M&A.

Frankie Brown of Investec Capital Services (India) Ltd said

With our unique position in the Indian market, we believe that Investec India is well placed to advise businesses across the Fin-Tech spectrum. We have a long-term relationship with Kissht, and this partnership has successfully resulted in both the Series B and Series C fundraises. The $30 million Series C round will see Kissht perfectly placed to consolidate their market leadership position. Investec is investing significantly in the Fin-Tech space across the both in India and globally.

Vinit Barve of Investec Capital Services (India) Ltd said

Technology led lending has opened up a huge credit opportunity in India. Kissht has established a leadership position in the consumer Fin-Tech segment. With its consistent growth, strong unit economics and enviable NPA record, Kissht has taken the right steps in the direction of building a mighty lending institution. This investment, led by Vertex and Sistema with participation from existing investors, will enable the company to achieve the next level of growth and cement its leadership position in the consumer financing segment.

Founded in 2015 by Krishnan Vishwanathan and Ranvir Singh, Kissht provides product financing and personal loans to its customers through a financial technology platform which is integrated with online and offline merchants. Kissht has developed its own self-learning proprietary algorithm which assesses a customer’s credit profile in a fraction of a second based on 2,000+ digital footprints.

Kissht has demonstrated remarkable growth with impressive record on credit costs. The business had previously raised its Series B round from Fosun RZ Capital, Prophet Capital, VenturEast and Endiya Partners in 2017. Currently Kissht is present in 50+ Online and 2,000+ Offline points of sale across categories including consumer durables, electronics, health, alternative energy & education, enabling customers to easily access credit for their purchases.

Kissht will use this funding to penetrate its business further into both offline and online merchants, and deeper across categories and further enhance its data and analytics capabilities as it seeks to cement its leadership position in the highly under-penetrated Indian consumer credit market, as well as investing further in technology and building the team.

NiYO Solutions Inc. [interaction with the NiYo founder here], a new-age digital banking solution for salaried employees, announced the launch of the Global Card, aimed at making international transactions safer and inexpensive. International travelers are always burdened with the high currency exchange rate charged by issuing banks for all transactions made outside the country. This rate can vary between 1~3% of the amount transacted. Banks also charge either a flat fee or a set percentage of the transaction amount, in addition to the currency exchange charge. In fact, travelers face a variety of issues with current multi-currency cards, starting from the difficulty in issuance, having to go to a branch to load/unload currency, challenges in tracking spending, etc.

The NiYO Global Card offers instant setup, convenient loading from any account via NEFT/IMPS, ZERO currency exchange premium, and zero international transaction fees on usage anywhere in the world. This makes present day multi-currency cards and traveler’s cheques redundant.

The card is supported by a cutting edge mobile banking app which gives users ability to lock and unlock either the full card or a payment channel anytime, anywhere. The app also provides real-time notifications on usage, exchange rates, and refunds, while helping users find convenient ATM locations, avail nearby offers, and much more.

If you are a business traveler, you can submit claims on-the-go by adding bills for each transaction right in the app. These claims can be instantaneously approved by your organization via the NiYO Corporate Portal. The NiYO Global Card is being launched in partnership with the DCB Bank and can be used at ATMs, POS terminals, and for online transactions in any country.

Features of the NiYO Global Card

Can be used at over 2 million VISA/MasterCard ATMs and over 35 million merchant outlets across the world

Load the card and check account balance in INR, no need to add international currency

For security, the card can be blocked using the NiYO mobile app and can be locked through the app when not in use

No minimum balance or low balance fines

Real time notification alerts of transactions

Users can reload the card instantly with ease from any bank account via NEFT/IMPS

Additional offers and benefits available at select outlets across the world

Features such as ATM locator and travel insurance included with the card

The United Nations World Tourism Organization [UNWTO] has estimated that by 2020, India will account for 50 million outbound tourists. With 65 million Indian passport holders and the ease of access in obtaining visa-on-arrival in more than 50 countries, it is no surprise that global spending by Indians is on the rise. According to the regulations by the Reserve Bank of India, Indian travellers are allowed to spend up to $250,000 outside the country in a year, in areas such as investments, education, medical expenses, property transactions, gifts, and donations.

By January 2018, Indian travellers had spent $1.2 billion abroad within 10 months. This has created immense opportunity for travel-friendly cards, and NiYO aims to be the market leader in this space. NiYO plans to issue 5 millions cards in next 2 years.

