Synechron, a global financial services consulting and technology services provider have announced the launch of two new, state-of-the-art digital innovation labs in Pune and Bengaluru to advance global, digital transformation initiatives for the financial services industry.

Synechron’s Financial Innovation Labs [FinLabs] act as an innovation hub that enables businesses to experience first-hand the latest digital technologies from blockchain and artificial intelligence, to voice recognition, drones and others to look at, touch and ‘feel’ real-world business solutions and advance fintech initiatives.

With Pune and Bengaluru FinLabs open to the industry and another new facility coming up in Hyderabad shortly, Synechron now has 8 FinLabs globally, with other labs located in London, Amsterdam, Dubai, Charlotte and Fort Lauderdale. Synechron also plans to roll out a flagship FinLab in its New York HQ, in the coming months.

The India FinLabs in Pune and Bengaluru are fully operational as of now and are open to Synechron clients to experience the latest digital technologies and be energized and inspired to develop transformative solutions.

Visitors can do everything, from role playing the customer journey through a typical digital engagement scenario to prototyping around new technologies, applications and accelerators including:

Artificial intelligence, robotics, machine learning and data science

Blockchain applications using Ethereum, Hyperledger and Ripple

Data analytics and visualizations

Drones

Gamification models

Tablets, beacons, biometrics and mobile applications

Virtual reality and augmented reality

Voice recognition and natural language processing via Amazon Echo and Siri

Additionally, Synechron’s India FinLabs have introduced an interactive video wall for data visualization, recognizing that user experience [UX] is the key to customer engagement and a centerpiece for the bank branch of the future.

Our vision for FinLabs was to create more than just a trendy collaboration space. Synechron has taken the innovation lab model to the next level by creating a truly immersive technology experience that fosters development of real business applications like our blockchain accelerators while supporting FinTech innovation. Pune, Bengaluru and Hyderabad are leading technology markets, and as we look to cultivate top tech talent and serve our clients, we are delighted to deliver this unique value.

David Horton, Managing Director and Head of Innovation at Synechron added

The financial services industry wants to embrace cutting-edge technology to advance business strategies. Each of the technologies we are featuring in FinLabs can help address key issues like regulation, cost pressure, efficiency, customer experience and engagement to deliver digital banking and achieve fintech’s promise of disruptive innovation that simplifies our world, and makes banking better.

Synechron, one of the fastest-growing digital, business consulting & technology services providers, is a USD 400 million firm based in New York. Since inception in 2001, Synechron has been on a steep growth trajectory. For more information, please visit Synechron

Jeet Suri does not own a credit card. He does, however own an apartment in Bangalore. It is almost bare, save for his furnished bedroom and modular kitchen. Considering the hefty furniture costs, he knows that he will need to avail of a personal loan to get his apartment fully furnished. But this is easier said than done! As a 24-year-old IT professional in a medium-sized IT firm, he has been denied personal loans twice in the past for not having the requisite Credit [or CIBIL] Score.

Image Source – Alternate Lending

Jeet has now made the decision to apply for a loan from one of the new Fintech startups that specialize in giving quick personal loans to salaried people. He applies, gets his approval within 2 hours and funds reach his account in 48 hours! Jeet himself is surprised at the smooth and quick process. And this is exactly what attracted numerous alternative lenders in the country to start online lending platforms, albeit at somewhat higher interest rates.

The Indian Banking Sector has quite a history of bad loans and non-performing properties that has made lenders [particularly public sector ones] more cautious and conventional. There are more than 1.5 million companies in the country, but banks tend to focus on lending to only to those salaried applicants working for less than 50,000 companies which are listed in their target databases. So where do the rest go for loans? This explains the rise of close to 100 alternate lenders in India in the last two years alone [India has the 3rd largest number of personal lending startups in the world, after China and the USA!].

This new breed of lenders can be broadly categorized as follows

Aggregators or Lead-Generators

Aggregators are solely responsible for generating a lead and passing it on to one, or more, banks. This is a commission-based task and they earn a fee per lead, regardless of whether the loan is approved [and eventually funded] or not. The decision to lend lies with the bank or the non-bank lender, who makes the final credit decision on the case. BankBazaar and PaisaBazaar are two notable names in this niche.

Direct Selling Agents [or DSAs]

DSAs do everything the aggregators do and some more. Aside from lead generation, they take care of the entire documentation process too, hereby assisting you in ensuring that your loan is approved. Here, too, the credit decision lies with the ultimate lender [a bank or a non-bank lender]. DSAs charge a fee to the lender, which typically ranges from ranging from 1.5 to 3 percent of the loan amount. Finance Buddha and Finwizz are two notable names.

Infographic Courtesy – Qbera

Consumer Durable Financing Marketplaces

Increased income, soaring consumer aspirations and easy cash access have prompted a sturdy growth in big-ticket purchases like electronics goods and furniture. Of the numerous schemes that have developed to fund these acquisitions, zero-interest EMIs and cardless EMIs are the most common. Astonishingly, in India, more than half of such purchases are made possible using small ticket loans from non-bank lenders! Here too, the lenders make the ultimate decision on the customer, and the platforms typically earn a commission or some sort of revenue share.