Vinay Bagri, CEO and Co-founder, NiYO said

I have seen people struggle with present day foreign currency solutions during travel and decided to make one of the best travel card solutions in the world. With the NiYO Global Card and App, we have achieved that. Our Mobile app, with path-breaking features like card control, channel control, and real-time notifications, and a card with zero markup and global acceptance, means that whether you are traveling for business or personal use, NiYO Global Card is the only card you need.

About NiYO

Founded in 2015 by Vinay Bagri and Virender Bisht, NiYO’s mission is to increase cash flow for all salaried individuals by leveraging technology in the areas of payroll & benefits. NiYO features an integrated solution comprising of a Multi-Pocket Card, a Mobile App, and a digital account with multiple wallets.

Vinay has spent more than 18 years working with diverse organizations like Parle, 3M, ICICI Bank, SCB, ING, and Kotak Mahindra Bank. He combines a deep understanding of distribution and retail banking, having spent over a decade in leadership roles across unsecured lending, retail liabilities, corporate salary, and retail banking strategy.

Virender is a seasoned technology professional with 16 years of experience in creating world-class software products for companies like MobiKwik, Makemytrip [MMYT], StudyPlaces.com, Exponential Inc, GE Medical Systems, and Tata Consultancy Services. Virender is a hands-on technologist and has a reputation for building scalable solutions for e-commerce and payments domain.

There is a famous quote – ‘Risk & Rewards are two sides of the same coin’ and the same is applicable for monetary investments. However, the investment portfolio would differ from person to person since it is dependent on many factors like risk appetite, assets, liabilities, dependencies, etc. and hence, it becomes virtually impossible for any investment firm to cater to varied investment requirements of such a large audience.

There is a wrong notion that investing in Mutual Funds or SIP’s is similar & equally risky as investing in the stock market. Due to this, less than 1.5% of the Indian population invested in equity markets and only 2% of India’s household savings were exposed to equity [as per a report from Bloomberg]. However, times are changing and more & more people are willing to invest in SIP’s for long-term benefits, given that they get proper guidance.

This is the problem that many new-age Fintech companies are trying to solve using Machine Learning, Artificial Intelligence, etc. by giving investors more personalized tailor-made portfolio suggestions based on their persona, long-term & short-term goals, etc. As it is said, you learn from your own mistakes and the 2008 market crash resulted in an Aha moment for entrepreneur Arjun Sarkar. Though he lost a significant amount of money in the crash due to misguidance, he soon realized that it was a ‘larger’ problem that required to be solved. Arjun Sarkar, along with Anup Abhonkar co-founded Everguard Life Ventures Pvt. Ltd. and came up with their first product named SIPtm with the aim to make equity investing simpler by taking investor’s persona and various other data points into consideration. In this episode, we have a chat with Arjun Sarkar, Founder & CEO of the Pune-based startup. The Q&A revolves around the core product SIPtm, fintech, persona-based investing & more. Let’s get started with the Q&A…

Note – ‘I’ in the interview refers to Arjun Sarkar.

Can you walk us through the idea of SIPtm and the team behind the same ?

Idea of SIPtm came to solve the problem of investing for retail investors i.e. answering the questions – Where to invest?, When to invest?, and How much to invest? Because the investor does not know what to do, they invariably go for the default option i.e. trust their friendly neighbourhood bank which is the worst decision they can make. Personally I lost a significant portion of my net-worth in the 2008 crash because I was misled by my relationship manager and invested in the wrong product, that’s when I started taking this subject seriously.

The team comprises of myself – Arjun Sarkar, CEO & Founder of Everguard Life Ventures Pvt. Ltd., the parent company behind the development of SIPtm. I have an MBA from University of Toronto. I have personally managed money for CXO’s and NRI’s in tens of crores for close to a decade and 80% of my personal wealth is invested in mutual funds.

Anup Abhonkar, CTO & Co-Founder has over 18 years of IT experience across domains like Banking, Insurance and Securities. He has worked for leaders in the industry like, Accenture, Barclays and Wipro delivering business critical solutions for Fortune 500 organizations like Aviva and Charles Schwab.

Both of us are passionate about our field. Ask our wives and you will find that we spend most of our time talking about the subject.

What does ‘tm’ stand for in SIPtm ?

TM stands for Through Mobile.

What are some of the data points that you take while recommending a particular SIP or Investment to a particular customer ?

We follow a thorough process backed by research, where we consider multiple quantitative and qualitative factors across domains like Economics [Macros and Micros] and Market and also take customer specific inputs like time-horizon and quantum of investment before suggesting a fund. Research further shows that some categories of funds are better suited for SIP mode of investments so we take that in to consideration as well.