Business Correspondents

Business Correspondents take ownership of the entire life-cycle of the loan, from acquiring the customer, underwriting the loan, documentation, verification and ensuring the final loan is disbursed. The loans are funded by one of more lending partners and, uniquely, the platform plays a role in making the credit decision. They are not middleman, as they usually share risk [as well as revenues] with the bank or non-bank lending partner. Qbera is one such startup that is operating on this model

Summing it up

The online lending landscape in India is evolving rapidly. New-age online lenders are giving the incumbents a run for their money, as they partner with a variety of capital providers to test segments which have previously been untapped. Added to this, they provide a superior customer experience, which includes more transparency, a better approval rate, a convenient process and lower turn-around times. However, time will tell how many of these new-age lenders will be able to target new, profitable segments, whilst scaling their businesses with low(er)-cost capital, and do all this while maintaining the quality of their portfolio.

About the author

Nidaa Chakkittammal is a Proud feminist, former journalist, certified mountaineer and currently Content Manager at Qbera. She believes self-discovery is an eternal journey. When she isn’t drafting finance articles and blogs by the dozen for Qbera & other similar platforms, she is busy reading romantic poetry and fiction, rollerskating, participating in marathons, cycling, chilling with friends and trekking. You can find more about her on her LinkedIn profile page.

Few weeks back, we reviewed MoneyTap which is India’s first app based credit line. You can find the MoneyTap review here. As mentioned in the review, MoneyTap offers unsecured loans for salaried professionals in association with its partner banks.

Unlike P2P lending companies, the interest rate is much lesser and the loan process is fast & simple 🙂 Today we have a chat with Bala Parthasarathy, Co-founder & CEO of MoneyTap about MoneyTap, the P2P lending market, opportunities in Fintech, impact of Digital India & much more. So let’s get started with the Q&A….

How did you come up with the idea of MoneyTap ?

It was a combination of personal experiences as well as general observation. Growing up in India in the 80’s & 90’s and coming from middle-income group families, we have all faced shortage of additional funds at some point. We observed the market need and realised that the middle income group [the salaried class] has always been facing challenges with respect to credits, especially small amounts. People are not comfortable going to banks for loans for minimal amounts-this could be anywhere from Rs. 3000 to Rs.50,000 to 1 or 2 Lakhs.

Asking for money from family and friends always has an embarrassment factor. The needs are what most of us have, that could be anything from medical, birth, death, school fees, deposit to take a rent on house, etc. In many cases, people even have fixed deposits that they just don’t want to break for a small need. This is where we thought of MoneyTap and wanted to be like a friend who could be reached out at fingertips.

At MoneyTap, we are on a mission to change this and make credit accessible to those who deserve it. The ubiquitous presence of smartphones and initiatives such as Aadhaar has made it possible for us to develop a truly powerful and disruptive financial instrument. The credit line for consumers with accessibility through an app is a new concept in India and we are excited about the opportunities it can bring to thousands of millions of Indians. MoneyTap is like a friend who gives you money when in need, be it marriage, birth sudden death in family, school fees, hospital bills or sudden cash crunch during the month end. We, at MoneyTap, want to make credit available for deserving and eligible candidates.

Can you share some details about the team behind MoneyTap ?

MoneyTap is based in Bengaluru and all the three of us have been entrepreneurs before with an IIT/ISB background. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and USD 300M in revenue. After moving to India in 2007, he volunteered for UIDAI under Mr. Nandan Nilekani before starting AngelPrime in 2011 [now Prime Venture Partners] where he helped create companies like ZipDial [sold to Twitter], EZETap, Happay, etc.

Kunal [ex Texas Instruments] & Anuj [ex Airtel & JWT] co-founded Tapstart that grew to 300K users and turned profitable in 2 years. They exited this venture in 2015.

What is the TAM of the consumer debt market that MoneyTap is trying to address ?

Consumer debt is growing fast in India. According to the last available consolidated data from the Reserve Bank of India [RBI], personal loans – extended by banks grew at 28.7% in 2015 and credit cards grew at 23.6%. But if we look at the actual numbers, there are just 24 million credit cards for a country of 1.2 billion! Middle income customers making Rs. 25,000 per month or more, facing frequent cash crunch for regular needs like education, medical, birth/death, etc. are not serviced by financial institutions today without putting up collateral such as gold.

Large needs, such as buying a vehicle, house, etc. are addressed by financial institutions unlike online and offline shopping. Though the latter often involves very high credit card interest rates of 40% if one doesn’t pay on time. This is the clear unaddressed need.

How different is lending based on Line Of Credit vis-a-vis P2P Lending or taking a loan [any type of loan, personal/housing/education,etc.]

We see the following major differences

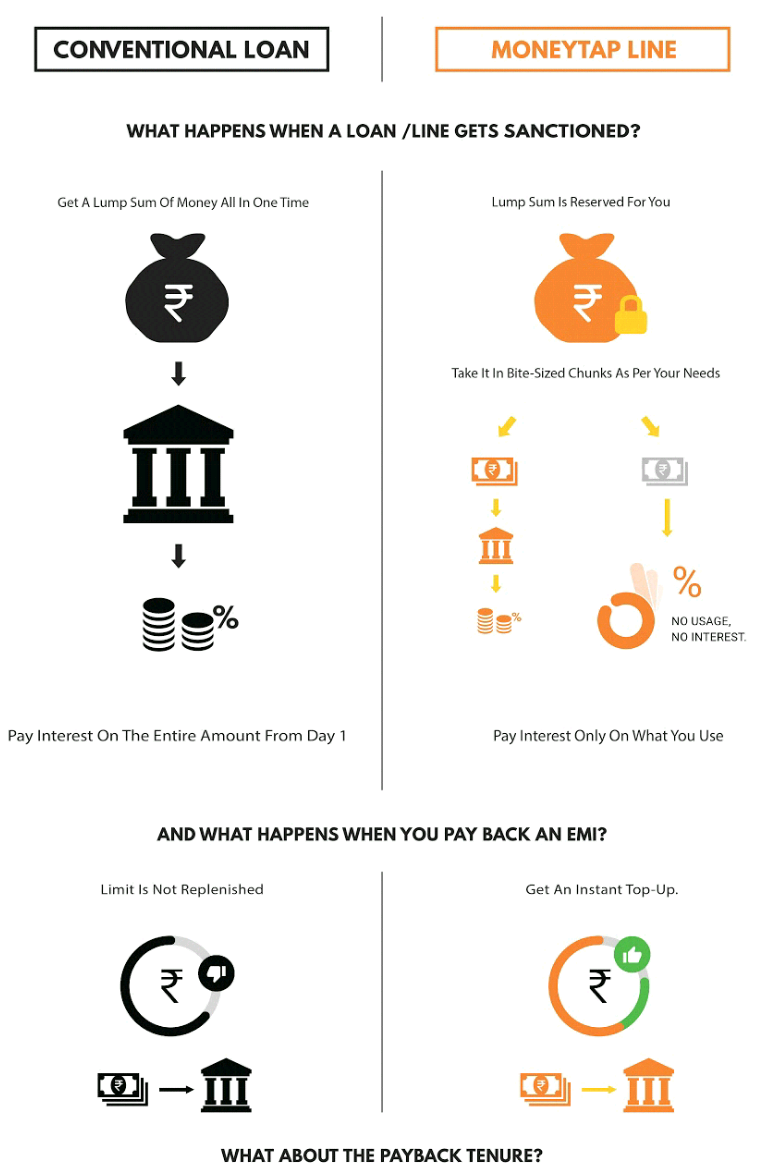

1. Once a credit line is sanctioned with an upper limit, one can decide any amount of money from that limit and choose to withdraw only that specific sum from the credit line. So, if there’s an approved credit line of say Rs. 3 Lakh, one could withdraw a small amount like Rs. 5,000 or Rs. 50,000 and so on.

In contrast, a typical personal loan would force one to take the entire Rs. 3 Lakh in one shot, even though the need for money is spread over a period of time.

2. Interest would be charged only on the small amounts borrowed and not on the full Rs. 3 Lakh. Thus, if amounts of Rs. 5,000 and Rs. 50,000 are borrowed separately, then one would only have to pay interest on the total of Rs. 55,000 and not on the entire amount of Rs. 3 Lakh sum. This would have made a world of difference to a person’s monthly cash flows and overall financial condition.

The obvious contrast with a typical loan is that interest would be charged on the full Rs. 3 Lakh amount from day one. Usually a person has no choice in this scenario.

3. In most cases, the flexible borrowing options in a credit line come with the convenience of deciding payback periods for the separately borrowed amounts. Thus, for an amount of Rs. 5,000 borrowed from the credit line, one could choose to repay in 2 months and pick a longer tenure for the amount of Rs. 50,000, say anywhere between 12 months.

In contrast, a personal loan tenure would be fixed upfront with little or no flexibility in most cases. The advantage of a credit line is that as soon as EMIs are paid back, the credit line gets replenished automatically and one can continue the cycle of borrowing and repayments without needing to apply gain.

The infographic also explains how a credit line differs from a conventional loan:

What are some of the data points that MoneyTap uses in order to check whether an individual is creditworthy to be approved as a borrower on MoneyTap ?

Firstly, an individual needs to qualify the MoneyTap eligibility criteria mentioned below:

23 years and above age

Salaried individuals with minimum salary of 20,000 pm.

Credible KYC documents

Residents of Delhi, NCR, Mumbai, Bangalore, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara and Bharuch [will be launching in other cities soon]

Secondly, our partner bank check the creditworthiness of the applicant based on their credit history and thereby the applicant is approved/ disapproved basis all the steps. Once approved, their credit limit is set according to their credit history.

Few years back, there was huge wave about MFI’s (like SKS Microfinance), in 2016~17 the wave is around fin-tech sector (NBFC’s), what are your thoughts about the Fintech space in the coming years ?

Fintech will see significant growth and innovation in the next few years. Innovations like IndiaStack and deregulation in the form of GSTN, payment bank licenses and demonetisation along with a massive governmental push to move payments to digital will spur a significant growth in multiple areas in finance.

[L to R] MoneyTap founders – Kunal Verma, Anuj Kacker and Bala Parthasarathy

There is a general question with borrower, what happens if they are unable to pay an EMI on time/not able to return the money. How is the lingering question of Credit Risk taken care of ?