In other words, it is not a cookie cutter approach of following ratings of funds or just looking at the past performance of funds. We are talking investments here, not buying e-commerce products where customer can buy just based on reviews and ratings, they may do well in the short term but will not able to sustain it for a meaningful period of time.

Please talk about ‘Persona Based Investing’ and how can millennials use a platform like SIPtm to plan their investments and maximize their savings ?

‘Persona based investing’ is a concept which maps life stage of investors to priority goals which then helps to filter the optimal investment mix for them. SIPtm is a great product for millennials as it is prescriptive in nature i.e. it is like a doctor listing out the medicine and the dosage which makes decision making very simple. More importantly, the dosage or SIP amounts are in the range of typical monthly savings which can be channelized in a disciplined manner thereby earning much higher returns than other traditional saving products like recurring deposits or insurance products.

Which is the target market segment of SIPtm and can you share some details about the customer demographics of SIPtm ?

Target market segment of SIPtm is people with regular income as SIP mode of investing is a good fit for them.

There are lot of Fintech companies like Scripbox, Sqrrl, etc. that are into goal-based investments, what are the USP’s of SIPtm over their competitors ?

SIPtm is a vehicle to achieve goals but takes a different route than its competitors to reach the goal faster, more predictably and with less volatility. The USP is in the name itself, the app is built ground up for SIP investments only i.e. no lump sum investments which makes the journey less bumpy and more predictable.

The other differentiator is that SIPtm offers a complete solution, right from prescribing the monthly SIP amount, to selection of funds, to distribution of monthly amount between the funds. More importantly, it re-balances the portfolio at appropriate times during the journey i.e. It does not take the fill it, shut and forget it approach.

We are a fintech company i.e. a financial services company that leverages technology to make life easier for our customers. Not the other way round i.e. a technology company that has built a financial app? The nuance is very important as you are suggesting an investment solution not a consumer commodity like laptops and mobile phones where ratings work.

As per a report, there is very small percentage of investors/would be investors who plan to invest in the Equity market [or MF], how does SIPtm plan to change this ‘resistant’ behavior from investors ?

Resistant behaviour is because of fear of loss – The answer is SIP mode of investing as SIPs manage volatility better and as a result, give higher returns at lower risks. Also, SIP amounts are small, so you are not putting a lot of money at risk at any point in time. In case of SIPtm there is another level of assurance, as the suggestions are coming from experts based on 5000+ hours of research. There is also a visible change in the behaviour in the recent times, as per latest figures, India is raking in over a billion dollars in SIPs per month now.

What is the Total Addressable Market [TAM] that you are trying to address with SIPtm?

20 Million SIPs with average investment of Rs 5000 per month

How is the response from the early adopters of SIPtm and what are some the best features that are liked by the community ?

The response from early adopters is great with SIP values ranging from Rs. 5000 right up to Rs. 20,000 per month. The best feature liked by the community is the prescriptive investment suggestion and the overall simplicity of the investment experience.

Currently how many AMC’s are syndicated on the SIPtm platform and how frequently the data is updated on the app ?

This is one more differentiator for us, we have shortlisted only the top 5 AMCs of the country based on some key criterion’s, one of them being the staying power and that is a conscious decision. We may add a couple more in the near future if they pass the criterion’s that we have laid out.

SIPtm Core Team – Anup Abhonkar, Co-founder & CTO [L], Arjun Sarkar, Founder & CEO [R]

Once the user has created an account on SIPtm [and all his investments from various AMCs are under one window], what other services does your team provide to the investors so that they can get more returns from their investments ?

The most relevant and important service provided is the rebalancing of the portfolio and timely interventions to ensure that the customer goal is achieved in time.

Can you give a small glimpse about the tech behind SIPtm ?

SIPtm App has a very simple process flow and UI only because, underneath lies a network of multiple systems, including the App back-end, payment gateway, our back-office tech and RTAs and these systems talking to each in a secure and efficient manner through APIs.

What is the on-boarding process for customers on SIPtm and how has initiatives like IndiaStack, Aadhaar, etc. helped Fintech companies like SIPtm in on-boarding & other services ?

The Customer on-boarding process is very simple and totally paperless. We take minimalistic information from the customer as a one time setup. We know paper work is boring, however this basic information is a part of the Regulatory requirements. After verifying the Customer information, we activate the customer. The customer then goes for the eMandate process. Here is where we use the Aadhaar based e-Sign process that is very simple and reduces the manual 15 days process to just 3 days. So yes, Aadhaar helping immensely in reducing the cycle time as well as going paperless.

SIPtm is currently limited to MF’s/SIP’s, are there any plans/timeline on whether it would be expanded to cover other financial instruments ?

Not in the immediate future as we want to focus all our energy in one area that we are really good at and an area that is under penetrated.

With growing investor and entrepreneur interest in Fintech, many wallet companies like Paytm via PaytmMoney, FreeCharge, MobiKwik, etc. have launched a boutique of finance products on their platform, does this growing competition have an impact on a startup like SIPtm and how it could result in expansion of the fintech ecosystem ?

We do not consider wallet companies as competitors as they do not have the expertise or experience in mutual fund investments. It is like going to a pharmacist who just stocks different products and asking them for a recommendation on medicines to treat a serious disease. But the fintech ecosystem can benefit if the wallet companies tie up with players like SIPtm as, as they can generate an incremental revenue stream and actually add real value to their users by helping them generate wealth vs earning cashbacks.

Does SIPtm charge any commission from the investment that is being done on the platform ?

Not directly from the customer but through the AMCs we have partnered with. That being said, we do not push mutual funds suggested by the asset management companies as a typical distributor does, just position funds shortlisted by our algorithm.

What is the revenue model of SIPtm and does it follow the Freemium model & do you plan to be a preferred investment partner for enterprise customers ?

As of today our revenue model is commissions. Yes, we plan to partner with enterprise customers in the future but the value proposition for them has to be worked upon.

There is a growing demand of products like SIPtm in Tier-2, Tier-3 cities [and beyond], what are some of the marketing initiatives that your team has taken in order to penetrate into that particular market ?

Yes, we are in talks with potential partners who have a strong existing network in the Tier-2 and Tier-3 cities.

SIPtm is backed by a very experienced founding team and there are very experienced domain-expert mentors behind SIPtm, how has the mentorship helped your team in building the ‘right set’ of features on SIPtm ?

The mentorship has helped us focus on the essentials and cut out the noise. Some of our key decisions on the product road-map have come through the regular calls we have with our advisors. The right set of features has come through a market research project we conducted for our target segment before developing SIPtm and we continue to collect feedback from our live customers.

Can you touch upon the funding of EverguardLife Ventures & are looking for institutional funding in the near future ?

Everguard is internally funded as of now, but we are looking for institutional funding this year for product development and marketing.

The app is currently present on Google Play Store, is there any timeline for the app to be released on the iOS platform ?

We are currently focussing on building traction and incorporating valuable feedback into the Android version. Work on the iOS version is underway and we shall release it shortly.

Do you plan to follow an app-only strategy or there is a plan to open-up a desktop version of the SIPtm platform [since it would definitely be useful for users who log-on the platform from their work location] ?

SIPtm is an app as mobile phones are the preferred mode for our target segment based on our customer research. That being said the algorithm that runs SIPtm is based on our earlier desktop platform called Finanswer which we plan to develop further for other target segments.

After demonetization, there has been a huge demand for payment apps [including UPI], wallet providers providing investment options like Digital Gold, etc. do you see that trend working in favor of apps like SIPtm [that makes an investor’s life smoother] ?

Absolutely, as users get more comfortable using and moving money through Apps it will help apps like SIPtm. We however, do not see payment apps as serious competitors because of the differentiators we touched upon earlier.

2017 was a tough year for startups [especially from funding point of view], how according to you should entrepreneurs deal with such adverse situations ?

Entrepreneurs should always be prepared and focus on their customers to earn revenue. Also, look out for investors who understand your domain well and who can help raise money when it is required, so that the team can focus on the product and business development.

SIPtm team is currently working out from a co-working space in Pune, what are some of the advantages for a startup/growth company while working out from a co-working space ?

You grow your network and get a chance to test your ideas quickly since the target segment is around you and more accessible.

There is lot of talk about implementation of Blockchain, AI, etc. in Finance & Fintech, what are your comments on the same and where do you see the tech moving ahead in the next 3~5 years ?

The ‘Blockchain’ and ‘AI’ landscape looks promising in delivering value to businesses and thereby increasing customer service levels which is very important in Finance. Organizations currently are trying to get a hang of it in multiple use cases and it will be a mainstay in the near future.

Some books that you highly recommend for entrepreneurs and some closing comments for our readers ?

We work really hard all our lives to earn money but do make our money work hard for us, by the time we realize this, half our working life is over. I would advise your readers to start investing early as time in the market is the most important factor and it is totally under our control. Investing is a process, boring maybe, but definitely life changing if taken up seriously.