The same consequences of not paying one’s credit card bill or bank loans apply in this case as well. The Reserve Bank of India has nominated 4 credit agencies [e.g. CIBIL] that track an individual’s financial credit scores. If one does not repay or delay the repayment, our partner bank will automatically report it to these agencies, which will record the information. This can lower the borrower’s credit score.

Once an individual’s credit score is affected, they will not only lose MoneyTap access, but all future loan applications will be negatively impacted. He might not be able to get loans easily to buy a house, a car or a two-wheeler or get a credit-card, as all the lending institutions in the country check with these agencies before approving any loan. The bank might also initiate legal recourse to recover the money from the individual.

Can you please share some insights into the min/max loan that a person can avail on MoneyTap, interest rates, pre-closure charges, association with RBL Bank and any other details that would come in the mind of a personal availing a short-term credit

MoneyTap enables consumers to get instant credit from partner banks at the tap of a button on the app. Credit Line, a facility that was only available for businesses until now, is now being made available to consumers. The ‘Credit Line’ means that the bank will issue a limit of up to INR 5 lakhs, without any collateral or charging any interest. Against this limit, using the MoneyTap app, consumers can borrow as little as Rs. 3000 or as much as Rs. 5 lakhs and repay it as EMIs from 2 months to 3 years. The interest is paid only on the amount borrowed and the rates can be as low as 1.25% per month. The limit also gets automatically replenished as soon EMIs are paid back.

Any salaried employee can download this free Android app and in a few minutes, using a patent-pending Chatbot interface, provide all the information typically required by banks. The app securely connects with the banking systems to give them not only an instant approval but also a credit limit, depending on individual credit history.

The RBL Bank is the launch bank partner of MoneyTap. RBL’s technology enables MoneyTap to provide instant decision and instant access to money, 24/7, irrespective of holidays. Though all actions are initiated on the MoneyTap app, per RBI guidelines, all financial transactions such as billing, repayment or withdrawals will directly be with the bank using secure APIs.

As an added convenience for shopping needs, a ‘MoneyTap RBL Credit Card‘ is also provided for the user. This is a regular MasterCard Credit Card that is accepted at all locations and for all card purchases – offline and online.

According to your data, which is the biggest category where customers have opted for loan based on Line of Credit/MoneyTap ?

Our Top-3 categories are Wedding spends, Household related purchases and Education.

Currently MoneyTap is available only for working professionals, any time-line or plan on when you plan to open up this avenue for entrepreneurs, SMB’s, freelancers, etc.

As of now our only target is to expand our customer base among the salaried class. We have lowered the minimum salary limit for eligibility from Rs. 25,000 per month to Rs. 20,000 per month. MoneyTap now is also available for people staying in shared accommodations.

Normally Banks & other financial institutions take couple of days~weeks for KYC, how does technology [behind MoneyTap] ensure that the entire process of validation of credit-worthiness of an individual is expedited ?

The first step in our evaluation process is to understand the person’s credit profile. We are able to do this under 7-minutes on the MoneyTap app that you can download for free from the PlayStore. After that, qualified applicants who have their Aadhaar card and updated mobile number with Aadhaar, can eSign their documents so that absolutely no paperwork is required.

We are able to do this because of our advanced technology as well as the increasing adoption of Aadhaar and IndiaStack.

MoneyTap is currently present in how many cities in India ?

MoneyTap is currently present in Bangalore, Delhi, NCR, Mumbai, Hyderabad, Chennai, Pune, Ahmedabad, Vadodara, Gandhinagar, Anand and Bharuch.

Are there are any RBI guidelines regulating the app based businesses [based on Line Of Credit] in India or to put it the other way round, is there a requirement to regulate lending based on Line Of Credit in India ?

Lending, whether they’re on an app, website or physical branches is regulated in the exact same way. There must be a bank or NBFC that meets all of RBI criteria. MoneyTap also meets with RBI from time to time to provide inputs so that the regulators can draft appropriate policies.

What are some of the things that a borrower needs to keep in mind while opting for repeated loans on MoneyTap [or for that matter any medium offering loan based on Line Of Credit] ?

Whether it is MoneyTap or not, basic rules of finance that we learnt from our parents and grandparents apply. Borrowing money to tide over medical emergencies or invest in things like education are good. Buying and spending things beyond the ability to pay it back will always have a bad ending.

In case of Loans, interest rates vary from Bank to Bank and are also dependent on external factors like market volatility, etc. can you let us know whether the interest rates are fixed on MoneyTap or whether it is like a normal loan [where for certain number of years interest rate is fixed and later it is variable] ?

A borrower has to pay interest only on the funds he uses. At the time of withdrawal, he can choose the terms of repayment, which can be anywhere between 2 months and 3 years. The repayment tenure he chooses will determine the EMIs.

The interest rate is equivalent to market rates for any ‘personal loan’ with zero collateral or security. It can be as low as 1.25% per month depending on the partner bank and the credit profile of the user.

Who are some of the competitors of MoneyTap ?

MoneyTap is the first credit line app in India. Until now the concept of credit line was present for traders through money lenders. We have introduced the concept for consumers for the first time. There is no competition that we see at present.

2016 was a tough year for startups [especially from funding point of view], how according to you should entrepreneurs deal with such adverse situations ?