SIPtm for Android can be downloaded from here. We thank Arjun Sarkar for sharing his insights with our readers and walking us through his journey. If you have any questions for him, please share them via a comment to this article or email them to himanshu.sheth@gmail.com

According to recent industry reports, 156 million of Indians who comprise the ‘urban mass’ and ‘urban middle’ section representing an annual income of USD 3000 and above have the potential of mass adoption of consumer credit. Of this the ‘urban mass’ constituting approximately 129 million have been mostly deprived of credit due to lack of credit history.

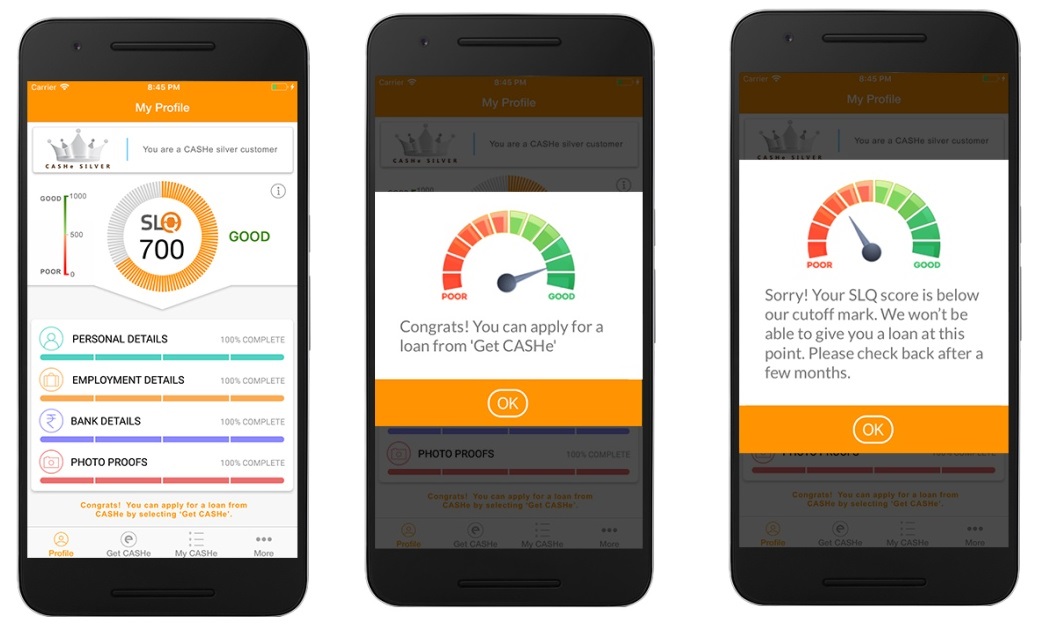

Addressing this major concern, CASHe, India’s leading digital lending company, promoted by serial entrepreneur and private equity investor V. Raman Kumar, announced the launch of India’s first alternate credit rating system – The Social Loan Quotient [SLQ].

India’s first social behaviour-based credit-rating system, SLQ is a fast, unique and a path-breaking real time platform which leverages big data analytics, artificial intelligence and predictive tools. The innovative platform will help score millions of Indians, who otherwise have been left in the lurch for lack of consumer credit in the absence of credit history.

Considering the young urban mass prefer to avail small ticket loans for short term, the existing traditional lending platforms such as banks and NBFCs’ find it unviable to serve the segment. In addition, the lack of credit history further dampens the situation. Here SLQ will play a pivotal role in helping this large untapped population to avail credit on the basis of the score generated by the system. Soon, the platform will also be set open to other institutions [banks, NBFCs’ and credit bureaus] to integrate and avail the system thereby helping them reach out to the masses.

Unlike conventional lending agencies who rely only on an applicant’s past financial transactions, CASHe’s revolutionary approach links multiple online and offline data points like his mobile, social and media footprint, education, remuneration, career and financial history to calculate the borrower’s credit score.

Speaking on the launch of this new credit scoring innovation, the CEO of CASHe, Ketan Patel, said:

Credit is critical for the growth of an economy. It incorporates the element of aspiration and infuses growth to keep the economy up and running. However, the lack of alternative credit models, challenging capital eco-system and an unviable cost structure have kept mass India deprived of quick and reliable credit.

Through SLQ, we are focused on those who may have little or no credit history with traditional lending institutions. We hope this will revolutionize the digital lending space in the country and encourage other credit institutes and agencies to avail ‘SLQ’ as the go-to platform to assess credit worthiness of mass India.

There are millions across the country who have never obtained a bank loan, however, they are internet users who shop on line, have a good social media presence, have a stable residential status and also have been using their mobile phones actively. SLQ will now use these factors or data points into consideration when assessing a customer’s creditworthiness.