Grin and bear it. Markets are always cyclical and the sky high valuations backed by even higher expectations were bound to come back to earth sooner or later. This is actually a great time to get excellent talent who are not overpaid and build great businesses.

Can you share some tips for building an effective team for startups [especially the initial core team].

There are three big rules:

Hire very, very smart people. You can’t substitute intellectual horsepower with anything else. And give them a lot of autonomy.

Smart people are rarely easy to work with. The ‘brains-premium’ is worth paying, up to a point.

If and when they get disruptive or if you made a mistake in hiring, quickly let them go. It’s better for both parties in the long term.

How important is it for early stage startups to pivot their business model [in case things are not working out as per their plan] or when is the right time to pivot ?

It is critical. But the problem with Indian entrepreneurs is not in recognizing the importance of pivoting. It is the execution of a pivot. They typically just add on the new business and keep the old one. That’s a ‘khichadi’ strategy, not a pivot strategy.

After demonetisation, there has been a huge demand for payment apps [including UPI], do you see that trend working in favour of apps like MoneyTap [that offer different services compared to e-wallet apps].

Absolutely. We are not a merchant or consumer UPI app like others. We are in the business of providing credit. UPI is a terrific way for our customers to take money out and pay back without the hassle of net-banking, etc.

Bala’s earlier venture Snapfish was acquired by HP, what according to you should entrepreneurs look for when there is interest [from other companies] for their startup getting acquired [and not acqui-hired].

Again, there are three rules for selling your company:

Good companies are bought, not sold. In other words, if you are actively out there selling your company, you will have to settle for peanuts.

You should always have multiple parties engaged, not just have one buyer.

Sell on a high note-when the company is doing great, potential buyers will extrapolate to value your company at an even more glorious future.

As per your entrepreneurial experience, when should an entrepreneur look out for external funding ?

When they really don’t need the money. It’s always the best time!

Some books that you highly recommend for entrepreneurs

There are lots of good books. The two I recommend are, ‘Zero to One’ by Peter Thiel and ‘Hard things about Hard Things’ by Ben Horowitz.

Some closing thoughts for our readers!

Entrepreneurship is not easy and not for everyone. But it is addictive and some of the most creative moments in your life will be during this journey. And there is no other [legal] way to have a huge financial windfall besides running your own company.

We thank Mr Bala for his time and sharing valuable insights with our readers! If you have any questions for Bala about MoneyTap, Fintech, scaling up, etc., please email them to himanshu.sheth@gmail.com or leave your question in the comments section.

Synechron Inc. [earlier coverage here] a global financial services consulting and technology services provider, has today announced the launch of Neo, aset of Artificial Intelligence [AI]-based solutions for the financial services industry. Neo brings together Synechron’s digital, business, and technology consulting to allow financial institutions to deploy cutting-edge, AI solutions that solve complex business challenges.

Synechron has built 14 reusable applications – Accelerators, that allow financial institutions to reduce time-to-market when applying AI to enhance business operations, reduce operating costs, and create better client experiences.

Synechron’s AI Accelerator applications have taken a business challenge that can be best solved through AI and re-designed business processes to build a solution powered by artificial intelligence and optimized for user experience. The Accelerators use techniques like Natural Language Processing [NLP], Chatbots, Robotic Process Automation [RPA], Cognitive Machine Learning, Data Science and Robo-Advisors to address a range of use cases.

The AI Accelerators enable financial industry players to solve complex data challenges, efficiently address regulatory and compliance requirements, and service growing customer needs. They also help automate repetitive processing tasks while cutting down time and costs in the long run, with customized and advanced bots for specialized operations such as trading, mortgages, insurance, and even personal banking.

Details of the various accelerators are below

The AI Accelerators broken down by the core underlying AI technology include:

Natural Language Processing (NLP) and Generation [NLG]

Automated Data Extraction allows firms to automatically extract written language data from reports [e.g. earnings reports] and understand what it means and why it’s significant [e.g. its intent] Automated Financial Advice Generation can be achieved to extract CRM data and NLG to reach a compliant conclusion through real-time queries and contextual user information. Automated Executive Summaries written in plain language.

Chatbots serve as either an internal virtual assistant or a front-line customer representative and have been created with an understanding of financial services business operations and systems integration expertise. The accelerators include – BankBOT for personal banking, TraderBOT for traders, LoanBOT for mortgages, and InsureBOT for insurance.

Robotic Process Automation [RPA]

Client On-boarding pulls information from images of documents such as driver’s licenses and passport to auto-populate forms and create a frictionless on-boarding experience. Automated Resolution of Failures ‘Breaks’ in Reconciliation processescompletely automates general ledger [GL]reconciliation. Margin Call Management analyses emails and automatically understands relevant margin call information based on pre-set criteria. Automated Pitch-book Generation allows financial institutions to automatically generate presentation decks by understanding what content is on the slides and the appropriate disclosures required based on that information.

Cognitive Machine Learning

OTCPrice Automation – derives real-time OTC pricing for liquid OTC products where this data is currently de-centralized and difficult for traders to factor into their pricing models and further using that data to advance collateral management reporting. LCR Reporting – uses historic data and machine learning to come up with a reliable intra-day liquidity estimate for LCR reporting.

Data Science

Customer Insights has 4 Modules for Banks, Credit Cards, e-Commerce and Mortgages that allow banks to bring together their Know Your Customer (KYC), Banking, and Credit Card Data into a database, and join them with the customer’s online behavior (if opts in) via web and social platforms. Product Recommendation uses behavioral analysis to understand customer patterns for new client acquisition. AML/Fraud Detection uses AI and behavioral analysis to identify potentially suspicious activity indicative of money laundering and fraud.

Artificial Intelligence Accelerator for Robo-Advisors – allows wealth managers to create a hybrid-robo-advisor that augments their existing services with an automated platform, creating the self-service experience clients are looking for, balanced with the high-touch, high-trust experience advisors are known to deliver with added capabilities like social investing, chat and more.

Financial institutions are looking to implement the latest technology to address real-world problems in financial services. Neo and Synechron’s AI Accelerators will be pivotal in helping clients be at the forefront of technological advancement, while providing a comprehensive set of tools to ease and streamline processes. This will allow businesses to deploy technology-enabled processes that augment the role of individuals, allowing them to be elevated to higher-value business tasks.

The AI engine, business, and technical analysis at the core of these accelerators can be applied to additional use cases to progress more quickly with similar initiatives. Along with the use of the AI applications, the Accelerator Program offers access to Synechron’s consultants, technologists and digital teams who are experts in financial services business processes, products, regulation, operating models and data architectures which are critical to constructing effective AI applications.

About Synechron

Synechron, one of the fastest-growing digital, business consulting & technology services providers, is a USD 400 million firm based in New York. Since inception in 2001, Synechron has been on a steep growth trajectory. For more information, please visit Synechron

Aeries Financial Technologies Pvt. Ltd, a fin-tech company promoted by serial entrepreneur and private equity investor V. Raman Kumar, announced that CASHe, India’s fastest loan giving app for young salaried professionals, has entered a strategic partnership with Rubique, India’s leading online marketplace for financial products.

In this collaboration, Rubique will enlist CASHe on its online platform for borrowers to avail viable short-term loan products from CASHe. CASHe disburses multiple loan products ranging from Rs 5,000 to Rs 1,00,000 payable over 15, 30 & 90 days. CASHe now disburses loans well over 1 Crore per day in less than a year of operations. With an average loan processing crossing 500 loan applications per day, CASHe is now India’s leading and most preferred fintech company in the personal lending space.

V. Raman Kumar, Chairman, Aeries Financial Technologies said

We are thrilled to partner with Rubique, India’s leading fintech company in marketplace lending. Rubique’s online platform with its unique matchmaking algorithm is an industry first, and with CASHe now being enlisted on its platform, the prospective borrowers will now have access to CASHe’s short-term loan products available through its app. The application will be directly integrated to Rubique’s platform for the users to download and avail a loan within minutes on their smartphone. Rubique’s large customer base will now have access to quick and easy credit without any collateral, physical documentation or verification. This indeed will be an exciting proposition for young salaried professionals. With our strategic partnership with Rubique, we hope to increase our customer base exponentially.

Partnering with a fintech product like CASHe complements our business model and vision to provide easy & quick access finance to the borrowers through advanced technology. We believe that for every borrower there is lender in the market. But there is no common place where both can discover each other. By creating this common platform for discovery through advanced technology, it’s our endeavour to reduce the processing time significantly. We would like to integrate with lenders with various risk appetite to ensure each of our customer find the right fit of products on our platform.

Products offered by CASHe’s unique mobile-enabled short-term loan offering is an apt solution towards growing consumer segment which demands quick loan disbursals. In terms of growth rate, both of us have witnessed impressive growth & there is absolute alignment on technology focus in the process implemented. With CASHe’s integration, we are now able to offer a wider range of personal loan products to our customers which can disbursed quickly. We are very excited to work with CASHe as we see a huge demand for a loan product offering like this which is hassle-free and convenient.

CASHe provides hassle-free loans with its app enabled documentation and loan disbursal/repayment process. Powered by its industry-first algorithm driven credit scoring platform, The Social Loan Quotient [SLQ], CASHe quickly determines a user’s credit worthiness by using multiple unique data points to arrive at a distinct credit profile of the customer.

SLQ is transforming the traditional credit rating measurements thereby providing immediate loans to the under-served young professionals who are kept out by traditional credit rating and banking systems. CASHe is completely automated and requires no personal intervention and no physical documentation. The average time taken for a loan to be disbursed is about 8 minutes, subject to proper submission of all documents.

About CASHe

CASHe, a fin-tech product of TSLC PTE. LTD., promoted by Aeries Financial Technologies is as unique as the young professionals it serves. In a smart digital world, CASHe offers millennials quick and easy personal loans through processes that are transparent, innovative and tuned to the times. CASHe utilises sophisticated algorithms and machine learning capabilities to deliver an amazing and improved lending experience to our customers, thereby helping young professionals achieve their financial goals effortlessly. CASHe app is available on Google Play and iOS app store

MoneyTap, India’s first App-Based Credit Line, has been awarded as the leading FinTech company, in the lending category, at PICUP Fintech 2017. PICUP Fintech is an event by FICCI to recognize the best innovations from Fintech companies in diverse areas like Wealthtech, Lending, Payments, Artificial Intelligence and Robotics. The event witnessed diverse groups of FinTech players, leading bankers, technology experts and policy makers. The event was organized by a joint effort of NASSCOM, FICCI, IBA and BCG in Mumbai.