The platform will analyze unstructured data from various sources – social media profiles, mobile data, KYC documents – to provide the users with a system that will instantaneously and continuously update a borrower’s credit worthiness and insure sound underwriting.

The scores are generated in Real Time and will enable the customer to know, within a few seconds, if he qualifies for a loan with CASHe or not. Subsequently, on completion of the loan application process, every customer’s personal SLQ score will now be displayed to him. This will provide the user with a reliable tool for accessing his/her creditworthiness.

This is a service that is sorely needed by many Indians. SLQ is developed using proprietary deep learning and artificial intelligence technologies that will analyze a wealth of data to find recurring patterns of credit behavior that will indicate an individual’s willingness and ability to pay his financial obligations.

CASHe, over the past two years have built a very large data set of customer information based on their digital footprint and mobile data to spur the financial inclusion of many deserving credit worthy Indians who do not have access to financial services. This allows us to build credit scores even for individuals with little or no formal credit information but who may actually be good candidates to obtain credit.

With more than 2 million downloads, 180,000 customers, 480 crore loan disbursals, 30,000 loans processed in a month, over 1000 loan applications in a day and 75% repeat customers CASHe has amassed a huge wealth of data encompassing rich customer information which can be potentially analyzed for credit behaviour.

About CASHe

CASHe is India’s most preferred digital lending company for young salaried millennials. CASHe provides immediate short-term personal loans to young professionals based on their social profile, merit and earning potential using its proprietary algorithm based machine learning platform. In April 2016, Aeries Financial Technologies Pvt. Ltd, launched its innovative technology-driven lending platform for the young, urban millennials. CASHe provides almost instantaneous loans on-demand. Its user-friendly digital interface enables faster loan application process and quicker loan disbursal’s. CASHe provides hassle-free loans with its app enabled documentation and loan disbursal/repayment process. For more information, please visit CASHe

METRO Cash & Carry, India’s largest organized wholesale and food specialist announced an exclusive partnership with the technology start-up Chqbook to offer a wide range of financial products and solutions to METRO’s above 3 million transacting customer base across its 25 wholesale stores in the country. In line with its commitment to be a ‘Champion for Independent Business’, METRO has partnered with Chqbook to provide inclusive financial solutions to all small and medium-sized enterprises [SMEs] within the METRO eco-system. The initiative will give SMEs access to best rates, lower fees, and more cashback on credit & debit cards with exceptional customer service.

Commenting on the strategic alliance, Arvind Mediratta, MD & CEO, METRO Cash & Carry India said

At METRO, we are committed to deliver tremendous value to our SME and Kirana value chain. The Indian Government has paved the way for a Digital India through its numerous initiatives and schemes for SMEs. Our partnership with Chqbook.com will provide a large financial marketplace to our 3 million customer base.

It has been our constant endeavor to deliver the best technological and financial support to SMEs to augment the efficiency of their business operations. This partnership is aligned with our mission statement of being a ‘Champion for Independent Business’ as we firmly believe that we are an integral part of their growth and success story in India.

Chqbook’s marketplace will provide financial services to METRO customers in the B2B sector exclusively. It brings competitive rates and fees from 40+ Banks, NBFC’s and Credit Card companies, allowing easier comparisons, instant eligibility checks and quick approvals. It also operates a network of 400+ experts across 15+ cities in the country to provide appointments within 4 hours for document pickups and same day or next day approval for loans & credit cards. Chqbook.com will work with banks and payment providers to bring cash-backs, zero EMI products and pay-later schemes, making purchasing at Metro seamless and helping SME’s and others save financing costs.

Chqbook.com will also offer pre–approved products for METRO customers across Home Loans, Business Loans, Personal Loans, Insurance, Credit Cards, and other Financial Services. It’s recommendation algorithm automatically suggests the right products between various categories, giving customers instant approval, paperless documentation and a digital on–boarding experience resulting in quick disbursals and issuance.

Speaking about the initiative, Vipul Sharma, MD & CEO of Chqbook.com, said

We found a synergy in METRO and Chqbook.com’s approach of unlocking customer value through marketplaces. Our technology, understanding of the financial services sector and our deep commitment to customer service are the cornerstone to create a world class financial service platform. With METRO, we have found a partner who champions the cause of independent businesses similar to our own mission.

This alliance will help both existing and new customers as they will benefit from the cashback programs, personal finance, insurance and a range of products & solutions that Chqbook.com is offering. We are very excited about this partnership and are enthused to work with METRO to bring more innovations and solutions to the evolving SME universe.