Six companies from each category were shortlisted after applying for a product demonstration. MoneyTap, Faircent, Cropin SmartRisk, GraduFund, FlexiLoans, FinTechLabs were the six shortlisted companies in the Lending category. These companies presented their latest innovations and overall business to the audience and industry jury members comprising of Sunny KP-General Manager, Federal Bank, Jayant Kshirsagar-Director (Marketing), SAP and Ashish Garg-Partner, BCG. MoneyTap was the top company to be selected by the jury members’ basis the presentation and product demo.

We feel honored to be recognised as the leading FinTech company at PICUP Fintech 2017. It gives us immense pleasure to be recognised by the top officials of the industry. This recognition gives a boost to our motto of providing a convenient credit line to the middle income group of our country and making the availability of money easier and faster.

MoneyTap introduced the concept of a Credit Line [personal line of credit for consumers] for the first time in India when it launched in September 2016. The ‘Credit Line’ means that the bank will issue a limit of up to INR 5 lakhs, without any collateral or charging any interest. Against this limit, using the MoneyTap app, consumers can borrow as little as Rs. 3000 or as much as Rs. 5 lakhs and repay it as EMIs from 2 months to 3 years.

The MoneyTap app is available on Android Playstore to all salaried employees, living in Ahmedabad, Vadodara, Delhi NCR, Mumbai, Bengaluru, Pune, Hyderabad and Chennai. The company is continuously expanding across India.

About MoneyTap

MoneyTap is a Bangalore-based fintech startup, founded by serial entrepreneurs Bala Parthasarathy, Anuj Kacker & Kunal Varma, who are IIT/ISB alumni. Bala has co-founded multiple startups in Silicon Valley including Snapfish [sold to Hewlett Packard], which he helped grow to 100M users and USD 300M in revenue. MoneyTap works in very close partnerships with various banks and other financial institutions to make the process painless and on-app. For more details, please visit MoneyTap

Setting the stage for Government of Andhra Pradesh’s ambitious initiative, #SpringConference 2017 was inaugurated at Novotel, Visakhapatnam today. Fintech Valley Vizag is Government of Andhra Pradesh’s flagship initiative that brings together industry, academia and investors to innovate, co-create & build the fintech ecosystem. The Fintech Spring Conference 2017 marks the beginning of this journey.

The primary objective of the event is to explore trends and opportunities in fintech. This is a platform where the finest minds of financial and startup community get to share mind-space with thought leaders, business leaders, artists, actors, musicians, futurists and entrepreneurs.

Offering full support to organisations, incubators, facilitators and start-ups, inviting anyone with disruptive ideas to be a part of Fintech Valley, on the edge of innovation, Chief Minister of Andhra Pradesh, Nara Chandrababu Naidu interacted with delegates for an hour over video conference and took inputs from fintech community present at the Spring Conference.

He will chair The Fintech Valley Forum setup to focus on various aspects of the ecosystem creation. While addressing the gathering he said

The Fintech Valley Spring Conference is our step in joining the Fourth Industrial Revolution which is a spectacular combination of technology and Internet of Things [IoT]. In recent times, technology has started influencing our lives in a comprehensive manner. The demand for Fintech is growing each day. To meet this demand, we would need the support from Fintech and Cyber security companies. We also need the academic institutions to adapt curriculum that trains individuals to contribute to fintech sector. I extend my best wishes for the success of the initiative and hope it provides multiple opportunities to meet the futuristic requirements of our country and the global economy at large.

In his keynote address, Special Chief Secretary and IT Advisor to the AP Chief Minister, J. A. Chowdary stated

Indian IT 1.0 is facing difficulties. The next flight towards IT 2.0 will be backed by fintech. The tectonic shifts this will cause and entail is captured by the expression ‘fintectonics’. It is a fintech culture we are creating here-a culture of doing something for the betterment of the common man, a culture of creating an ecosystem by getting the right industry linkages and finding the right formula for the critical manpower.

Present on the dais were Roy Teo, Director, Fintech & Innovation Group, Monetary Authority of Singapore [MAS]; Utkarsh Palnitkar, Partner KPMG; George Inasu-COO, Fidelity Financial Services; Puneet Pushkarna, Chairman, TIE-Singapore & Joe Seunghyun Cho, Co-founder and Chairman, Marvelstone Group.

Keynote speakers at the conference

To accelerate the evolution of Fintech Valley, the Government of Andhra Pradesh [GoAP] has also initiated a fintech networking event every month, in addition to the annual fintech international flagship event. This year, on October 9-10, the government will host the Blockchain Technology International Event. The flagship Global Fintech Summit will take place on Feb 19th & 20th, 2018. This event provides the opportunity to participate in the $1 million global fintech award challenge and the INR 1 crore Indian fintech award challenge.