About Chqbook

Chqbook is India’s largest market place for AI based personalized financial services. It’s the winner of the SuperStartup Asia 2018 award and currently has over 35+ credit cards, 21 Home Loan providers and 17 Personal loan and Business loan providers listed on it’s platform. Chqbook.com uses it’s proprietary TARA AI journey which provides customers instant and personalized recommendations of products best suited to their credit score, profile and demographics.

It also pulls in data from card issuers, banks and credit bureaus to fine-tune recommendations in real time. Chqbook.com has built the next generation marketplace and provides comparisons, eligibility and a seamless application process across 40 banks and credit card companies. It’s rapidly expanding marketplace brings pre-approved loans, credit cards, insurance and mutual funds to the country’s gen next with a sharp focus on a magical customer experience each and every time. For further information, log on to Chqbook.com

Fin-tech is having a huge impact on the financial services in India. It has been largely dominated by the lending and payments companies in India. Initiatives like the India Stack [UPI, e-KYC, Aadhar] by National Payments Corporation Of India [NPCI] have been instrumental in leading the Fin-tech revolution. As of 2018, it has been estimated that India has around 19 crore adults without a bank account despite efforts from the government. Digital payments is a rapidly growing sector in India today with multiple players capturing various pockets of the market.

In this dynamic space, MoneyOnMobile brings to the table a unique and revolutionary concept of Digital payments for the unbanked and under-banked through means of financial inclusion and self-dependence.

MoneyOnMobile helps these consumers to successfully adopt digital payment practices through use of just a basic feature phone to make life simpler and easier. Users can simply convert physical cash to digital cash by visiting any MoneyOnMobile retailer base store or by activating services through a SMS or by downloading the MoneyOnMobile app.

MoneyOnMobile has been designed to work across all mobile phone handsets, from the most basic to the most advanced. By using the innovative m-Wallet from MoneyOnMobile, one can recharge a mobile; pay utility bills; top-up a DTH account; shop for any goods or services; buy travel related services such as – rail/air/bus/movie tickets and even handle banking transactions – all from the comfort of a mobile phone. MoneyOnMoney’s success to reach the remotest parts of India makes them the standalone prepaid instrument in the market today. Today we have a chat with Mr. Harold Montgomery, CEO – MoneyOnMobile about the MoneyOnMobile retailer eco-system, Fintech enablement, Digital India, etc. so let’s get started with the Q&A…

Can you walk us through the MoneyOnMobile – company, services, etc.

MoneyOnMobile is one of India’s largest mobile phone-based payment provider in India catering to the unbanked and under-banked population. We primarily operate through a well-connected network of distributors and retailers who are enabled with semi-closed payment instruments or pre-paid wallets to offer various financial services.

MoneyOnMobile offers a vast range of services including money transfer, bill payment, MOM Cart, MOM Capital, DTH payment, mobile recharge, travel tickets, two-wheeler insurance, etc. MOM ATM is another innovative solution that is worth a mention – it is a mobile point of sale device that enables brick and mortar stores or any existing MoneyOnMobile channel partner to facilitate cash withdrawals to customers by swiping their debit/ATM cards.

These services are offered on real time basis irrespective of geography, time and mobile operator within the country. The dynamic services of MoneyOnMobile can be activated through a simple SMS, APP or web portal.

MoneyOnMobile is headquartered in Mumbai in India and Dallas in the US. I am based in the US along with Scott Arey – CFO and Will Dawson – COO. You can more details about it here.

There is a lot of push for Digital India and there is a major competition with different PSP’s like PayTm, PhonePe, including BHIMP from NPCI, what are some of the core differentiators of MoneyOnMobile vis-a-vis other PSP’s since most of them provide plethora of services like Mobile/DTH recharge, Money Transfer, Bus Booking, etc.

Today the top Payment Service Providers [PSP] present in the Indian market deal with cashless transactions. Their target audience primarily have active bank accounts and other necessary means like a network enabled smartphone. MoneyOnMobile however caters to the under-banked and unbanked population who deal with physical cash on daily basis.

Through us, customers can access online services by just walking up to a MoneyOnMobile enabled retailer store requesting for payment of bills, DTH services, travel booking, etc. and pay for products and services through physical cash. The retailer collects cash from the customer to complete the process by pushing notification to the customer’s mobile phone by means of a SMS – thereby also earning a small commission in the process.