An invigorating Investment Panel Discussion on ‘Funding Fintech – wearing an investor’s hat‘ was moderated by P. S. Sreekanth, Investment Director, Hyderabad Angels; Sampath Iyengar, Partner, Forum Synergies; Abhinav Chaturvedi, Principal, Accel Partners; Prasad Vanga, Founder & CEO, Anthill Ventures; Utkarsh Sinha, Enterprise Technology Investor, Bitkemy Ventures; Puneet Pushkarna, Chairman, TiE-Singapore & Utkarsh Palnitkar, Partner and National Head IGS Advisory Management, KPMG. Beginning the discussion with the post demonetization scenario, the panelists sustained their dynamic dialogue in identifying fintech investment portfolios with high RoIs.

Additionally, the finalists’ demos and presentations for the ICICI Bank Start-Up Challenge & the HDFC Life Start-Up Challenge were showcased to the audience, wherein the competitors took questions from the judging panelists. Following this, another Banking Panel Discussion on Consumers and Marketplaces changing in an increasingly cashless world was moderated by Neha Punater, Partner and Head Fintech, KPMG. Key panelists Akhil Handa, Advisor to MD&CEO, Bank of Baroda; Shashi Bhushan, Managing Director, Investment Management Technology, Goldman Sachs India; Ramesh Loganathan, Professor, IIIT Hyderabad and Sudin Baraokar, Head of Innovation SBI discussed challenges faced by start-ups in being unable to identify and direct resources towards the accurate fintech problem area. They also proposed the need to create a consolidated industry-wide ‘use case’ library to facilitate innovation.

The first Fintech Valley Vizag Spring Conference brought together fintech companies, start-ups, researchers and key government officials working in the fintech sector and provided opportunities for disruptive business solutions.

The peaceful atmosphere offered by Visakhapatnam compared to other bustling tech-hubs in India, created a serene environment for igniting fintech innovation and disruption ideas at the Fintech Valley Spring Conference. Fintech Valley Vizag is rapidly becoming the epicenter of fintech disruption. Since the launch of Fintech Tower, the Andhra Pradesh government has signed numerous partnership agreements with renowned educational institutions, corporations and governments that share the state’s vision of becoming pioneers for building strong standards for fintech and mutually sharing the desire in working towards cooperative advancement through information and resource sharing.

About Fintech Valley Vizag

The Fintech Valley brings together public and private players, state of the art incubators and accelerators, innovation labs, mentorships, angel investors and anyone willing to break free from traditional processes. The self-sustained global Fintech Ecosystem provides more than just access to Fintech and its innovators; it nurtures an oasis in which cyber security, block chain, digital education and research thrive at international standards. For more information, please visit Fintech Valley Vizag

About Spring Conference 2017

Fintech Valley Vizag is Government of Andhra Pradesh’s flagship initiative that brings together industry, academia and investors to innovate, co-create and build the Fintech ecosystem. The Fintech Spring Conference 2017 marks the beginning of this new journey. Spring conference will have CXOs from Fintech companies, start-ups & financial services. For more information, please visit Spring Conference 2017

Aeries Financial Technologies Pvt. Ltd, a fin-tech company promoted by serial entrepreneur and private equity investor V. Raman Kumar, have announced that CASHe, India’s fastest loan giving app for young salaried professionals is now disbursing loans well over 1 Crore per day in less than a year of operations. CASHe now processes an average of 450 loan applications per day for young salaried professionals. CASHe is now India’s leading and most preferred fin-tech company in the personal lending space.

Launched in April 2016, CASHe offers loans based on a combination of Big Data Analytics and proprietary Artificial Intelligence based algorithm, the Social Loan Quotient, which enables loan disbursal within 8 minutes.

V. Raman Kumar, Chairman, Aeries Financial Technologies Pvt. Ltd said

We have seen a fantastic response to our loan products with a month-on-month 45% growth in customer base and 60% growth in disbursal value in the past few months. Our loan disbursements now stand at 1 crore per day and we have achieved a significant milestone of processing over 450 loan applications on a daily average – all this within a year of setting up our operations. We are now well set to disburse loans worth 30 crores for March 2017.

CASHe has embarked on a tremendous growth trajectory to achieve a loan disbursement value of Rs 100 crore for the month of December 2017. We have leveraged innovative technology along with our proprietary Artificial Intelligence based algorithm platform, the Social Loan Quotient, to make loan disbursal hassle free for our customers, leading to over 70 percent of them returning for fresh loans.

CASHe provides hassle-free loans with app enabled documentation & loan disbursal/repayment process. Powered by its industry-first algorithm driven credit scoring platform, The Social Loan Quotient [SLQ], CASHe quickly determines a user’s credit worthiness by using multiple unique data points to arrive at a distinct credit profile of the customer.

SLQ is transforming the traditional credit rating measurements thereby providing immediate loans to the under-served young professionals who are kept out by traditional credit rating and banking systems. CASHe is completely automated and requires no personal intervention and no physical documentation. The average time taken for a loan to be disbursed is about 8 minutes, subject to proper submission of all documents.

About CASHe

CASHe, a fin-tech product of TSLC PTE. LTD., promoted by Aeries Financial Technologies is as unique as the young professionals it serves. In a smart digital world, CASHe offers millennials quick and easy personal loans through processes that are transparent, innovative and tuned to the times. CASHe utilises sophisticated algorithms and machine learning capabilities to deliver an amazing and improved lending experience to our customers, thereby helping young professionals achieve their financial goals effortlessly. CASHe app is available on Google Play and iOS app store