Moreover, MoneyOnMobile has the capacity to handle low value transactions which opens up to a wider range of transaction opportunities for under-banked customers whose monthly income can be anywhere between 400-500 dollars or less. This is a huge disrupting factor vis-a-vis other players. MoneyOnMobile has also involved a low-cost processing approach that bypasses direct integration with banks or card networks; APIs is used to connect digitally with third parties. This reduces the cost and saves time which is essential for most customers. Check links 1 & 2 for reference.

Mr. Harold Montgomery, CEO – MoneyOnMobile

As MoneyOnMobile is mainly targeting the unbanked/BOP population, please comment on the market share of MoneyOnMobile in the digital payments [and services sector] and where does MoneyOnMobile team see the next level of growth in a diversified country like India ?

Since inception, MoneyOnMobile has signed up more than 350,000 retailers across 900 cities all over India. More than 2-billion-dollar worth of transaction has taken place on behalf of 200 million Indian consumers with unique Indian phone numbers till date.

MoneyOnMobile caters to 600-800 million unbanked and under-banked population in comparison with other PSP players who cater to the remaining 200 million with active bank accounts. MoneyOnMobile plans to offer loans to shop owners via third parties and focus more on financial remittances sent within and outside India. Our more ambitious goal going forward is establishing 30,000 biometric-based MOM ATM systems by end of 2019 to support fee-based cash withdrawals throughout India. Refer this for more information.

There is a major push by the GOI for bringing more people under the banking umbrella, how does this shift affect MoneyOnMobile’s game play/growth plan and how does MoneyOnMobile plan to offer services if major population becomes banked ?

A recent World Bank report stated that around 19 crore adults do not have a bank account in India despite efforts from the Indian Government. Almost 50 percent of bank accounts under various schemes remained inactive in the past year, owing to different factors including poor accessibility to banks, inadequate financial literacy and non-existent of a robust network infrastructure in the country. Moreover, currency circulation had returned to near pre- demonetization levels as indicated from an analysis of credit and debit card usage in the previous financial year.

All this indicates that concept of physical cash transaction is not going anywhere despite bringing more people under the banking umbrella. India’s cash problem must be addressed at a much deeper level, this is an area MoneyOnMobile focuses to thrive and grow. MoneyOnMobile continues its effort to bring more retailers from the remotest parts of the country under its umbrella. In parallel, we also plan to diversify our service offerings, improve efficiency of transactions and add more MOM ATMs. More here, here and here.

Apart from customer experience, what are some of the advantages for a MoneyOnMobile AGENT in terms of commission, services, etc. so that he can recommend MoneyOnMobile over other PSP’s

MoneyOnMobile’s retailer assisted mobile payments model is structured to reward every member in the ecosystem – distributors, merchants and retailers in this case.

Distributor agents typically scout and sign up retailers to enable MoneyOnMobile services. Every agent earns an incentive based on total payments volume each store/retailer under him/her generates. This acts as a great motivator for more distributors to register retailers who can bring in strong traffic in the area. Distributors are also encouraged to provide training and support to retailers who instill strong support system to grow.

Retailers earn through transaction based commission, once the retailer accepts cash from a consumer and directs the funds to the respective payee, the merchant gets a percentage of the profit gained from the transaction. MoneyOnMobile’s business model ensures all stakeholders involved in the network are benefitted from each transaction and this has helped in registering more than 350,000 retailers throughout India. More details can be found here.

Though Demonetization happened in 2016, it had a major impact on all the sectors, but it resulted in a huge push in Digital Payments, how much growth in volumes did MoneyOnMobile observe during that phase and how did you keep the users hooked after that exponential growth phase ?

Demonetization had a different impact on MoneyOnMobile. While it had given adequate boost to the growth of digital payment apps and wallets, MoneyOnMobile witnessed a slight decline due to shortage of cash, which is core to our business. But on longer, demonetization succeeded in boosting growth of digital transaction and adoption of digital payment methods in semi urban and rural areas. Eventually with cash returning back to the system coupled with consumer trust and understanding of the importance in digital remittances, we have witnessed considerable growth post demonetization.

The key attraction for retailers and consumers to continue using MoneyOnMobile is the combination of bringing different services to a single location that will help people save tremendous amount of time & money. Another is the cost of investment to use MoneyOnMobile; the fact that consumers need only a simple mobile phone to use these services is a huge plus factor. More here and here.

We thank Mr. Harold Montgomery, CEO – MoneyOnMobile for sharing his insights with our readers. If you are retailer and planning to join the ever expanding MoneyOnMobile network, please download the MoneyOnMobile Retailer Prima from here. MoneyOnMobile Wallet for consumers can be downloaded from here. If you have any questions for Mr. Harold or his team, please email them here or share them via a comment to this article.